South Africa Macro Daily(Beta Mode)

Trade Deficit Emerges Amid Protest Volatility

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 101,936.10 | +0.10% |

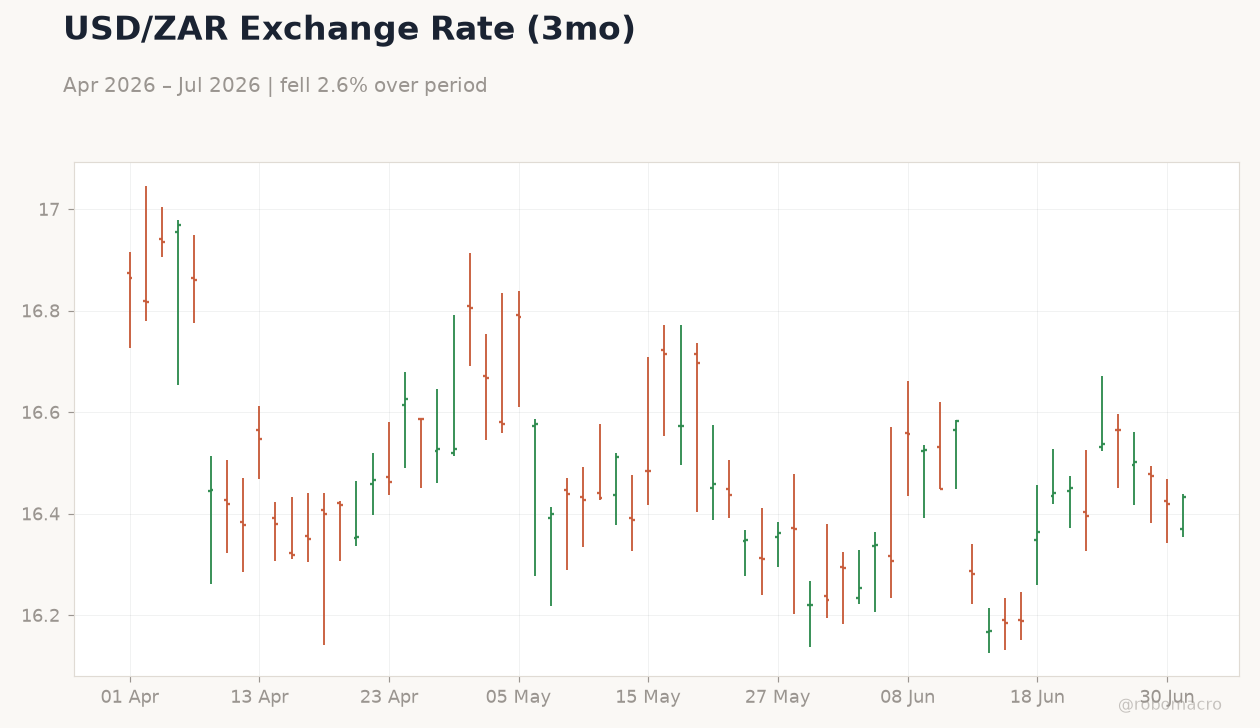

| USD/ZAR | 16.42 | -0.03% |

| EUR/ZAR | 18.73 | -0.13% |

| Platinum | 1,549.10 | -0.07% |

| Gold | 3,988.60 | -0.85% |

| Brent Crude | 73.18 | +0.36% |

| Naspers | 83,897.00 | +4.93% |

| Bitcoin | 59,064.12 | -1.79% |

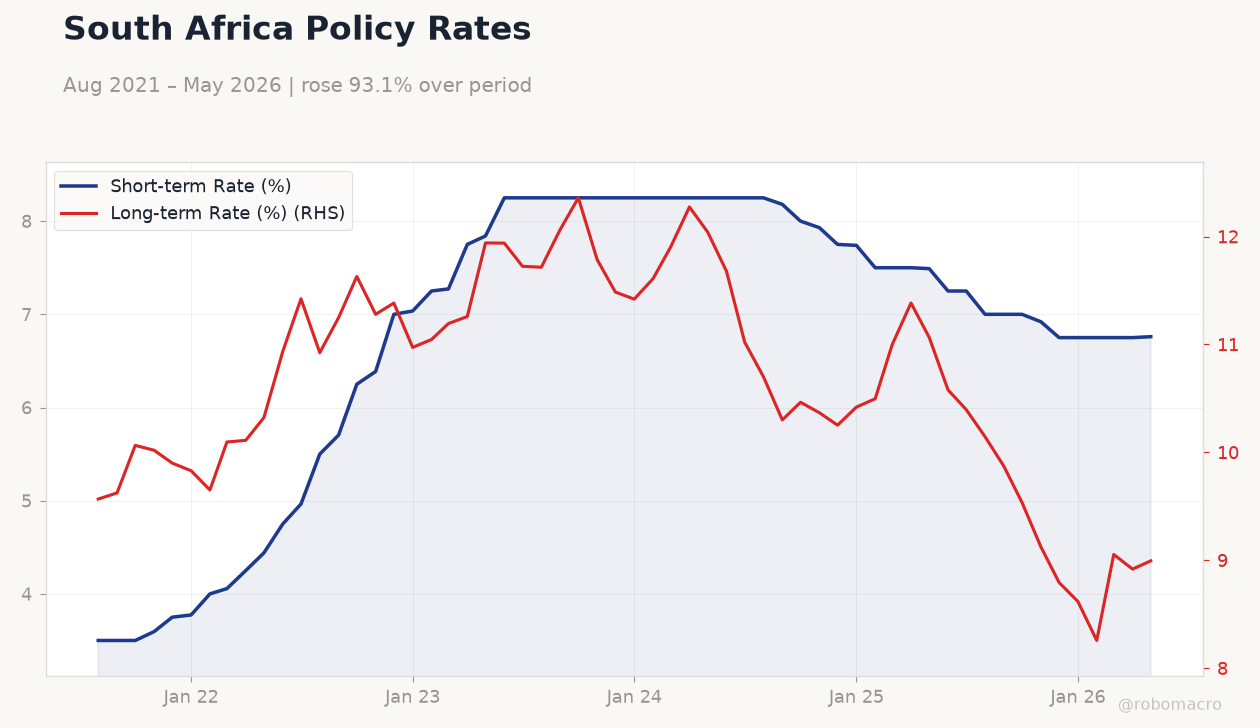

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 15,160m | - | -1,790m |

South Africa Policy Rates | Type: macro_line | Short-term Rate (%): 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,6.25,8.25,7.5,6.75,6.76 | Long-term Rate (%): 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.568,11.63,11.49,10.5,8.918,8.995

South Africa Policy Rates | Type: macro_line | Short-term Rate (%): 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,6.25,8.25,7.5,6.75,6.76 | Long-term Rate (%): 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.568,11.63,11.49,10.5,8.918,8.995

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South Africa’s trade balance swung to a R1.79bn deficit from a R15.16bn surplus, highlighting external weakness.

- JSE Top 40 rose 0.10% to 101,936.10 while USD/ZAR eased 0.03% to 16.42 on contained risk appetite.

- Anti-migrant protests triggered heavy police deployment and rand trading surges as SARB noted external volatility.

Yesterday's Recap

South Africa’s May trade balance printed a sharp R1.79bn deficit, reversing the prior R15.16bn surplus and underscoring softer export momentum. The JSE Top 40 advanced 0.10% to 101,936.10, supported by Naspers gains of 4.93%. USD/ZAR closed 0.03% firmer at 16.42 while the long-term government bond yield climbed 0.86% to 8.99%.

