South Africa Macro Daily(Beta Mode)

JSE Climbs as Rand Firms on Metals Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 104,697.80 | +2.33% |

| USD/ZAR | 16.18 | -0.64% |

| EUR/ZAR | 18.77 | -0.39% |

| Platinum | 1,771.90 | +3.67% |

| Gold | 4,329.80 | +2.72% |

| Brent Crude | 83.50 | -4.39% |

| Naspers | 85,592.00 | -0.48% |

| Bitcoin | 65,746.12 | +2.06% |

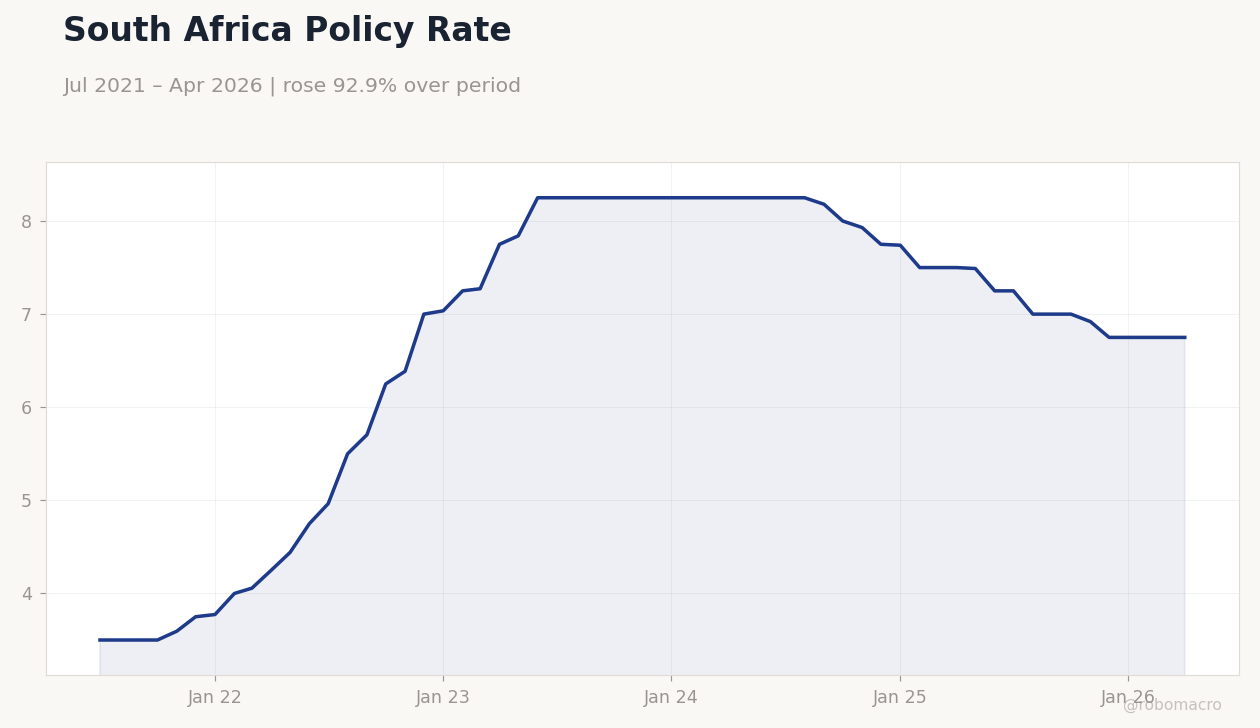

| South Africa Short-term Rate | 6.75% | +0.00% |

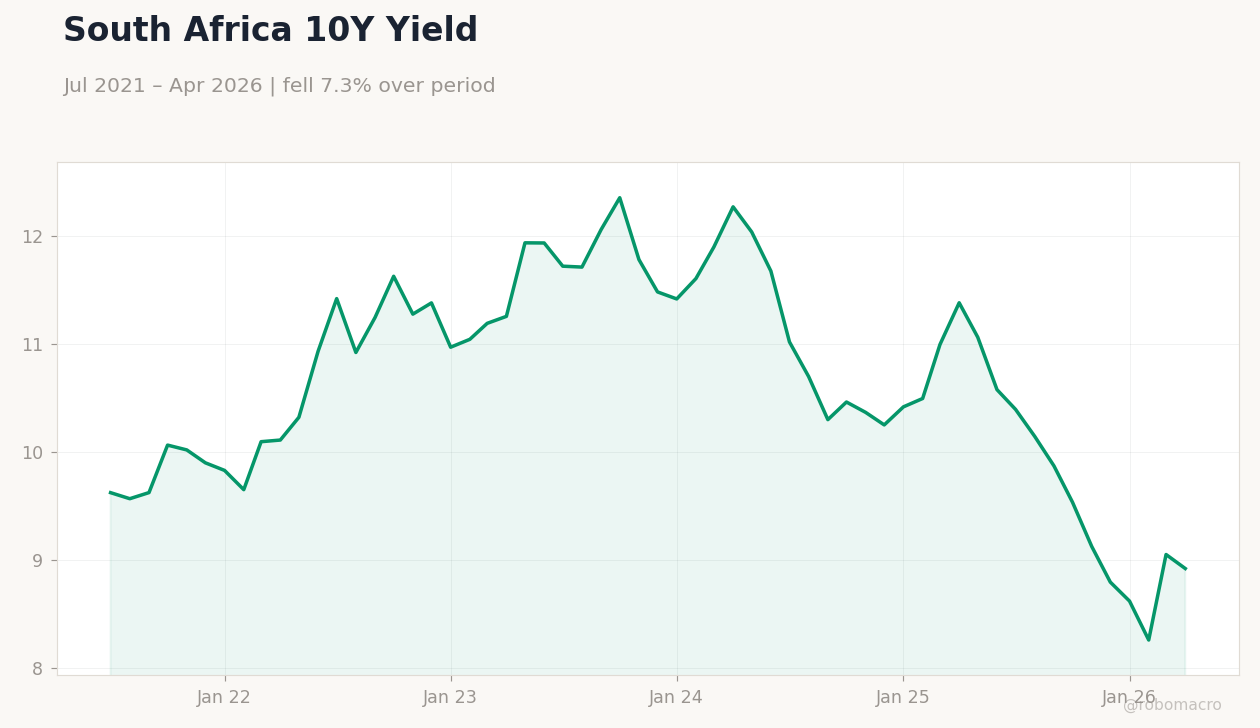

| South Africa Long-term Rate | 8.92% | -1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Policy Rate | Type: macro_line | Repo Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

South Africa Policy Rate | Type: macro_line | Repo Rate %: 6.75 (2026-04-01) | Range: 3.5–8.25 | Trend(5pt): 3.5,5.705,8.25,7.74,6.75

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-17) | |||

| Inflation Rate Month-over-Month | 1.10 | - | 00:00 |

| Inflation Rate Year-over-Year | 4 | - | 00:00 |

- JSE Top 40 rises 2.33% to 104,697.80 driven by platinum and gold gains.

- USD/ZAR drops 0.64% to 16.18 while long-term yields fall 1.44% to 8.92%.

- SARB repo rate holds steady at 6.75% ahead of June inflation data.

Yesterday's Recap

South African markets posted strong gains on June 14 with no major data releases. The JSE Top 40 climbed 2.33 percent as platinum jumped 3.67 percent to 1,771.90 and gold advanced 2.72 percent to 4,329.80 on safe-haven demand. The rand strengthened, sending USD/ZAR down 0.64 percent to 16.18 and EUR/ZAR 0.39 percent lower to 18.77.

