South Africa Macro Daily(Beta Mode)

Rand Weakens Ahead of GDP Release

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 103,117.60 | -0.29% |

| USD/ZAR | 16.56 | +1.54% |

| EUR/ZAR | 18.98 | -0.29% |

| Platinum | 1,762.10 | +0.73% |

| Gold | 4,360.40 | +0.57% |

| Brent Crude | 93.26 | -1.05% |

| Naspers | 88,300.00 | +1.49% |

| Bitcoin | 63,320.02 | +0.36% |

| South Africa Short-term Rate | 6.75% | +0.00% |

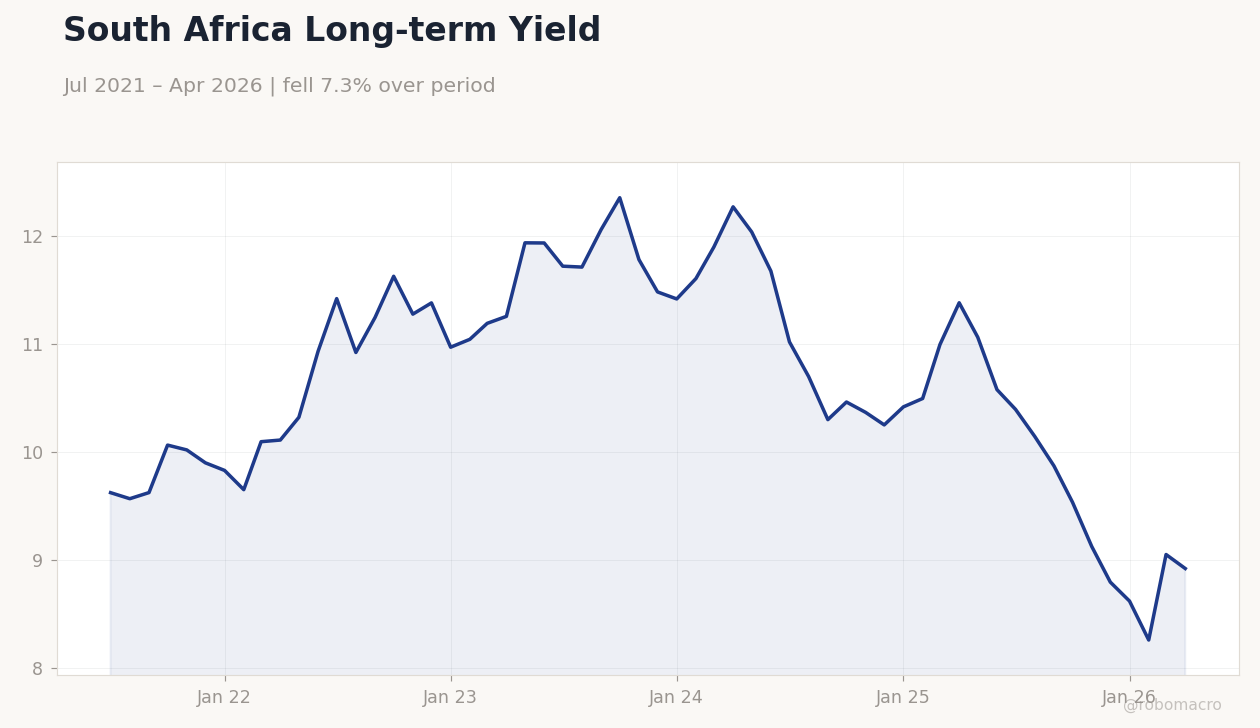

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Long-term Yield | Type: macro_line | 10Y Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

South Africa Long-term Yield | Type: macro_line | 10Y Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.40 | - | 01:00 |

| GDP Growth Year-over-Year | 0.80 | - | 01:00 |

- GDP quarter-over-quarter and year-over-year prints due at 01:00 today with no consensus available.

- USD/ZAR climbs 1.54% to 16.56 as anti-migrant protests intensify across townships.

- South Africa long-term rate falls 1.44% to 8.92% while JSE Top 40 slips 0.29%.

Yesterday's Recap

South African markets closed lower with the JSE Top 40 falling 0.29% to 103,117.60 amid heightened political noise. USD/ZAR advanced 1.54% to 16.56, reflecting rand depreciation, while EUR/ZAR eased 0.29% to 18.98. The long-term government bond yield dropped 1.44% to 8.92%, narrowing the spread over the unchanged 6.75% short-term rate.

Platinum rose 0.73% to 1,762.10 and gold gained 0.57% to 4,360.40, supporting resource names such as Naspers which added 1.49%. Anti-migrant protests persisted in Johannesburg townships despite President Ramaphosa’s televised pledge to address illegal immigration. Nigeria’s foreign minister expressed official displeasure and signaled possible sanctions, adding external pressure on bilateral ties and investor sentiment.

The Day Ahead

Statistics South Africa will release first-quarter GDP growth figures at 01:00, covering both quarter-over-quarter and year-over-year measures. The prints follow prior readings of 0.4% and 0.8% respectively and carry medium market impact. Traders will parse the data for signs of momentum ahead of the next SARB policy meeting.

No additional domestic data or SARB speeches are scheduled. Attention will also remain on any further statements from the presidency regarding migration enforcement.

Other Economic Notes

Persistent xenophobic demonstrations risk dampening foreign direct investment and tourism receipts in the near term. Nigeria’s consideration of sanctions could further strain regional trade links already pressured by weak growth. The unchanged 6.75% repo rate continues to anchor short-term funding costs while the bull-flattening yield curve signals expectations of eventual policy easing.

Commodity price strength in gold and platinum offers partial offset to rand softness.

Global Macro News

Brent crude declined 1.05% to 93.26, weighing on energy-related revenues for the fiscus. Firmer gold and platinum prices provided support to South Africa’s export basket and terms of trade. Bitcoin edged 0.36% higher, offering limited spillover to local risk appetite.

<i>↓ p.2</i>