South Africa Macro Daily(Beta Mode)

SA GDP Beats Forecasts, Rand Firms

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 102,770.45 | -0.34% |

| USD/ZAR | 16.53 | -0.19% |

| EUR/ZAR | 19.08 | +0.17% |

| Platinum | 1,679.00 | -1.73% |

| Gold | 4,222.20 | -0.89% |

| Brent Crude | 91.19 | -0.28% |

| Naspers | 88,999.00 | +0.68% |

| Bitcoin | 61,571.08 | -0.12% |

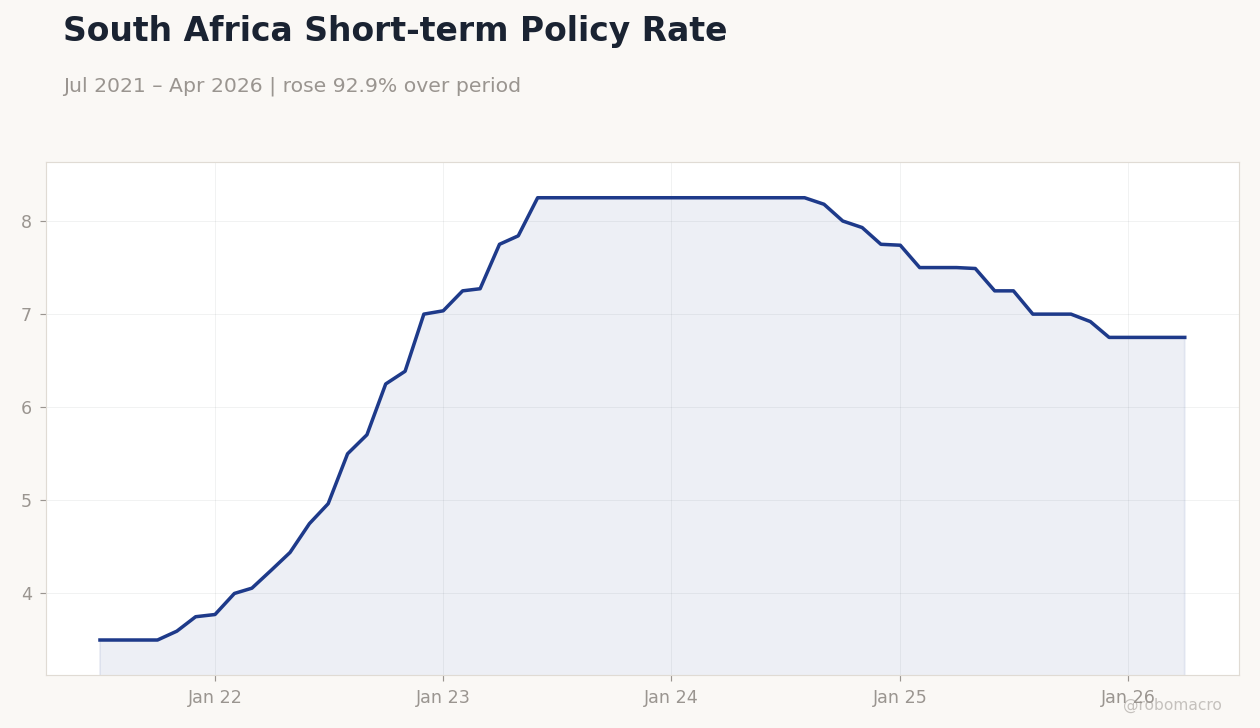

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.40 | 0.30 | 0.50 |

| GDP Growth Year-over-Year | 0.80 | 1.80 | 1.90 |

South Africa Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

South Africa Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- SA GDP grew 0.5% QoQ and 1.9% YoY, both above consensus

- USD/ZAR eased to 16.53 as long-term yields fell 1.44pp

- JSE Top 40 slipped 0.34% while platinum and gold declined

Yesterday's Recap

South Africa’s statistics agency reported first-quarter GDP growth of 0.5% quarter-over-quarter, exceeding the 0.3% consensus, while the year-over-year reading reached 1.9% against expectations of 1.8%. The better-than-expected print lifted the rand, sending USD/ZAR 0.19% lower to 16.53 and EUR/ZAR 0.17% higher to 19.08. The JSE Top 40 closed 0.34% down at 102,770.45 despite Naspers rising 0.68%.

The long-term government bond yield dropped 1.44pp to 8.92%. Platinum fell 1.73% to 1,679.00 and gold declined 0.89% to 4,222.20. Short-term rates remained unchanged at 6.75%.

Anti-migrant protests continued in Gauteng townships but produced limited immediate market reaction.

The Day Ahead

Markets enter a data-light session with no scheduled South African releases. Focus will remain on ongoing Eskom operational updates and any follow-through from yesterday’s GDP figures. Global commodity price moves, particularly in platinum group metals and Brent crude at 91.19, will influence rand and mining equity flows.

Investor attention may also track developments around potential Nigerian sanctions linked to xenophobic incidents. The absence of domestic prints leaves USD/ZAR and JSE direction largely dependent on external risk sentiment.

Other Economic Notes

Eskom launched its Eskom Green renewable unit, which will initially operate under the holding company before becoming an autonomous subsidiary. The move raises questions about the utility’s standalone credit profile following the planned separation of generation, transmission and distribution assets. Renewed xenophobic violence prompted several African governments to begin repatriating citizens, adding to social and reputational pressures.

Student debt levels continue to block graduate entry into the formal labour market, constraining medium-term productivity growth. These structural issues sit alongside the stronger GDP print and reinforce the case for cautious policy easing.

Global Macro News

Softer US inflation prints supported broader emerging-market flows, providing a modest tailwind for the rand. Brent crude eased 0.28% to 91.19, limiting upside for SA energy exporters. <i>↓ p.2</i>