South Africa Macro Daily(Beta Mode)

Rand Weakens to One-Month Low on Dollar Strength

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 101,534.00 | -1.79% |

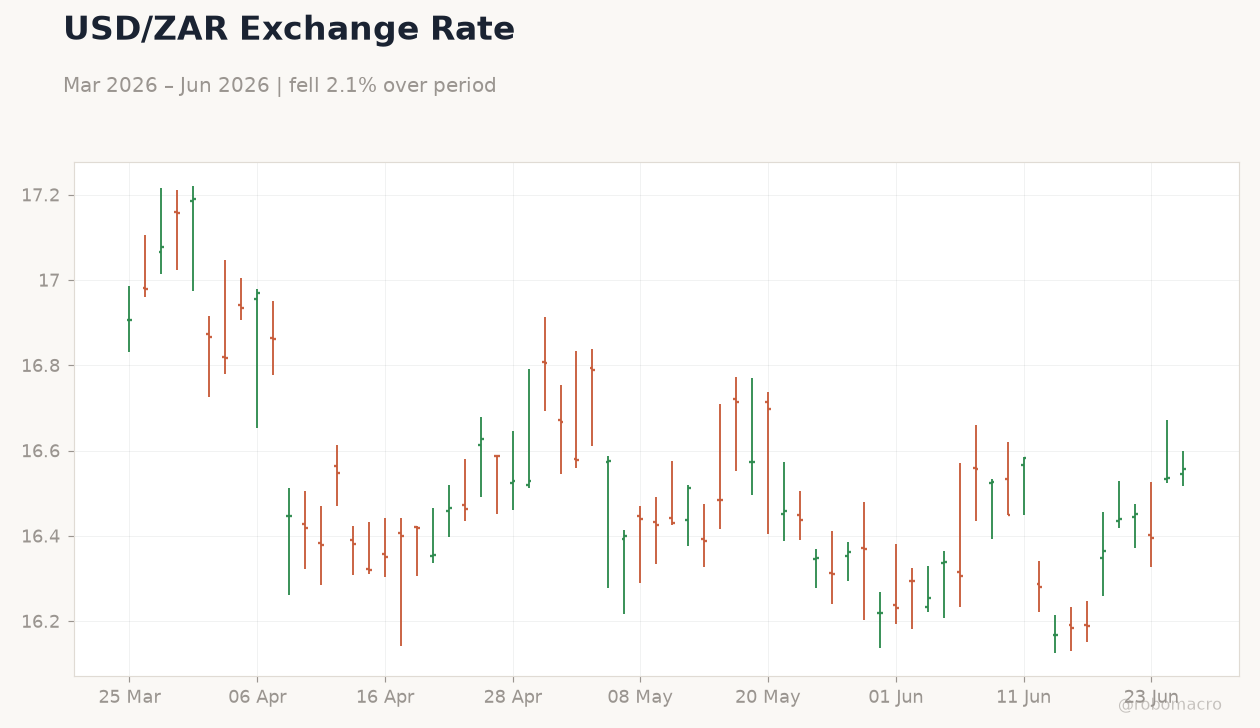

| USD/ZAR | 16.55 | +0.05% |

| EUR/ZAR | 18.80 | -0.09% |

| Platinum | 1,566.80 | -0.87% |

| Gold | 4,009.90 | +0.49% |

| Brent Crude | 72.66 | -1.46% |

| Naspers | 81,844.00 | +1.60% |

| Bitcoin | 61,428.49 | -1.98% |

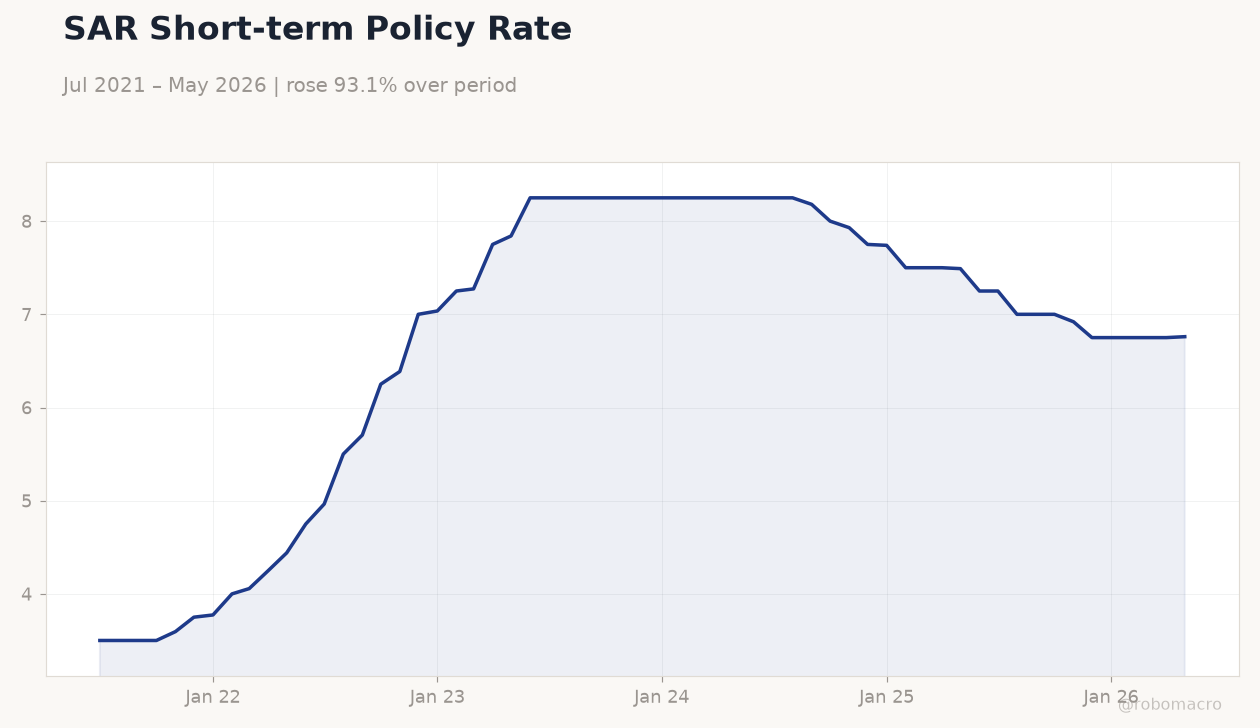

| South Africa Short-term Rate | 6.76% | +0.15% |

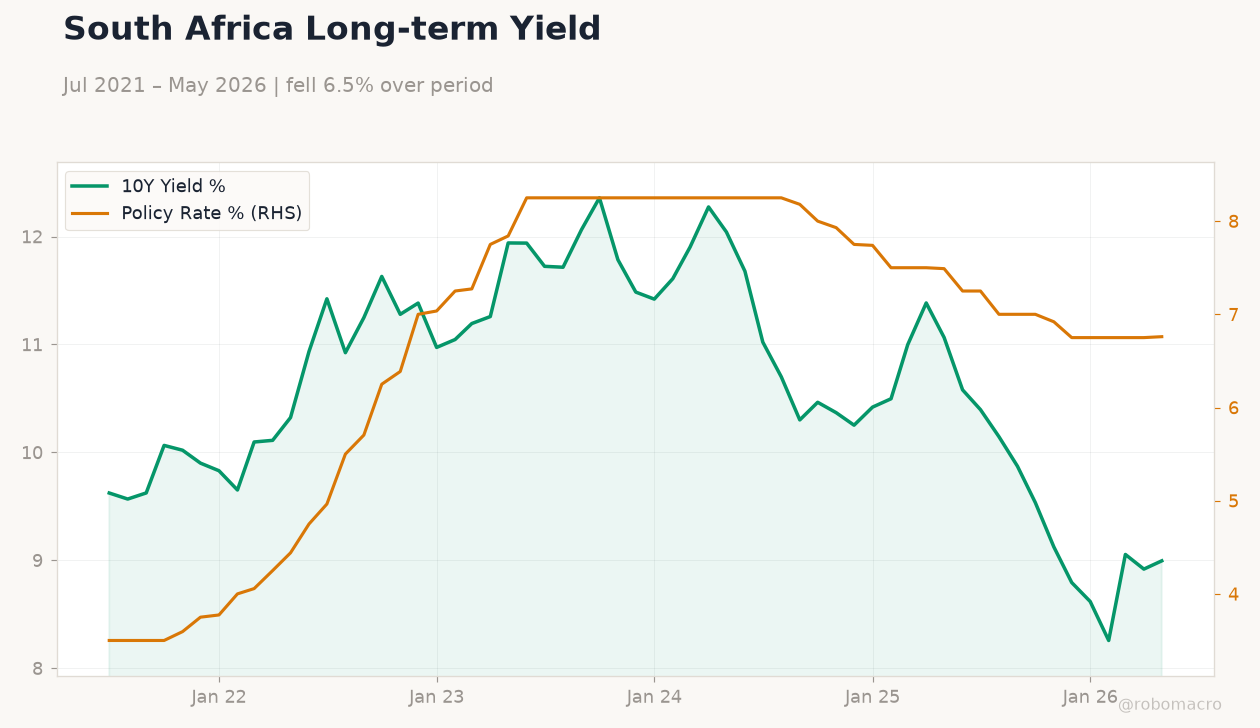

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SAR Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

SAR Short-term Policy Rate | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- USD/ZAR rises to 16.55 as rand weakens to over one-month low amid broad dollar gains against EM currencies.

- JSE Top 40 falls 1.79% to 101,534 while gold climbs 0.49% to 4,009.90, supporting mining names.

- SARB stresses lower inflation and fiscal reform as essential to cut borrowing costs and ease debt servicing.

Yesterday's Recap

The rand softened further, with USD/ZAR closing at 16.55 after a 0.05% gain and EUR/ZAR easing 0.09% to 18.80. The JSE Top 40 declined 1.79% to 101,534, pressured by global risk-off flows and weaker platinum prices that fell 0.87% to 1,566.80. Gold advanced 0.49% to 4,009.90, providing some support to precious-metal producers.

