South Africa Macro Daily(Beta Mode)

GDP Beats Consensus, Rand Rallies on Metals

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 102,315.00 | +0.65% |

| USD/ZAR | 16.32 | -1.59% |

| EUR/ZAR | 18.86 | -1.43% |

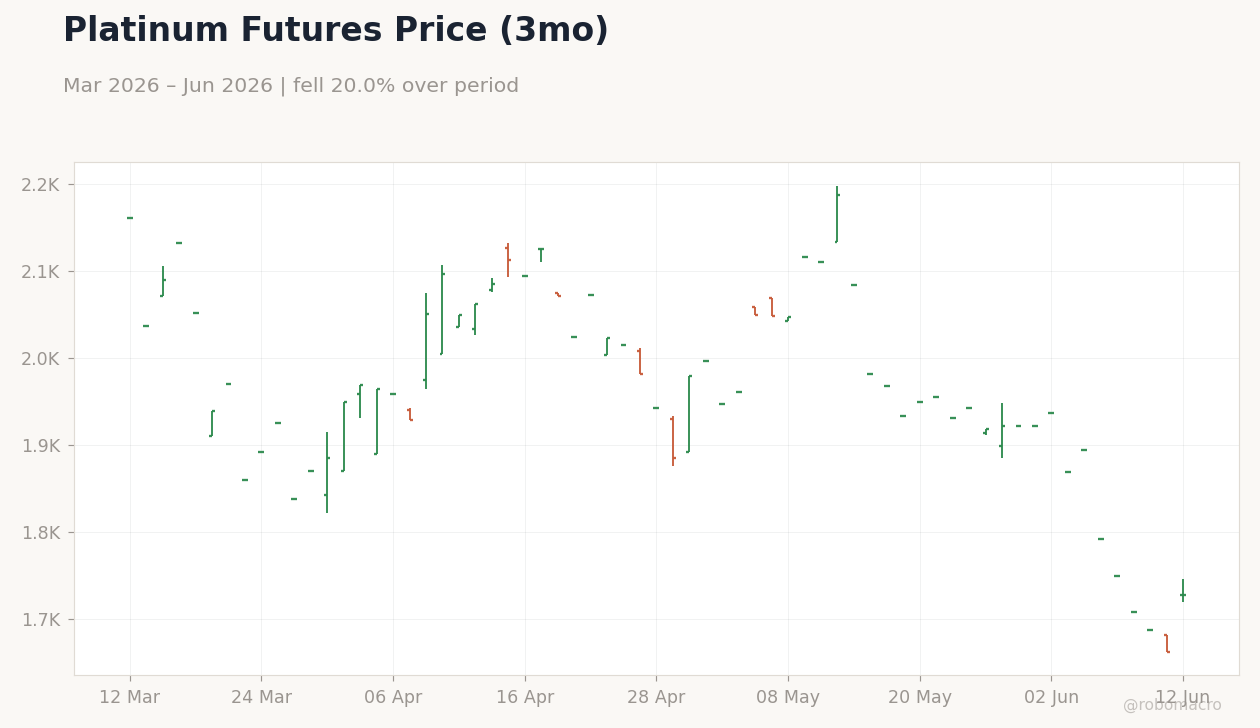

| Platinum | 1,728.50 | +3.96% |

| Gold | 4,200.40 | +2.69% |

| Brent Crude | 88.40 | -2.19% |

| Naspers | 87,769.00 | -0.94% |

| Bitcoin | 63,272.63 | +2.97% |

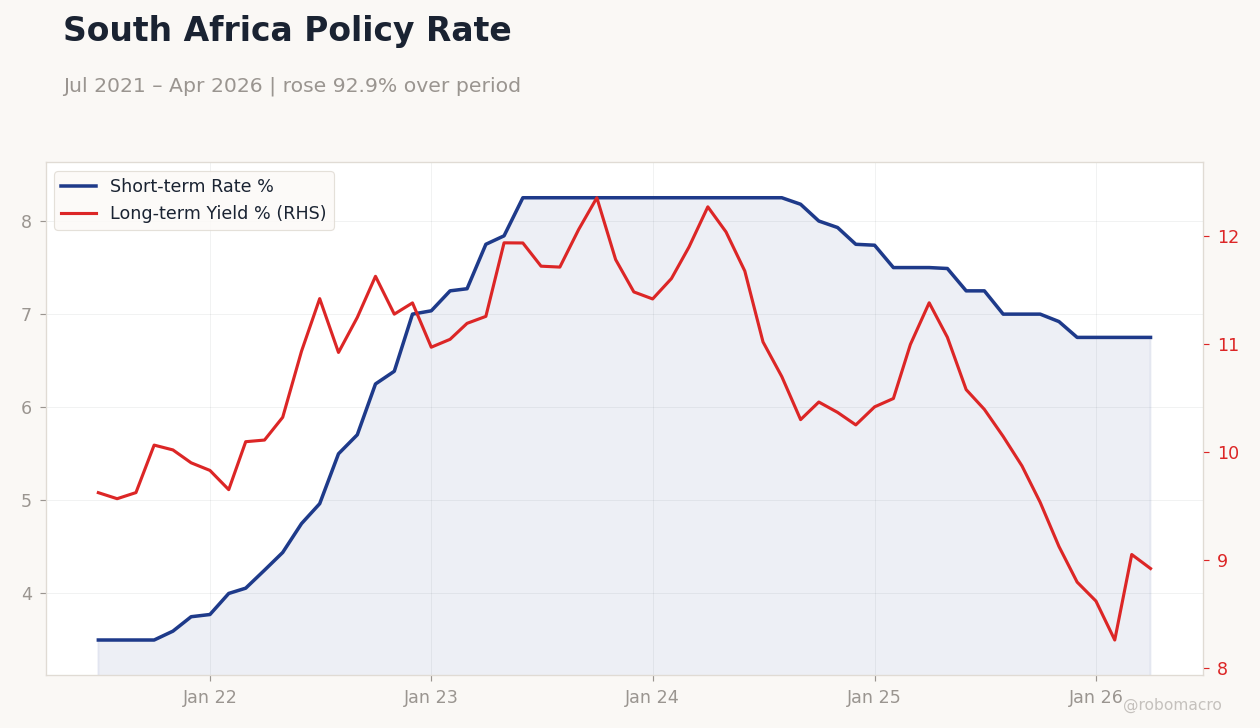

| South Africa Short-term Rate | 6.75% | +0.00% |

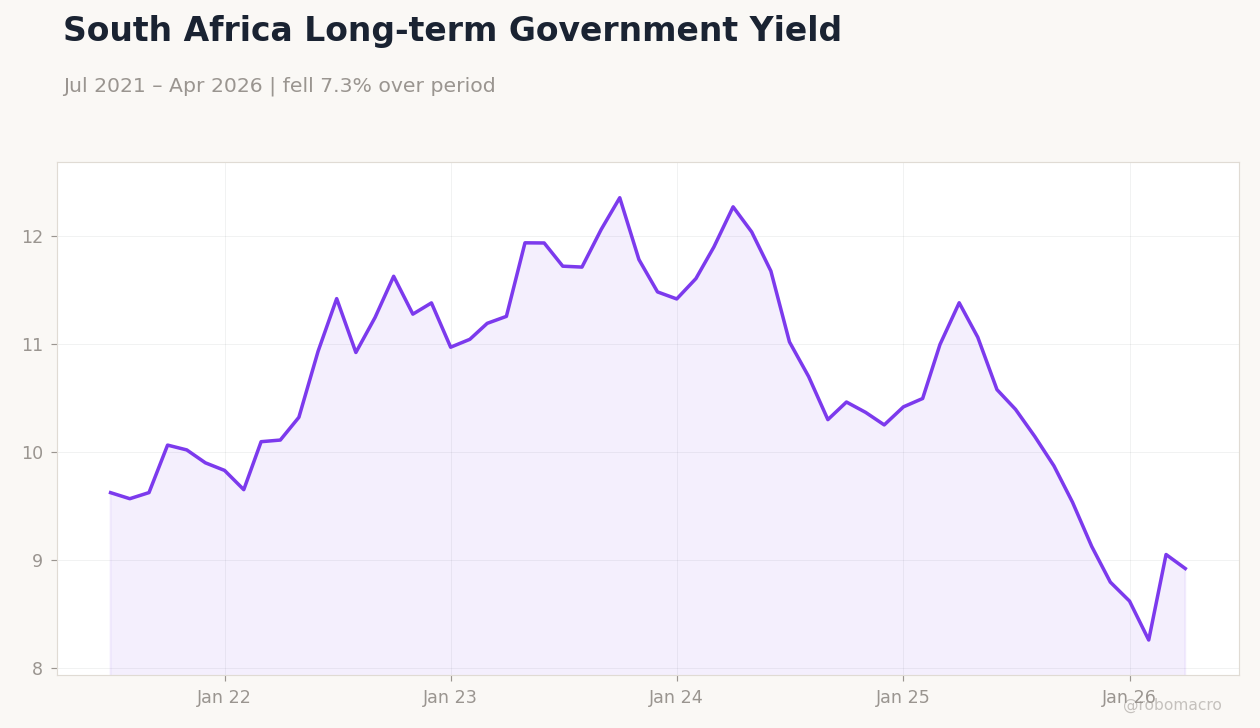

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.40 | 0.30 | 0.50 |

| GDP Growth Year-over-Year | 0.80 | 1.80 | 1.90 |

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75 | Long-term Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

South Africa Policy Rate | Type: macro_line | Short-term Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75 | Long-term Yield %: 8.92 (2026-04-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.05,8.92

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South Africa GDP growth beat expectations with 0.5% q/q and 1.9% y/y prints.

