South Africa Macro Daily(Beta Mode)

JSE Climbs, Rand Firms Ahead of Trade Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 102,047.88 | +0.21% |

| USD/ZAR | 16.42 | -0.35% |

| EUR/ZAR | 18.72 | -0.18% |

| Platinum | 1,585.70 | +0.71% |

| Gold | 4,041.00 | +0.46% |

| Brent Crude | 73.42 | +0.37% |

| Naspers | 83,897.00 | +4.93% |

| Bitcoin | 59,394.72 | -1.24% |

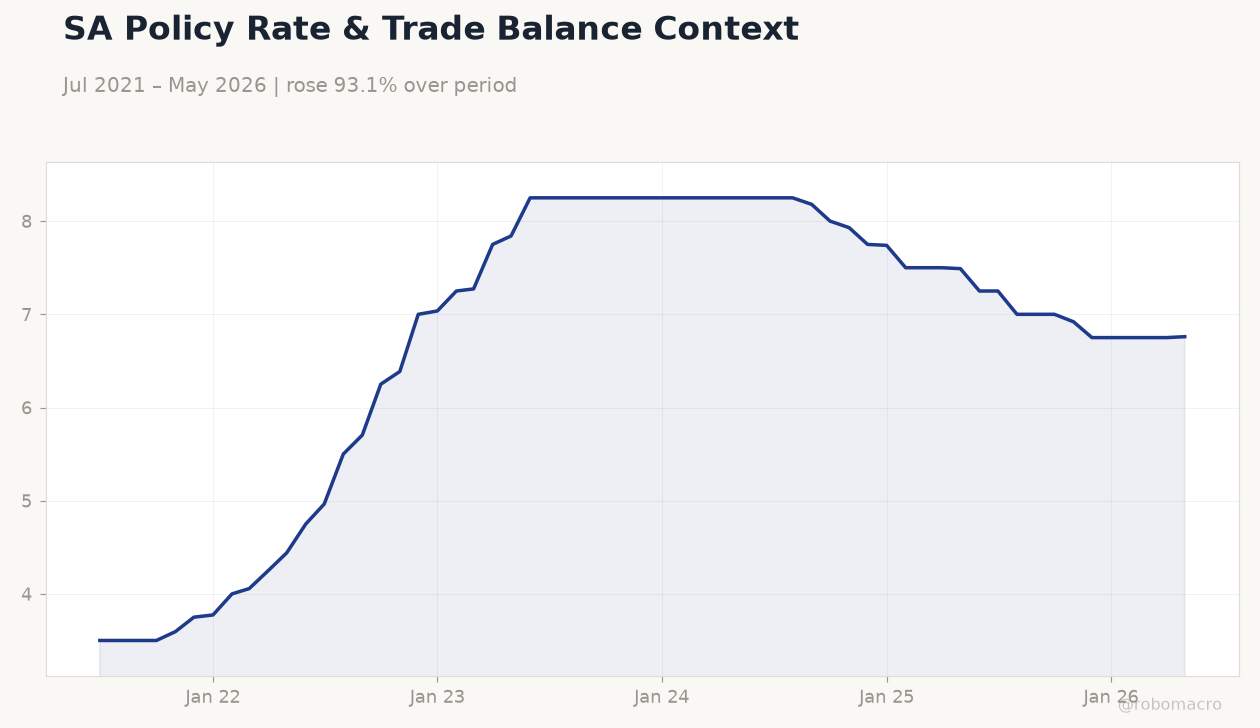

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

SA Policy Rate & Trade Balance Context | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

SA Policy Rate & Trade Balance Context | Type: macro_line | Policy Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,5.705,8.25,7.74,6.75,6.76

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 15,160m | - | 04:00 |

- JSE Top 40 rises 0.21% to 102,047.88 while Naspers jumps 4.93%.

- USD/ZAR falls 0.35% to 16.42 as short-term rates edge up 0.15% to 6.76%.

- Trade Balance release at 04:00 ET draws focus amid mounting anti-migrant tensions.

Yesterday's Recap

South African markets closed higher with the JSE Top 40 advancing 0.21% to 102,047.88, driven by platinum and gold gains of 0.71% and 0.46%. The rand strengthened against both the dollar and euro, with USD/ZAR dropping to 16.42 and EUR/ZAR to 18.72. Long-term yields climbed 0.86% to 8.99% while short-term rates reached 6.76%.

No economic data prints occurred, leaving price action dominated by resource sector momentum and global commodity moves. Heavy security deployments preceded Tuesday's anti-migrant deadline, prompting evacuations of foreign nationals and warnings from President Ramaphosa for lawful protests only. Bitcoin declined 1.24% to 59,394.72, offering little offset to local equity gains.

The Day Ahead

The Trade Balance print at 04:00 ET represents the sole scheduled release and carries medium market impact. Analysts will assess whether the prior 15.16 billion rand surplus narrows or widens under current commodity prices. No SARB speakers or MPC minutes are slated.

Focus will remain on external sector resilience given rand strength and Brent crude at 73.42. Broader attention may shift to any follow-through from today's protest deadline and its potential effect on foreign investor sentiment.

Other Economic Notes

Reports indicate the SARB is moving toward ending the prime interest rate framework, shifting emphasis to repo-linked benchmarks. Xenophobic tensions and planned rallies have triggered fresh Nigerian evacuations and Malawian repatriation queues at border camps. Domestic pension funds are absorbing the full June bond issuance, reducing reliance on external financing.

Load-shedding remains contained at stage 2 over the weekend with expectations of further improvement through winter.

Global Macro News

Gold advanced 0.46% to 4,041.00 and platinum rose 0.71% to 1,585.70, supporting South African mining equities. Brent crude gained 0.37% to 73.42 on supply discipline signals. Bitcoin's 1.24% decline to 59,394.72 reflected broader risk-off flows.

The rand's outperformance versus the dollar occurred against softer US data that tempered rate expectations globally. <i>↓ p.2</i>