South Africa Macro Daily(Beta Mode)

SA Inflation Data Looms as Rand Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 107,296.40 | -0.23% |

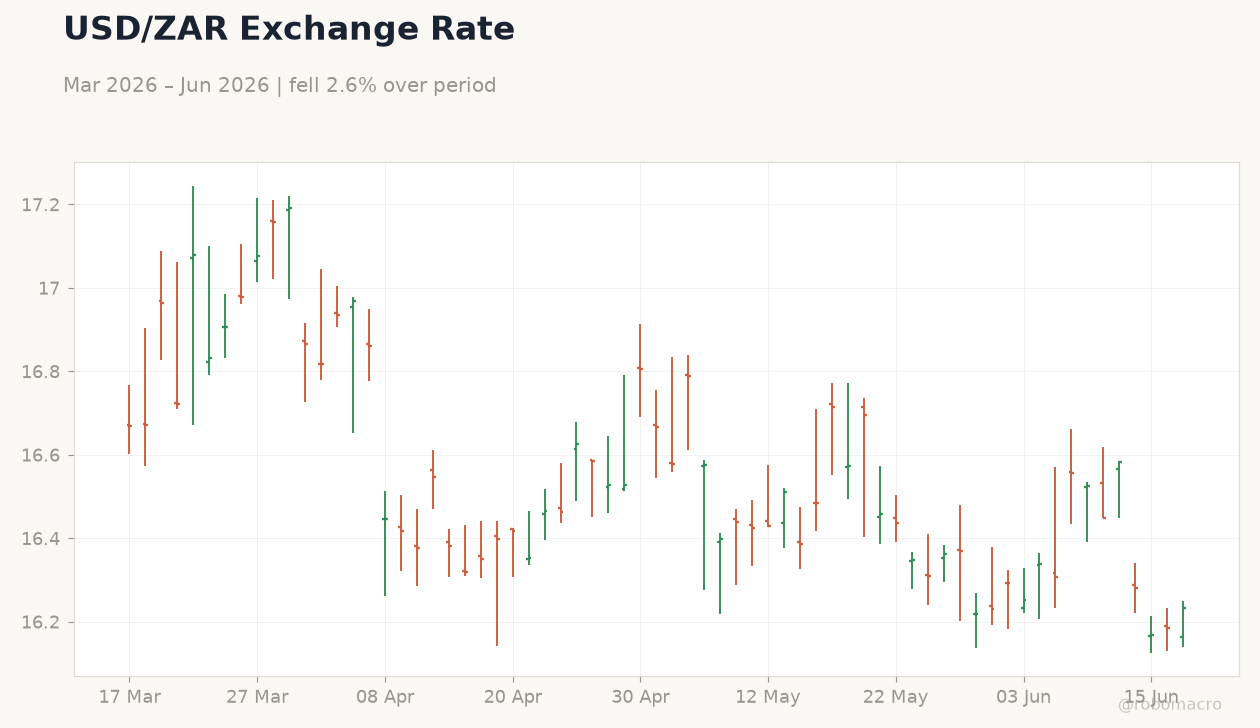

| USD/ZAR | 16.23 | +0.27% |

| EUR/ZAR | 18.83 | +0.34% |

| Platinum | 1,788.90 | -1.28% |

| Gold | 4,344.00 | +0.30% |

| Brent Crude | 78.93 | -0.04% |

| Naspers | 86,286.00 | +0.81% |

| Bitcoin | 65,046.90 | -0.84% |

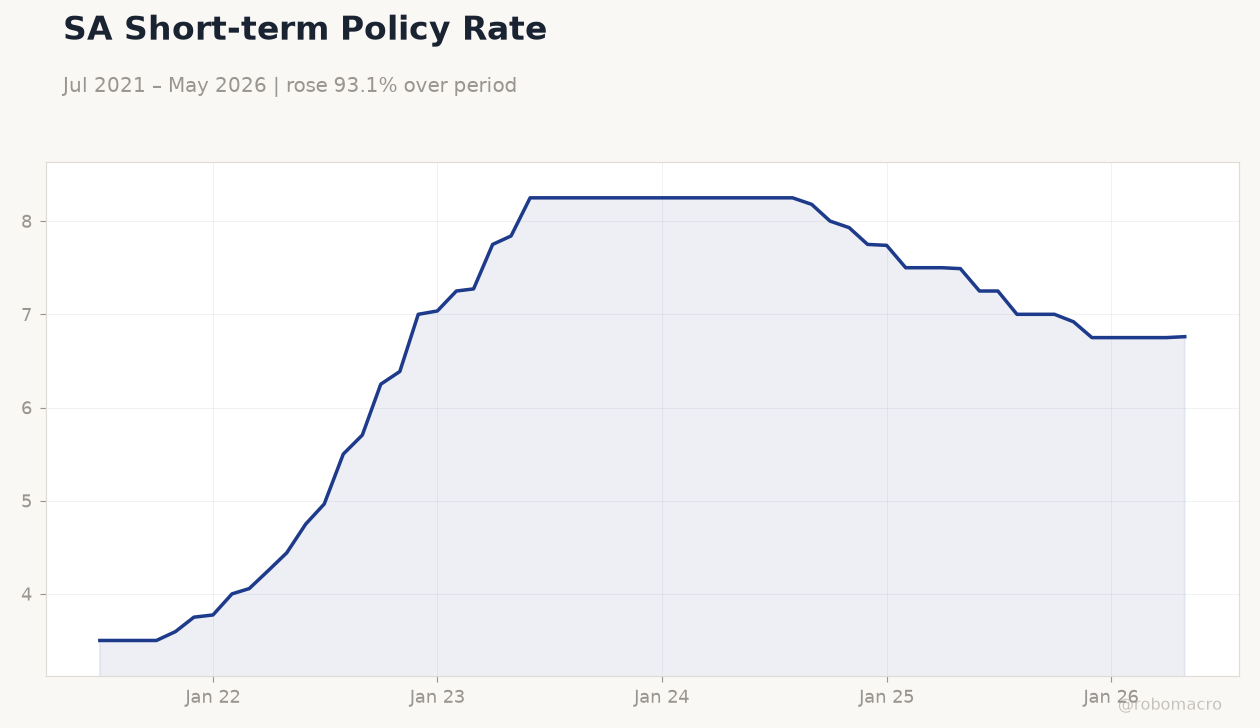

| South Africa Short-term Rate | 6.76% | +0.15% |

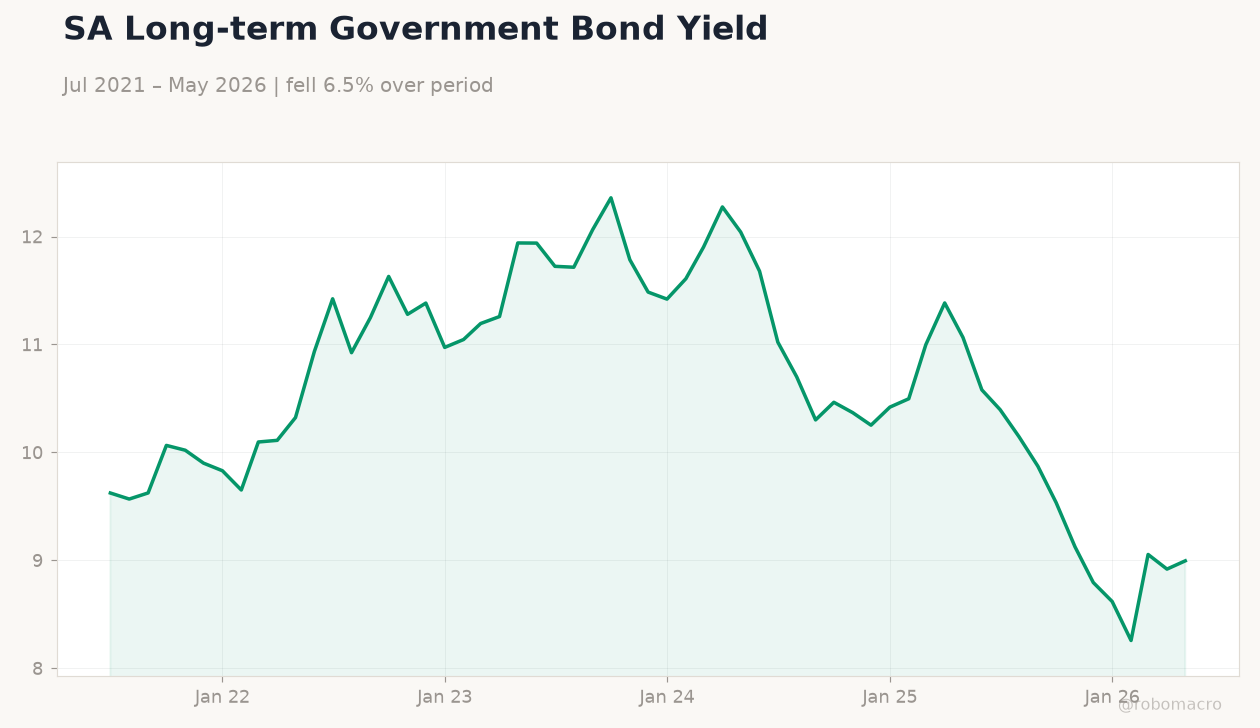

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SA Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

SA Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.10 | - | 04:00 |

| Inflation Rate Year-over-Year | 4 | 4.70 | 04:00 |

- South Africa CPI prints due today with consensus YoY at 4.7% after May jump to near two-year high

- JSE Top 40 slips 0.23% to 107,296 while USD/ZAR climbs 0.27% to 16.23 on risk-off flows

- Mining output resilience and persistent energy constraints shape near-term growth and policy outlook

Yesterday's Recap

South African markets closed mixed on 16 June with the JSE Top 40 declining 0.23 percent amid thin volumes and commodity rotation. USD/ZAR rose 0.27 percent to 16.23 while EUR/ZAR gained 0.34 percent, reflecting mild dollar strength and local inflation concerns. Platinum fell 1.28 percent to 1,788.90 dollars per ounce whereas gold edged 0.30 percent higher.

