South Africa Macro Daily(Beta Mode)

Rand Climbs to Three-Month High on Peace Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 104,697.80 | +2.33% |

| USD/ZAR | 16.22 | +0.30% |

| EUR/ZAR | 18.76 | -0.01% |

| Platinum | 1,755.70 | -0.81% |

| Gold | 4,339.00 | +0.25% |

| Brent Crude | 82.75 | -0.50% |

| Naspers | 85,592.00 | -0.48% |

| Bitcoin | 66,070.62 | +0.55% |

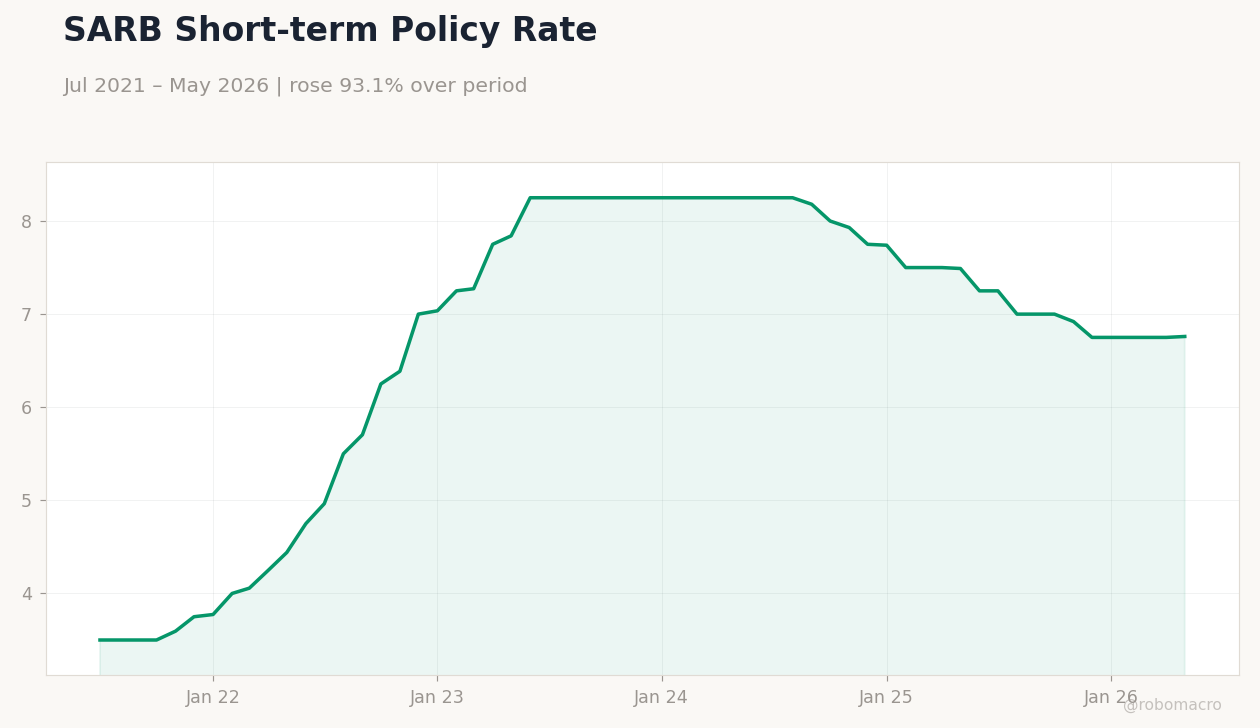

| South Africa Short-term Rate | 6.76% | +0.15% |

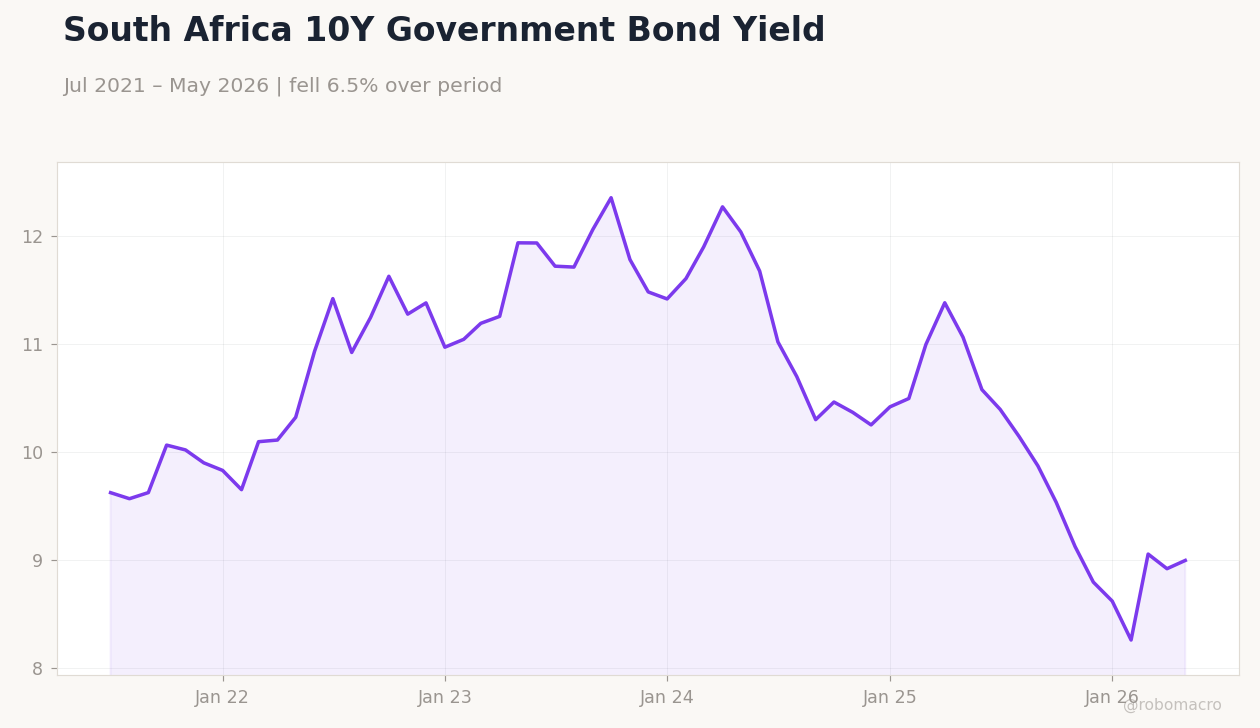

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

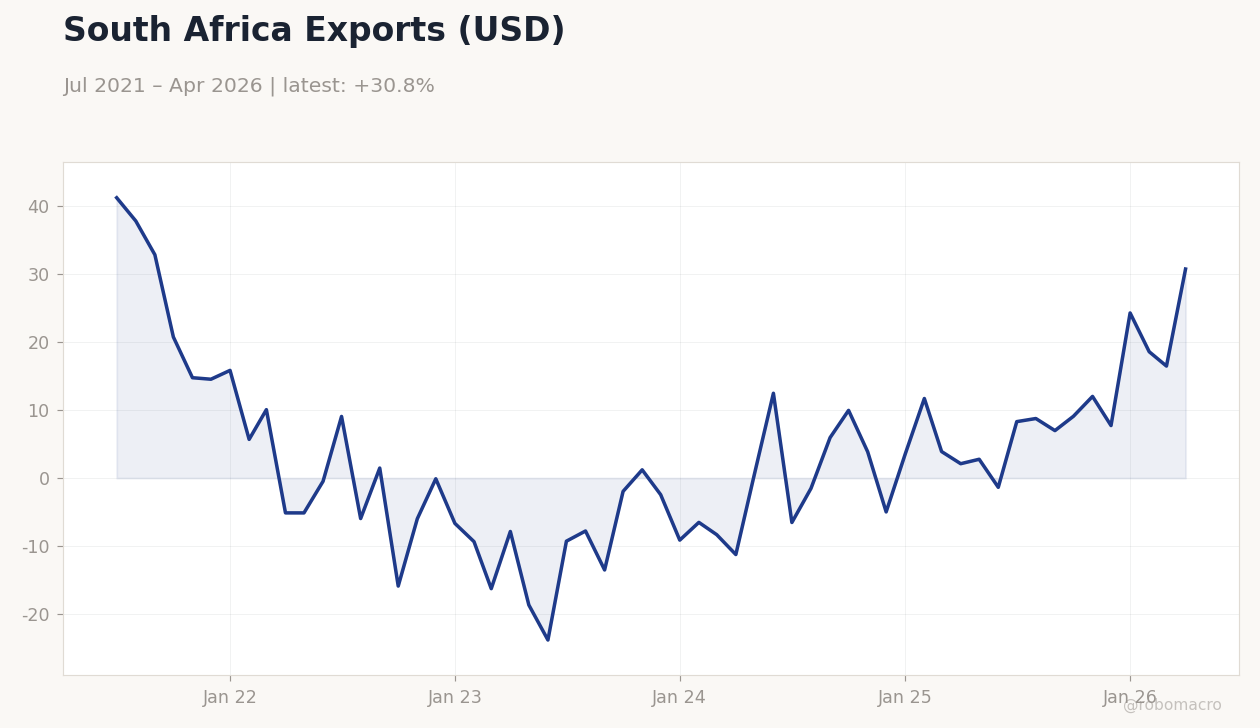

South Africa Exports (USD) | Type: macro_line | YoY %: 30.76 (2026-04-01) | Range: -23.83–41.25 | Trend(6pt): 41.25,1.473,1.213,3.546,16.48,30.76

South Africa Exports (USD) | Type: macro_line | YoY %: 30.76 (2026-04-01) | Range: -23.83–41.25 | Trend(6pt): 41.25,1.473,1.213,3.546,16.48,30.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-17) | |||

| Inflation Rate Month-over-Month | 1.10 | - | 00:00 |

| Inflation Rate Year-over-Year | 4 | - | 00:00 |