South Africa’s short-term rate edged up 0.15% to 6.76% while the long-term rate jumped 0.86% to 8.99%, steepening the curve. News that the SARB is tightening scrutiny on offshore payments to curb money laundering added to rand volatility. Broader EM currencies also faced headwinds from a firmer dollar, amplifying rand losses.

No major data releases occurred, leaving market moves driven by external flows and political headlines.

The Day Ahead

Markets face a data-light session with no scheduled releases from Stats SA or the SARB. Focus remains on ongoing diplomatic tensions with Nigeria that could affect investment flows from African partners. Traders will monitor any follow-up comments from SARB officials on offshore payment rules.

Global dollar direction and commodity prices will dictate rand and JSE moves. Platinum and gold futures will influence mining equity performance. Attention may also turn to Eskom’s generation outlook after recent load-shedding-free days.

Other Economic Notes

The SARB highlighted that sustained lower inflation combined with credible fiscal consolidation offers the clearest path to reduced borrowing costs. Persistent US funding cuts for HIV programmes risk raising fiscal pressures and health expenditure. Xenophobic incidents continue to prompt calls from Nigerian firms for investment boycotts, threatening regional capital inflows.

Platinum-group metal output guidance from major producers remains a key earnings driver for the JSE. Energy availability has improved but remains vulnerable to coal-plant reliability.