Brent crude fell 4.39 percent to 83.50, weighing on energy names while Naspers slipped 0.48 percent. The long-term government bond yield eased 1.44 percent to 8.92 percent, reflecting improved risk sentiment. Bitcoin rose 2.06 percent but had limited spillover to local assets.

Overall volume remained thin with focus shifting to the upcoming inflation print.

The Day Ahead

Markets await the June 17 release of South Africa’s inflation rate month-over-month and year-over-year figures. The prints carry medium impact and follow prior readings of 1.1 percent and 4.0 percent respectively. A softer outcome could reinforce expectations for steady policy while any upside surprise may pressure front-end yields.

The SARB Quarterly Bulletin is also due but carries no press conference. No MPC speeches are scheduled. Traders will monitor rand reaction for clues on rate path through year-end.

Other Economic Notes

The World Bank lowered its 2026 South Africa GDP growth forecast, contributing to rand volatility earlier in the month. Government efforts to repatriate 2,745 foreigners in one week highlight ongoing immigration pressures that may affect labor markets and fiscal costs. Long-term borrowing costs remain sensitive to policy credibility amid the wider deficit trajectory.

Mining output data continue to reflect energy supply constraints. These factors keep external vulnerability elevated despite recent commodity strength.

Global Macro News

Global commodity markets supported South Africa with gold and platinum rallying on geopolitical tensions and safe-haven flows. Brent crude’s 4.39 percent drop eased imported inflation risks for the rand economy. <i>↓ p.2</i>