South Africa Macro Daily(Beta Mode)

JSE Climbs as Rand Firms Ahead of Trade Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 102,964.73 | +1.05% |

| USD/ZAR | 16.42 | -0.50% |

| EUR/ZAR | 18.72 | -0.13% |

| Platinum | 1,618.70 | -0.75% |

| Gold | 4,076.90 | -0.04% |

| Brent Crude | 72.98 | +1.38% |

| Naspers | 79,953.00 | -2.52% |

| Bitcoin | 59,985.67 | +0.76% |

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

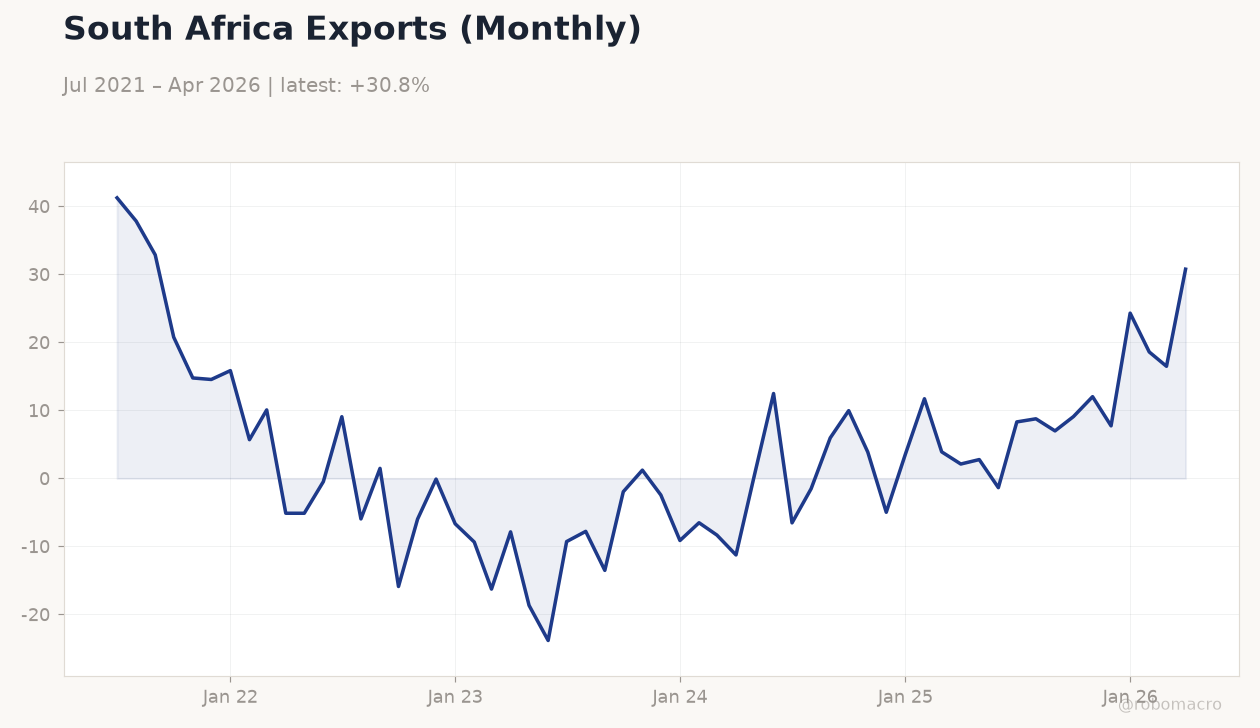

South Africa Exports (Monthly) | Type: macro_line | Exports (ZAR mn): 30.76 (2026-04-01) | Range: -23.83–41.25 | Trend(6pt): 41.25,1.473,1.213,3.546,16.48,30.76

South Africa Exports (Monthly) | Type: macro_line | Exports (ZAR mn): 30.76 (2026-04-01) | Range: -23.83–41.25 | Trend(6pt): 41.25,1.473,1.213,3.546,16.48,30.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-30) | |||

| Trade Balance | 15,160m | - | 04:00 |

- JSE Top 40 rises 1.05% to 102,964.73 while USD/ZAR drops 0.50% to 16.42.

- South Africa Short-term Rate holds at 6.76% and Long-term Rate reaches 8.99%.

- Trade Balance due tomorrow with prior print at 15.16 billion rand.

Yesterday's Recap

South African markets posted gains on 28 June with the JSE Top 40 closing 1.05% higher at 102,964.73. The rand strengthened, sending USD/ZAR down 0.50% to 16.42 and EUR/ZAR 0.13% lower to 18.72. Brent crude advanced 1.38% to 72.98 while platinum fell 0.75% to 1,618.70 and gold edged 0.04% lower to 4,076.90.

Naspers declined 2.52% to 79,953.00 even as Bitcoin rose 0.76% to 59,985.67. The South Africa Short-term Rate increased 0.15% to 6.76% and the Long-term Rate climbed 0.86% to 8.99%. No major data releases occurred yesterday, leaving price action driven by external USD moves and commodity flows.

The absence of fresh inflation or credit figures kept front-end yields stable ahead of the monthly trade print.

The Day Ahead

The Trade Balance for May releases at 04:00 ET tomorrow, with the prior surplus at 15.16 billion rand. Markets will scrutinise export volumes given ongoing mining output adjustments. No other high-impact South African indicators are scheduled for 29 June.

Attention will also turn to any follow-up comments from National Treasury on the 4.5% deficit target. Positioning ahead of the print is expected to keep USD/ZAR in a tight range near 16.40.

Other Economic Notes

Eskom’s return to stage-2 load-shedding after a Medupi outage highlights persistent energy supply risks for mining and manufacturing. Glencore’s 12% cut to 2026 coal guidance adds downside pressure to export earnings. Finance Minister Godongwana’s confirmation of unchanged borrowing plans supports the fiscal trajectory but leaves little room for additional stimulus.

Broader credit growth remains subdued, limiting domestic demand impulses into the second half of the year.

Global Macro News

A firmer US dollar continues to cap rand gains despite yesterday’s modest USD/ZAR decline. News flow on a potential digital rand draws attention to future payment-system modernisation without immediate market impact. Regional export data from Nigeria to Southern Africa reaching N1tn underscores shifting intra-African trade corridors that could support SA port volumes.

<i>↓ p.2</i>