South Africa Macro Daily(Beta Mode)

Rand Weakens on Peace Deal Concerns

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 104,422.20 | +0.16% |

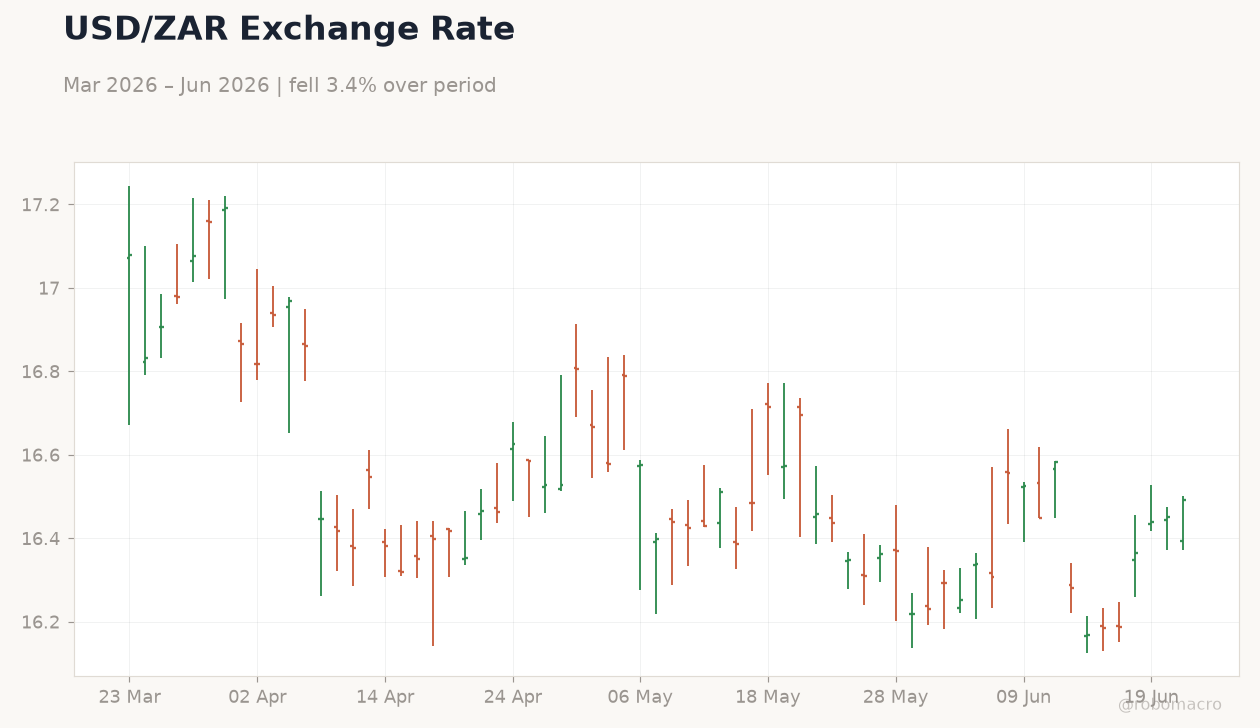

| USD/ZAR | 16.49 | +0.21% |

| EUR/ZAR | 18.83 | -0.14% |

| Platinum | 1,631.20 | -2.34% |

| Gold | 4,131.40 | -1.21% |

| Brent Crude | 76.70 | -1.54% |

| Naspers | 84,500.00 | +0.60% |

| Bitcoin | 62,880.44 | -1.68% |

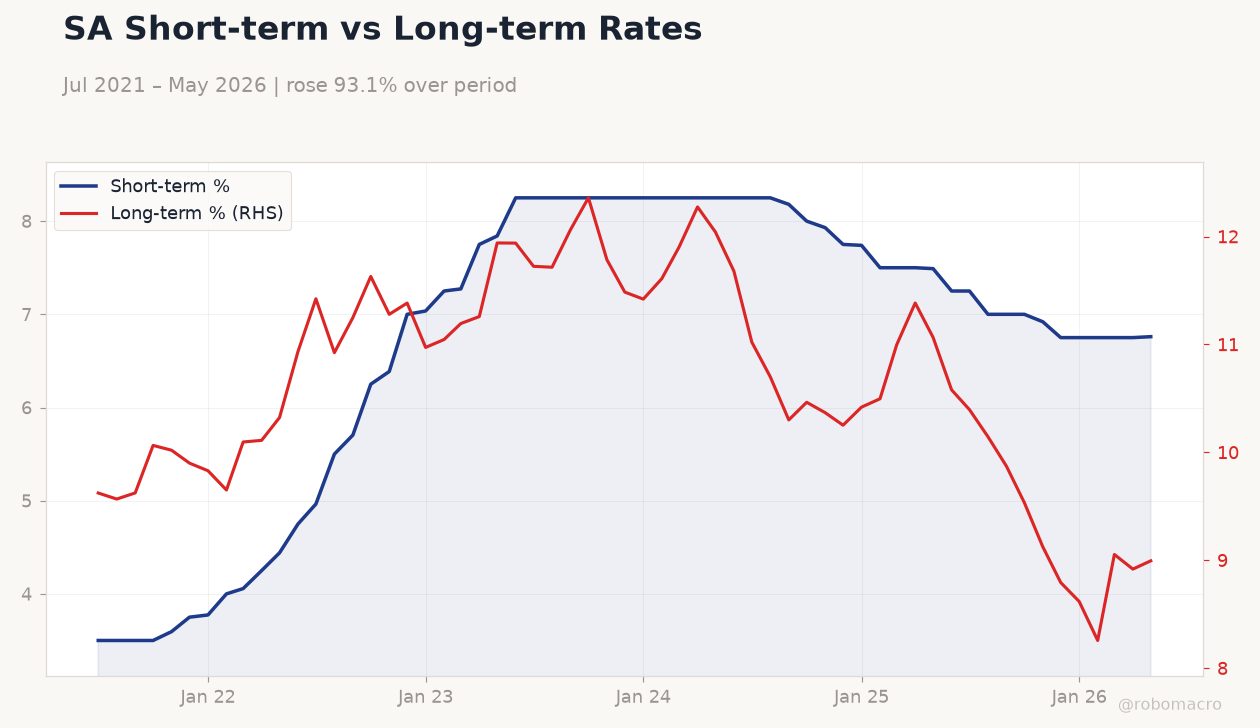

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SA Short-term vs Long-term Rates | Type: macro_line | Short-term %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76 | Long-term %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.054,8.995

SA Short-term vs Long-term Rates | Type: macro_line | Short-term %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76 | Long-term %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.624,11.25,11.79,10.42,9.054,8.995

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- JSE Top 40 edges 0.16% higher to 104,422.20 while USD/ZAR rises 0.21% to 16.49

- Platinum drops 2.34% to 1,631.20 and Brent crude falls 1.54% to 76.70 amid softer commodity demand

- SARB repo rate holds at 2.25% with short-term rates at 6.76% and long-term yields climbing to 8.99%

Yesterday's Recap

South African markets recorded modest gains in equities as the JSE Top 40 advanced 0.16% to close at 104,422.20, supported by Naspers which rose 0.60%. The rand softened against the dollar, with USD/ZAR climbing 0.21% to 16.49, reflecting concerns over peace deal durability. EUR/ZAR eased 0.14% to 18.83.

