South Africa Macro Daily(Beta Mode)

SA Inflation Miss Eases Hike Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 108,040.90 | +0.46% |

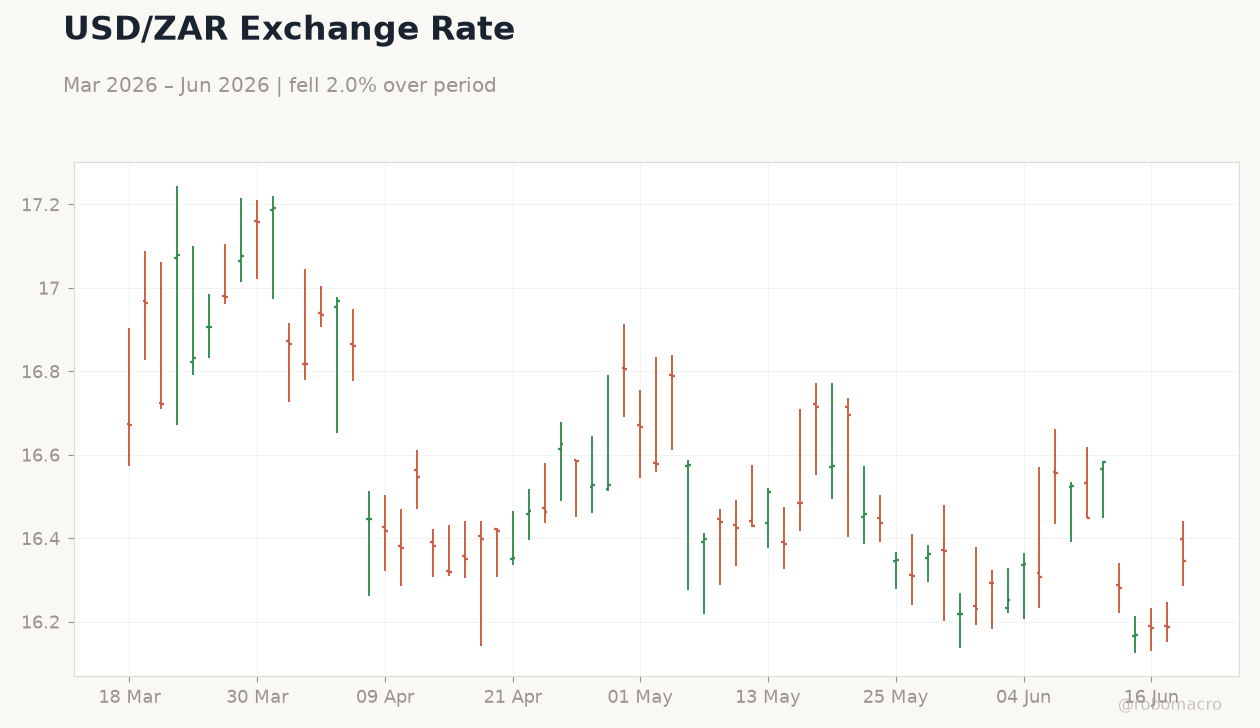

| USD/ZAR | 16.31 | +0.77% |

| EUR/ZAR | 18.81 | +0.08% |

| Platinum | 1,754.30 | -2.03% |

| Gold | 4,324.50 | -0.79% |

| Brent Crude | 77.24 | -2.90% |

| Naspers | 84,000.00 | -2.65% |

| Bitcoin | 63,975.00 | -2.48% |

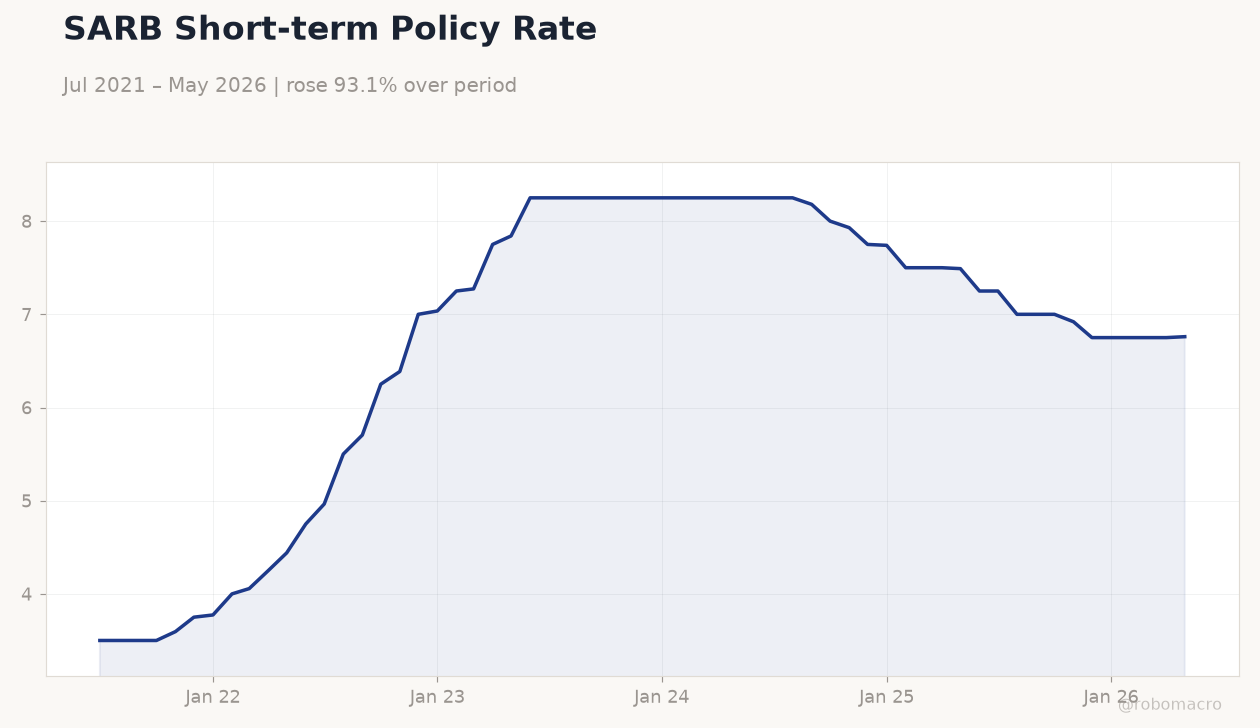

| South Africa Short-term Rate | 6.76% | +0.15% |

