South Africa Macro Daily(Beta Mode)

Rand Weakens on Dollar Strength, JSE Slips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 103,388.50 | -0.99% |

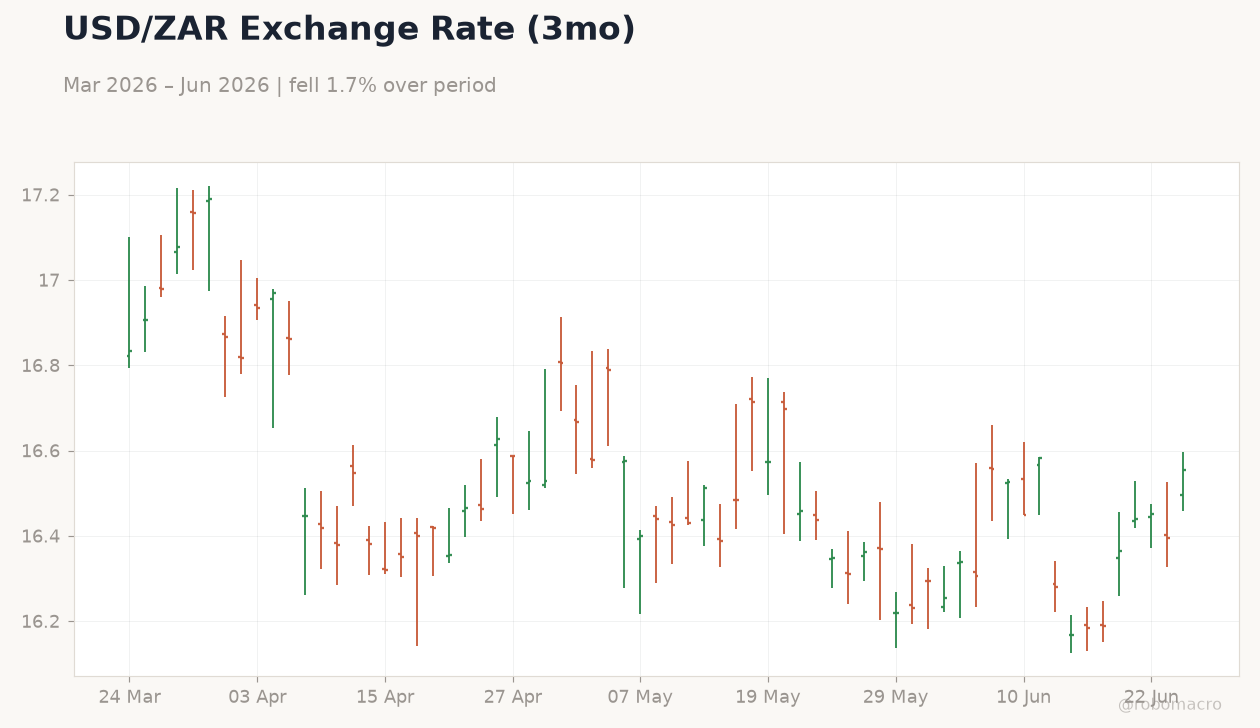

| USD/ZAR | 16.39 | -0.34% |

| EUR/ZAR | 18.74 | -0.63% |

| Platinum | 1,651.00 | -0.60% |

| Gold | 4,106.20 | -0.57% |

| Brent Crude | 76.48 | -0.78% |

| Naspers | 84,500.00 | +0.60% |

| Bitcoin | 62,753.59 | -1.87% |

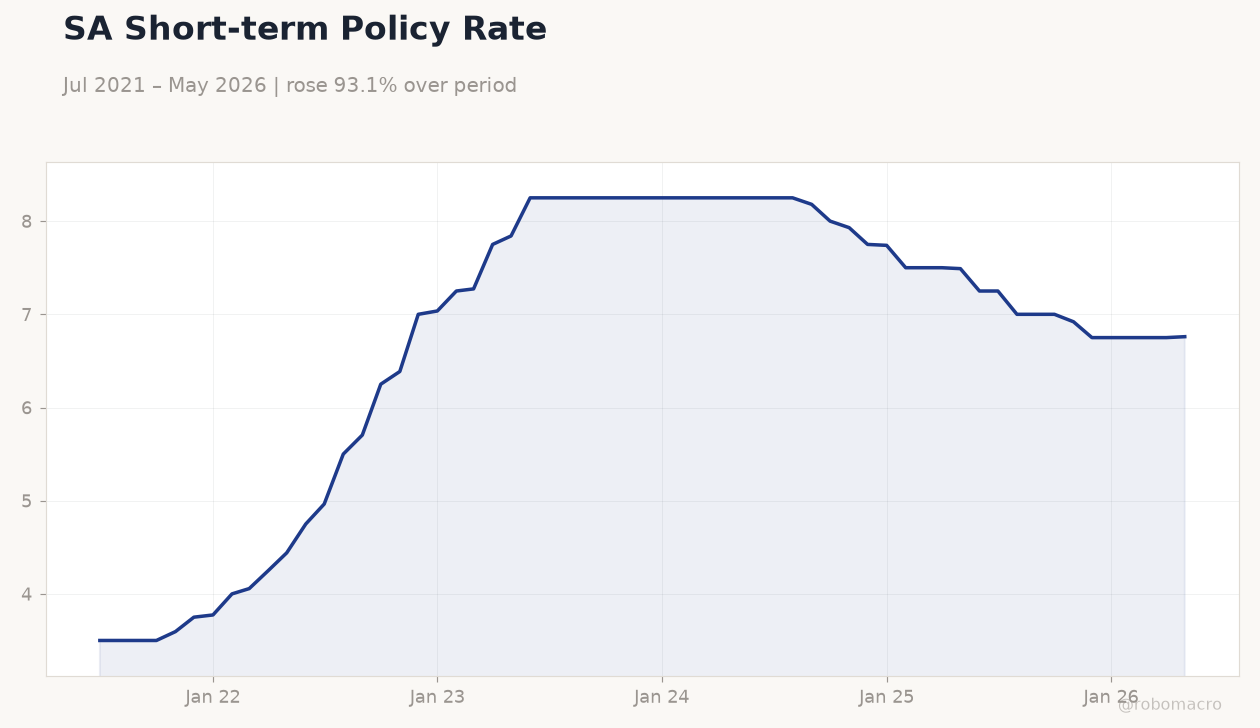

| South Africa Short-term Rate | 6.76% | +0.15% |

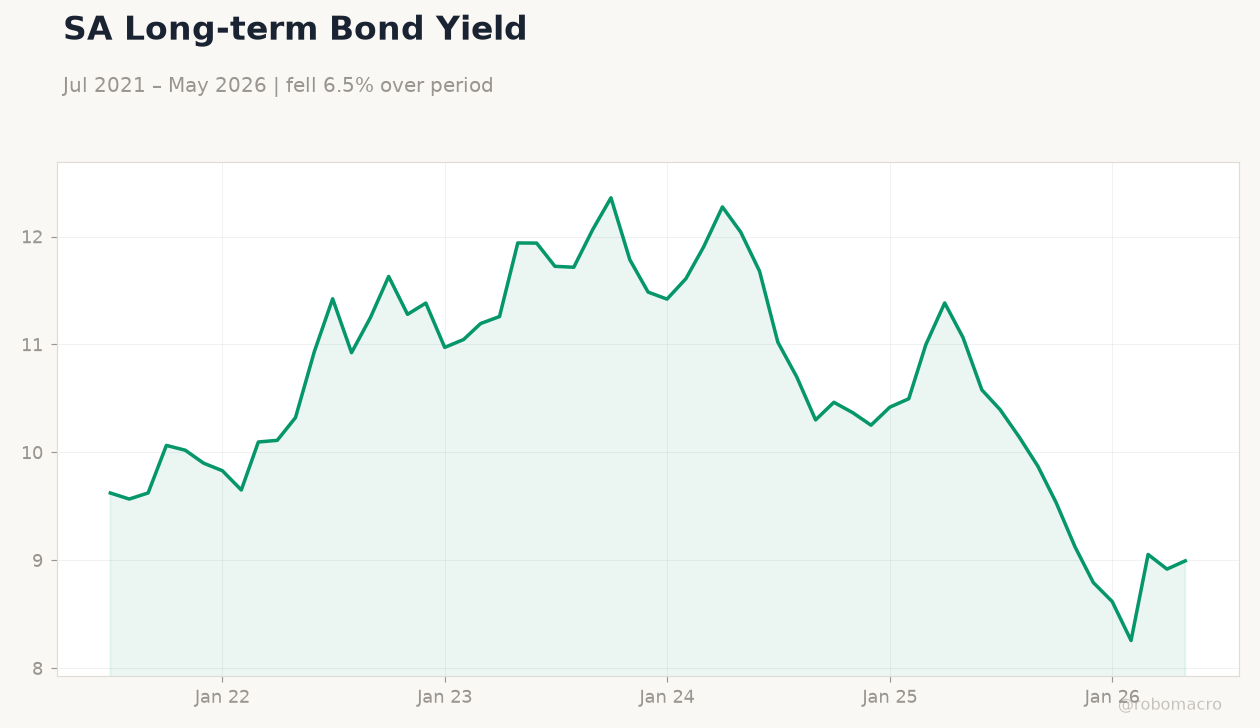

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SA Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

SA Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Rand falls 0.34% to 16.39 versus USD as firmer dollar and hawkish Fed signals dominate flows.

- JSE Top 40 drops 0.99% to 103,388.50 while mining stocks weigh on the index.

- Short-term rates stay at 6.76% as long-term yields climb 0.86% to 8.99%.

Yesterday's Recap

The rand weakened against the dollar to 16.39, extending losses as a stronger greenback and expectations of prolonged Fed tightening drew capital away from emerging markets. The JSE Top 40 closed 0.99% lower at 103,388.50, with platinum and gold prices declining 0.60% and 0.57% respectively and adding pressure to resource-heavy equities. Brent crude slipped 0.78% to 76.48, reflecting softer global demand signals.

Naspers advanced 0.60% to 84,500.00, providing a modest offset amid broader market weakness. South Africa’s short-term rate held steady at 6.76% while the long-term rate rose to 8.99%. Business confidence indicators declined, reinforcing rand softness ahead of leading indicator data.

Bitcoin fell 1.87% to 62,753.59, mirroring risk-off sentiment across asset classes.

The Day Ahead

Markets await South Africa’s leading business indicator data, which could further shape rand direction after yesterday’s decline. Consumer confidence figures are also due and are expected to reflect the impact of higher fuel prices. The absence of major data releases today leaves focus on external drivers, particularly US dollar moves and any Fed-related headlines.

Regional political tensions involving Nigeria may influence sentiment toward South African corporates with cross-border exposure. Traders will monitor commodity prices for any rebound in mining shares.

Other Economic Notes

Consumer confidence deteriorated in the second quarter as households faced elevated fuel costs linked to Middle East supply risks. The IMF’s new Africa director highlighted potential spillovers from regional conflicts into sub-Saharan growth and financing conditions. US funding cuts to HIV programs could reduce health outcomes and add fiscal pressure if domestic budgets must compensate.

MTN Group urged stronger continental integration to mitigate xenophobic incidents that threaten operations and investor perceptions.