Commodity prices declined, with platinum falling 2.34% to 1,631.20, gold dropping 1.21% to 4,131.40 and Brent crude retreating 1.54% to 76.70. South Africa short-term rates rose 0.15% to 6.76% while long-term rates increased 0.86% to 8.99%. No economic data releases occurred on the day.

The Day Ahead

Markets face a quiet session with no scheduled South African data releases or events. Attention will turn to global commodity price movements and any shifts in risk sentiment that could influence rand flows. Mining output and manufacturing figures remain absent from the calendar, leaving investors to monitor external drivers.

The absence of domestic catalysts keeps focus on USD/ZAR positioning and JSE resource stocks. Thin trading volumes may amplify any moves in platinum or gold prices.

Other Economic Notes

South Africa’s mining sector faces ongoing pressure from weaker platinum and gold prices, weighing on export earnings and related equities. Energy supply constraints continue to pose risks to industrial output despite the lack of fresh load-shedding updates. Fiscal allocations, including social relief grants, sustain concerns about expenditure slippage without new Treasury announcements.

Broader African market integration efforts offer limited immediate relief for local capital markets.

Global Macro News

Global commodity markets eased, with Brent crude declining on softer demand signals. African currencies showed mixed performance, with the naira gaining on higher foreign reserves while the rand faced specific local pressures from peace deal durability concerns. IMF commentary on declining aid to the continent highlights the need for stronger domestic capacity across sub-Saharan economies.

<i>↓ p.2</i>