South Africa Macro Daily(Beta Mode)

Rand Steady as SARB's Hawkish Tone Softens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 104,258.70 | -2.52% |

| USD/ZAR | 16.42 | -0.09% |

| EUR/ZAR | 18.82 | -0.09% |

| Platinum | 1,668.20 | -2.17% |

| Gold | 4,209.90 | -0.34% |

| Brent Crude | 78.96 | -1.11% |

| Naspers | 84,500.00 | +0.60% |

| Bitcoin | 64,146.25 | -0.15% |

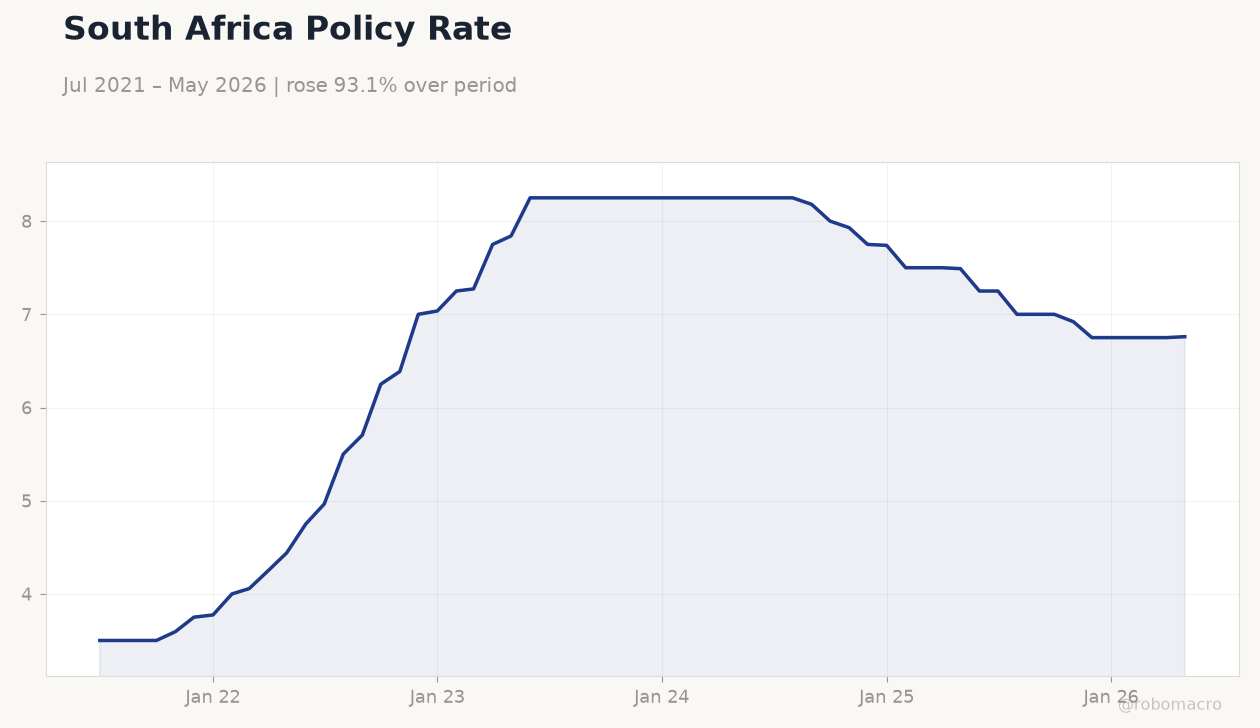

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

South Africa Policy Rate | Type: macro_line | Policy Rate (%): 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

South Africa Policy Rate | Type: macro_line | Policy Rate (%): 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- JSE Top 40 drops 2.52% to 104,258.70 while long-term yields jump 86 bp to 8.99%

- USD/ZAR holds near 16.42 with only a 0.09% decline as platinum falls 2.17%

- Short-term rate edges up 15 bp to 6.76% amid limited reaction to softening SARB signals

Yesterday's Recap

South African markets recorded modest rand stability despite equity weakness and rising yields. The JSE Top 40 declined 2.52% to close at 104,258.70, pressured by a 2.17% drop in platinum to 1,668.20 and a 0.34% fall in gold to 4,209.90. USD/ZAR eased 0.09% to 16.42 while EUR/ZAR also slipped 0.09% to 18.82.

The South Africa long-term rate climbed sharply 0.86% to 8.99%, outpacing the 0.15% rise in the short-term rate to 6.76%. Brent crude fell 1.11% to 78.96, adding to resource sector pressure. No major data releases occurred, leaving market moves driven by external flows and the SARB’s tempered hawkish messaging.

Naspers gained 0.60% to 84,500.00, providing limited support to the broader index. Bitcoin slipped 0.15% to 64,146.25.

The Day Ahead

The domestic calendar remains empty of scheduled releases, directing attention to global risk sentiment and any follow-up SARB commentary. Traders will monitor USD/ZAR reactions to US data and commodity price swings, particularly platinum and gold. Potential updates on Eskom load-shedding or Treasury borrowing plans could surface and affect yields.

The absence of MPC speakers keeps focus on the recent softening in hawkish language already priced into OIS markets. Rand positioning may stay range-bound near current levels unless external shocks emerge.

Other Economic Notes

Fiscal concerns continue to anchor the long end of the yield curve as borrowing needs rise. Mining output guidance cuts from major producers weigh on JSE resources exposure and the broader equity index. Energy supply constraints remain a structural drag on growth without near-term resolution.

The rand’s resilience reflects the SARB’s credible inflation targeting within the 3-6% band despite external volatility.

Global Macro News

US policy signals under new Fed leadership raise the prospect of sustained higher global rates, increasing pressure on emerging-market currencies including the rand. <i>↓ p.2</i>