South Africa Macro Daily(Beta Mode)

SA Inflation Undershoots at 4.5% as Rand Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 106,955.70 | -1.00% |

| USD/ZAR | 16.51 | +0.89% |

| EUR/ZAR | 18.83 | +0.22% |

| Platinum | 1,672.60 | -1.91% |

| Gold | 4,161.10 | -1.49% |

| Brent Crude | 80.31 | +0.58% |

| Naspers | 84,500.00 | +0.60% |

| Bitcoin | 62,703.97 | -0.31% |

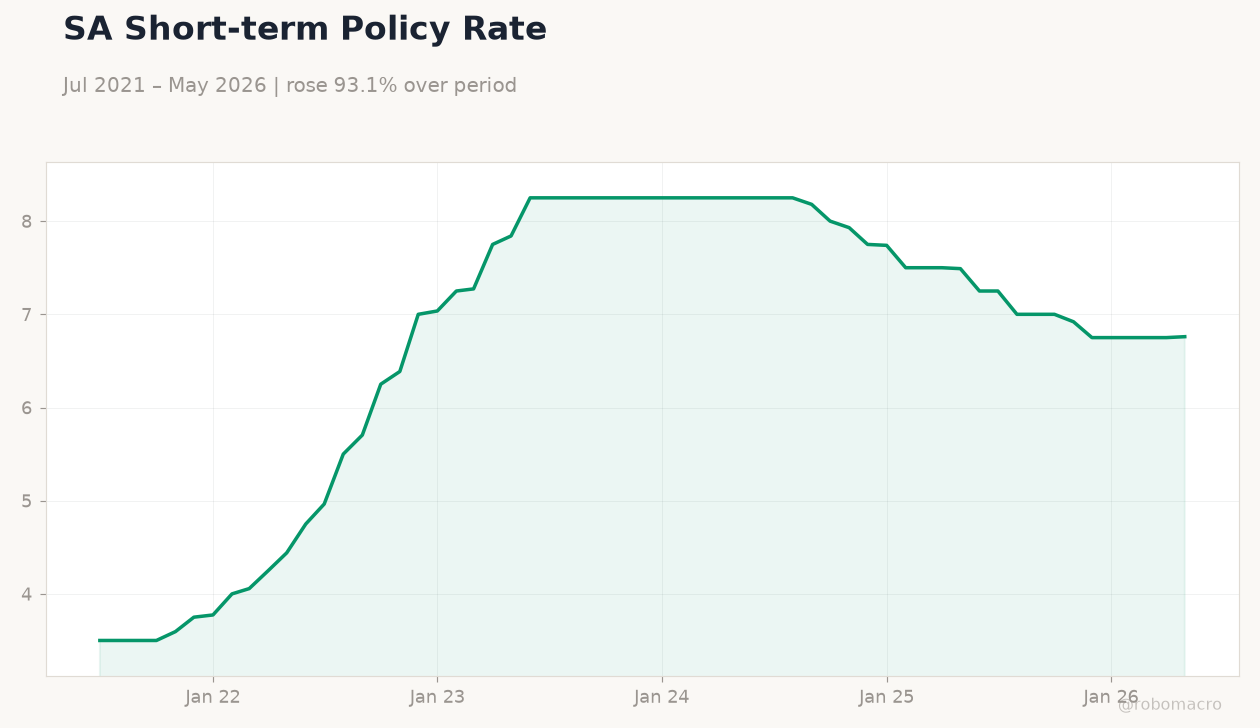

| South Africa Short-term Rate | 6.76% | +0.15% |

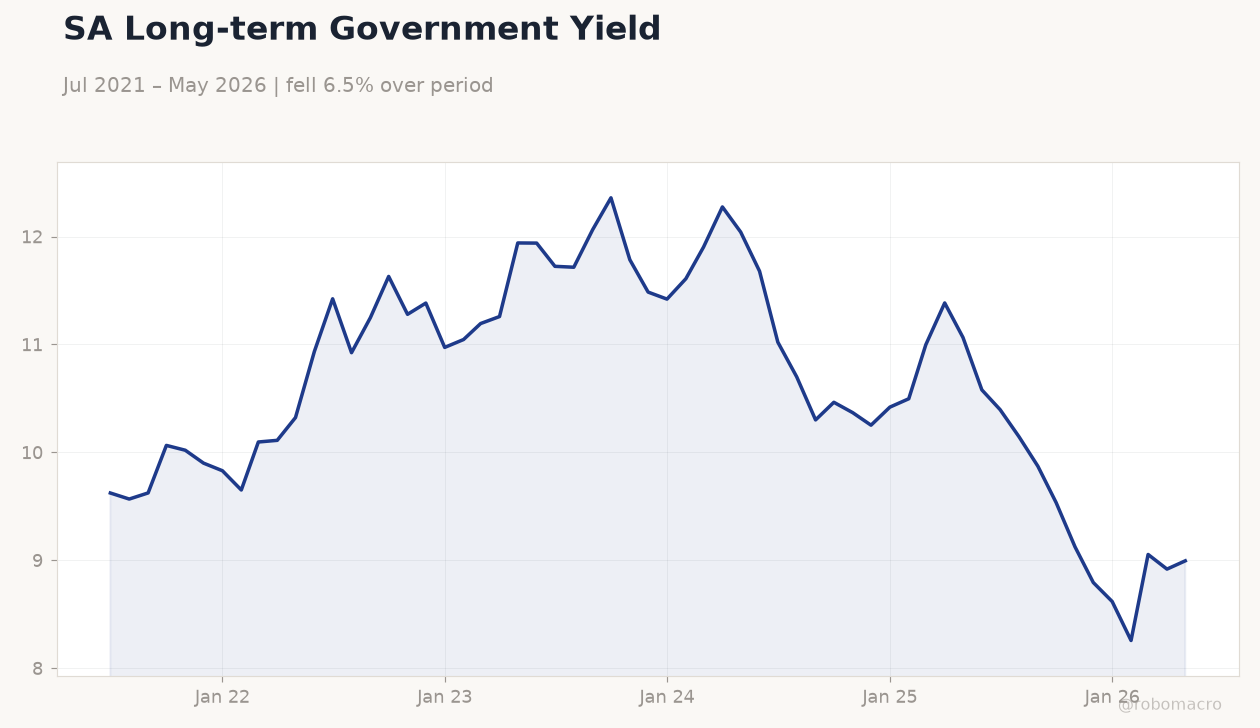

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 1.10 | - | 0.70 |

| Inflation Rate Year-over-Year | 4 | 4.70 | 4.50 |

SA Long-term Government Yield | Type: macro_line | 10Y Yield %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.054,8.995

SA Long-term Government Yield | Type: macro_line | 10Y Yield %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.054,8.995

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- May CPI rises 4.5% y/y, below 4.7% consensus, with MoM at 0.7%

- JSE Top 40 drops 1.00% to 106,955.70 as USD/ZAR climbs 0.89% to 16.51

- SARB short-term rate at 6.76% while long-term yield reaches 8.99%

Yesterday's Recap

South Africa’s May inflation printed 4.5% y/y and 0.7% m/m, undershooting consensus and prior readings amid softer food and transport components. The JSE Top 40 fell 1.00% to 106,955.70, led by resource names as platinum declined 1.91% to 1,672.60 and gold fell 1.49% to 4,161.10. USD/ZAR rose 0.89% to 16.51 while EUR/ZAR gained 0.22% to 18.83, reflecting rand underperformance.

The short-term rate stood at 6.76% and the long-term yield climbed to 8.99%. Brent crude edged 0.58% higher to 80.31, offering limited support to the currency. Naspers gained 0.60% while Bitcoin slipped 0.31%.