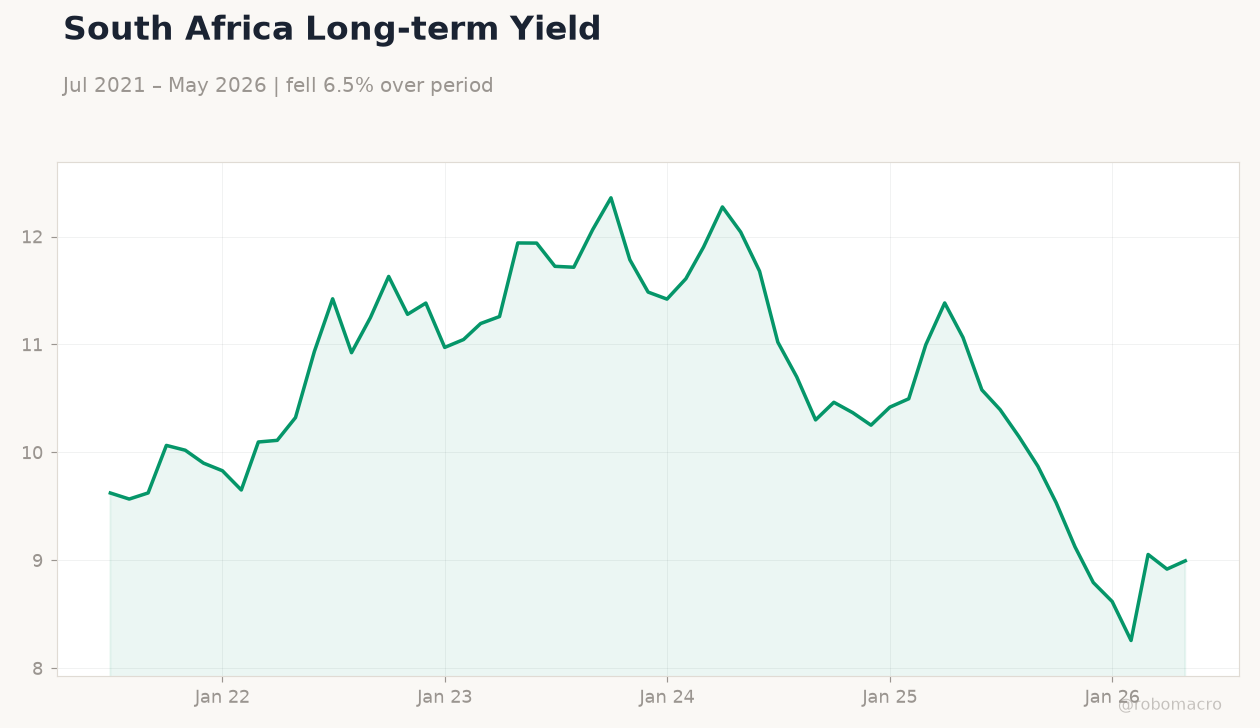

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.10 | - | 0.70 |

| Inflation Rate Year-over-Year | 4 | 4.70 | 4.50 |

SARB Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

SARB Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- May CPI rose 4.5% y/y, missing 4.7% consensus and easing immediate rate-hike pressure.

- USD/ZAR climbed 0.77% to 16.31 while JSE Top 40 gained 0.46% to 108,040.90.

- SARB repo rate held at 6.76% as markets trimmed tightening odds after the soft print.