The short-term rate held at 6.76 percent and the long-term yield climbed 0.86 percent to 8.99 percent, steepening the curve. News flow highlighted renewed xenophobic tensions that threaten services exports and regional trade links. No major data releases occurred, leaving investors focused on today’s inflation figures and their implications for SARB timing.

The Day Ahead

Statistics South Africa will release May inflation data at 04:00 ET, covering both month-over-month and year-over-year readings. Markets expect the annual rate to reach 4.7 percent, up from 4.0 percent previously, driven largely by energy costs. The prints will directly inform July MPC deliberations and near-term rate path pricing.

No SARB speakers are scheduled. Attention will also turn to any updates on Eskom load-shedding stages and their effect on industrial production.

Other Economic Notes

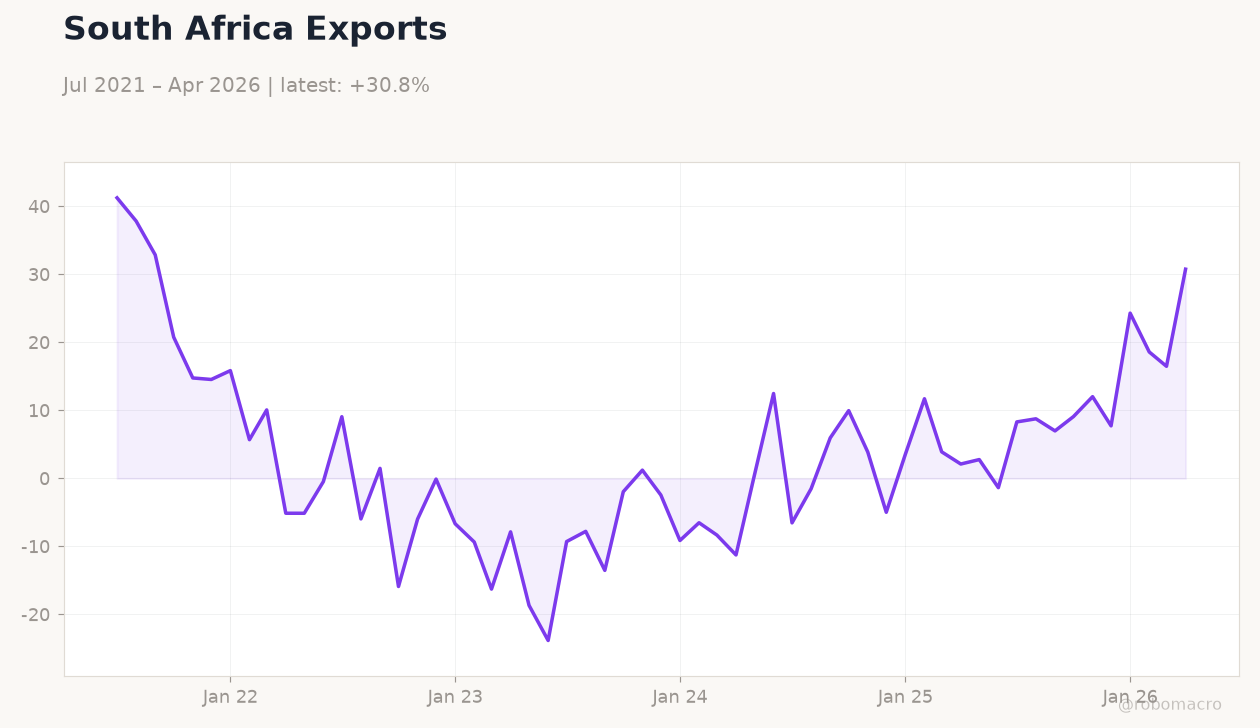

May mining production beat expectations, supporting the view that second-quarter GDP will avoid contraction despite power shortages. Exxon’s preliminary LNG supply agreement offers medium-term relief for coal-dependent generation but does not alter immediate load-shedding risks. Persistent xenophobic incidents are already curtailing cross-border services revenue and could weigh on foreign direct investment inflows in the second half.

Global Macro News

Softer US CPI prints improved global risk sentiment and supported gold prices, providing a modest buffer for rand-linked assets. OPEC+ supply discipline kept Brent crude near 78.93 dollars, limiting downside for South African terms of trade. Elevated US yields continued to exert mild pressure on emerging-market currencies including the rand.

<i>↓ p.2</i>