The Day Ahead

No scheduled South African data releases appear on the calendar for 19 June. Markets will monitor ongoing fuel-price effects on June inflation prints and any follow-through from yesterday’s CPI undershoot. Global risk sentiment and US policy signals remain the dominant drivers for USD/ZAR and JSE flows.

Mining output and Eskom supply updates could surface in corporate commentary. Traders will watch for any SARB or Treasury remarks on the revenue shortfall flagged earlier this month.

Other Economic Notes

Fuel-price shocks lifted headline inflation to a 22-month high despite the monthly moderation. Xenophobic tensions with Nigeria threaten potential measures against South African firms operating in that market. An apartheid-era statute still in force continues to constrain investment and growth according to industry commentary.

Immigrant contributions to food security remain economically material yet politically contested. Broader US-Africa relations face recalibration risks that could affect capital flows into the rand and local assets.

Global Macro News

Warsh’s first Fed meeting raised the prospect of higher US rates, increasing external pressure on South African yields and the currency. OPEC+ signals of steady supply supported Brent at 80.31, providing modest terms-of-trade relief. Chinese auto data lifted platinum earlier in the week before yesterday’s reversal.

Global risk-on flows showed limited transmission to the JSE Top 40 amid local inflation concerns. South African bonds priced in a possible pause in SARB easing following the CPI print. <i>↓ p.2</i>