Yesterday's Recap

South Africa’s May inflation printed 0.7% m/m and 4.5% y/y, both below expectations and prior prints. The softer outcome reinforced views that the SARB will keep the repo rate at 6.76% through the coming meetings. USD/ZAR rose 0.77% to 16.31 while EUR/ZAR edged 0.08% higher to 18.81, reflecting modest rand softening on global dollar strength.

The JSE Top 40 advanced 0.46% to 108,040.90, supported by resource names despite platinum falling 2.03% to $1,754.30 and gold declining 0.79% to $4,324.50. Brent crude dropped 2.90% to $77.24, adding to downside pressure on mining revenues. South Africa’s short-term rate climbed 0.15% to 6.76% and the long-term rate jumped 0.86% to 8.99%, steepening the curve.

Traders responded by scaling back near-term hike probabilities embedded in FRAs.

The Day Ahead

The domestic calendar is empty today, leaving markets to digest yesterday’s inflation surprise. Focus will remain on rand flows and any follow-through in commodity prices. Global risk sentiment and US data releases will likely dictate USD/ZAR direction.

Mining equities may continue to track platinum and gold moves amid ongoing energy-supply concerns. No SARB speakers are scheduled, keeping the latest MPC guidance as the operative policy signal.

Other Economic Notes

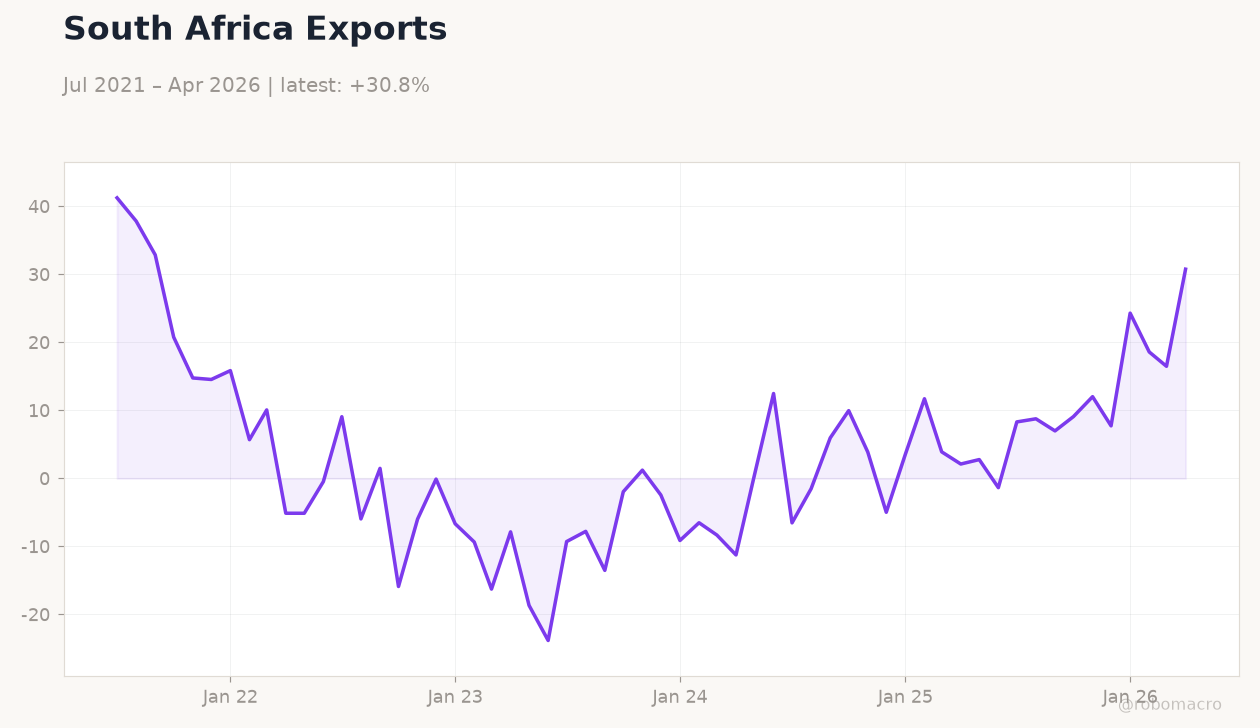

Persistent load-shedding risks continue to weigh on Q3 mining output and electricity-intensive sectors. The current-account surplus remains supported by gold exports, providing a buffer for the rand. Long-term fiscal credibility concerns keep South Africa’s borrowing costs elevated relative to peers.

BRICS-bank funding for urban infrastructure offers modest relief but does not alter near-term growth dynamics.

Global Macro News

Softer US data reduced global rate-hike expectations, supporting commodity currencies broadly. OPEC+ supply discipline signals lifted Brent earlier in the week before yesterday’s reversal. Platinum prices faced additional pressure from rhodium supply concerns outside South Africa.

<i>↓ p.2</i>