- Rand strengthens to three-month highs as peace deal optimism lifts sentiment.

- JSE Top 40 rises 2.33% to 104,697.80 while traders cut SARB hike bets.

- Inflation data due tomorrow with prior YoY rate at 4.0%.

Yesterday's Recap

The rand firmed sharply, with USD/ZAR closing at 16.22 after a 0.30% gain that pushed the currency to its strongest level in three months. MarketForces Africa attributed the move to shifting sentiment around a potential peace deal. The JSE Top 40 advanced 2.33%, supported by gains in gold at 4,339.00 despite platinum slipping 0.81%.

South Africa’s short-term rate stood at 6.75% and the long-term rate reached 8.99%. Foreign investors reduced exposure to local assets amid Iran-related global market volatility. News of 2,745 repatriations highlighted tighter immigration enforcement under President Ramaphosa.

Brent crude fell 0.50% to 82.75, easing imported inflation concerns.

The Day Ahead

Statistics South Africa will release May inflation figures at midnight ET, covering both month-over-month and year-over-year rates. Markets expect the prints to influence the scale of any remaining SARB tightening priced for 2026. No other domestic data or MPC speeches are scheduled.

Traders will monitor global oil moves for further shifts in rate expectations. The JSE and rand open will set the tone ahead of the prints.

Other Economic Notes

Long-term fiscal credibility continues to anchor South Africa’s borrowing costs, according to Business Report analysis. Persistent load-shedding risks and mining output volatility remain key constraints on growth. Immigration enforcement has intensified, with over 40,000 arrests reported this year.

These factors weigh on investor sentiment even as the rand benefits from short-term sentiment swings.

Global Macro News

Iran conflict concerns triggered broad foreign outflows from South African assets, as reported by Business News Nigeria. Oil price weakness reduced near-term inflation risks and prompted traders to slash SARB hike bets, per Newsnote. Global equity caution spilled into emerging-market currencies, limiting rand gains despite local positive drivers.

Gold held steady near 4,339, offering some support to mining equities. <i>↓ p.2</i>