- USD/ZAR fell 1.59% to 16.32 as platinum and gold surged.

- JSE Top 40 rose 0.65% while the long-term rate eased 1.44% to 8.92%.

Yesterday's Recap

South Africa reported stronger-than-expected GDP growth for the first quarter, with quarter-over-quarter expansion at 0.5% versus the 0.3% consensus and year-over-year growth reaching 1.9% against the 1.8% forecast. The positive surprise lifted market sentiment and supported the rand. USD/ZAR declined 1.59% to close at 16.32 while EUR/ZAR fell 1.43% to 18.86.

The JSE Top 40 index advanced 0.65% to 102,315, driven by mining shares. Platinum jumped 3.96% to 1,728.50 and gold rose 2.69% to 4,200.40. The South Africa long-term rate declined 1.44% to 8.92% as the short-term rate held steady at 6.75%.

Brent crude fell 2.19% to 88.40, providing limited offset to the commodity-led gains.

The Day Ahead

No major South African data releases are scheduled for today, leaving markets to digest yesterday’s GDP figures. Focus will remain on rand flows and any follow-through in precious metals prices. The absence of new prints allows attention to shift toward global commodity trends and their impact on the current account.

Traders will monitor USD/ZAR for signs of sustained strength below 16.40. Equity investors may rotate further into resource names if platinum and gold hold gains. SARB communications are not expected, keeping policy expectations anchored to the 6.75% repo rate.

Other Economic Notes

Mining output remains a key growth driver after the strong GDP print, with platinum and gold prices providing direct support to export revenues. Energy supply constraints continue to pose downside risks to industrial production despite the recent positive data. The long-term rate decline signals improving investor appetite for South African duration amid firmer growth.

Fiscal revenue trends will warrant watching as higher commodity prices could lift tax collections from the mining sector. Overall, the economy shows resilience in external balances while domestic demand indicators stay subdued.

Global Macro News

Stronger precious metals prices reflect global safe-haven demand and supply concerns in major producing regions. <i>↓ p.2</i>