South Africa Macro Daily(Beta Mode)

GDP Beat Bolsters Rand Outlook

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 101,837.57 | -1.31% |

| USD/ZAR | 16.45 | -0.47% |

| EUR/ZAR | 19.08 | +0.15% |

| Platinum | 1,683.30 | -0.28% |

| Gold | 4,127.00 | +0.46% |

| Brent Crude | 92.37 | -0.78% |

| Naspers | 88,137.00 | -0.97% |

| Bitcoin | 62,644.02 | +1.94% |

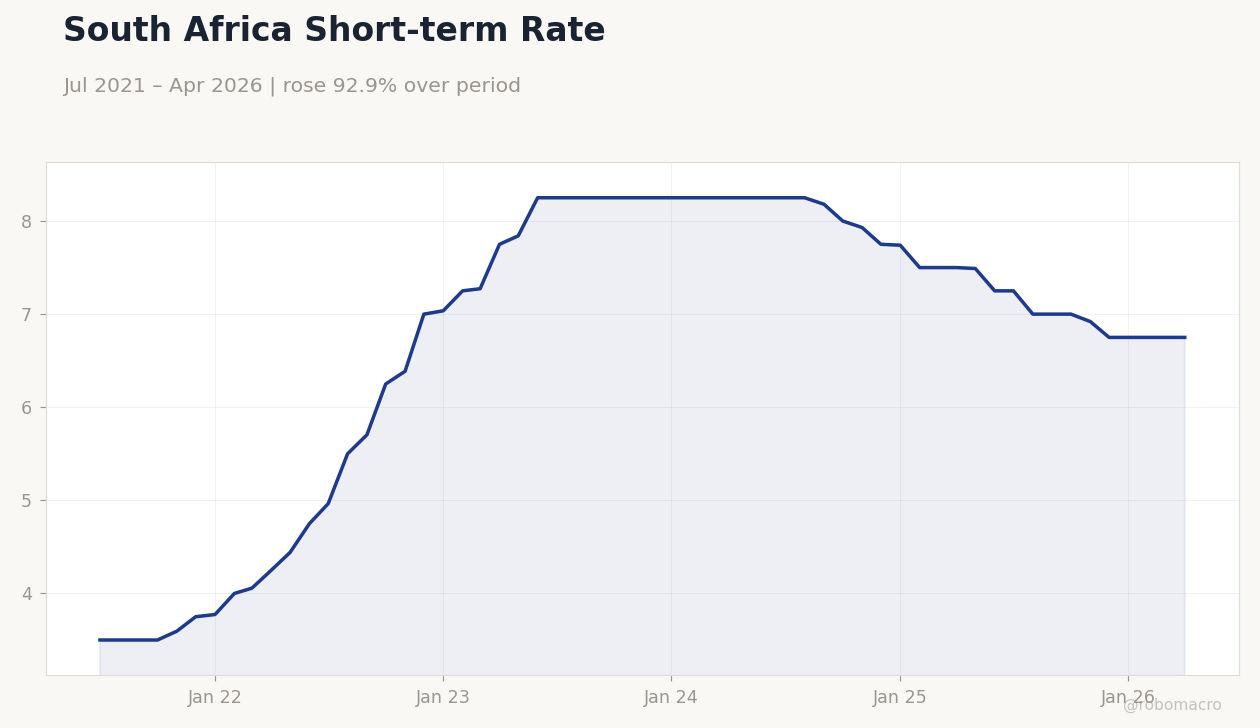

| South Africa Short-term Rate | 6.75% | +0.00% |

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.40 | 0.30 | 0.50 |

| GDP Growth Year-over-Year | 0.80 | 1.80 | 1.90 |

South Africa Short-term Rate | Type: macro_line | Policy Rate (%): 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

South Africa Short-term Rate | Type: macro_line | Policy Rate (%): 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- SA GDP growth surprised to the upside with QoQ at 0.5% and YoY at 1.9%, both above consensus.

- JSE Top 40 fell 1.31% to 101,837.57 while the long-term rate eased 1.44% to 8.92%.

- USD/ZAR declined 0.47% to 16.45, reflecting modest rand support amid stable repo rate at 6.75%.

Yesterday's Recap

South Africa’s economy expanded faster than expected in the first quarter. GDP rose 0.5% quarter-over-quarter against a 0.3% consensus and 0.4% prior reading. Year-over-year growth reached 1.9%, well above the 1.8% forecast and 0.8% previous print.

Equity markets sold off, with the JSE Top 40 closing 1.31% lower at 101,837.57. The rand strengthened modestly, sending USD/ZAR to 16.45. Long-term government yields declined sharply, with the South Africa Long-term Rate falling 1.44% to 8.92%.

Short-term rates remained unchanged at 6.75%. Commodity prices were mixed, with gold rising 0.46% to 4,127 while platinum slipped 0.28% to 1,683.30 and Brent crude fell 0.78% to 92.37. Bitcoin gained 1.94% to 62,644.02, adding a mild risk-on tone.

The Day Ahead

No high-impact South African data releases are scheduled for today or tomorrow. Markets will focus on global commodity trends and any follow-through from yesterday’s GDP print. The absence of domestic events leaves the rand and bonds sensitive to external risk sentiment.

Traders will monitor USD/ZAR for signs of further consolidation below 16.50. Attention may also turn to corporate updates from mining houses given recent production guidance changes.

Other Economic Notes

Recent commentary points to continued pressure on household finances from elevated borrowing costs. SARB communications have reiterated the 3% inflation target despite global supply shocks. Fiscal authorities have reaffirmed the 4.5% deficit ceiling, limiting additional borrowing.

Load-shedding risks remain a drag on mining output expectations. These factors together keep the growth outlook cautious even after the stronger GDP release.

Global Macro News

Gold advanced 0.46% to 4,127 while Brent crude eased 0.78% to 92.37, reflecting mixed commodity demand signals. Bitcoin rose 1.94% to 62,644.02, providing some risk-on tone for emerging-market currencies. The Bank of Canada held its policy rate steady, underscoring a cautious global monetary stance.

<i>↓ p.2</i>