Short-term rates edged 0.15% higher to 6.76%, aligning with the prevailing SARB repo level. Platinum held near $1,549 amid modest commodity support, whereas gold fell 0.85% to $3,988.60. Anti-migrant marches unfolded across major cities with police units deployed to curb violence risks.

SARB officials highlighted that Middle East conflict had lifted rand turnover but left domestic growth largely unscathed.

The Day Ahead

No scheduled data releases appear on the calendar for 1 July or 2 July. Markets will monitor ongoing protest developments and any follow-through evacuation flows. Inflation expectations data due later this week will shape positioning ahead of the next MPC meeting.

The SARB Quarterly Bulletin may offer updated credit and balance-sheet detail without altering near-term policy signals. Participants will also track Eskom plant availability for signs of sustained load-shedding relief.

Other Economic Notes

Private-sector credit growth slowed in May, adding pressure on bank margins and rand liquidity. PwC’s 2026 outlook points to modest GDP expansion tempered by structural constraints and fiscal consolidation at a 4.5% deficit target. Anti-immigration tensions risk dampening foreign direct investment and tourism receipts in the second half.

Mining output showed resilience in April, led by platinum-group metals, supporting export revenues despite the trade swing.

Global Macro News

Brent crude rose 0.36% to $73.18 on OPEC+ discipline signals, offering marginal support to the terms of trade. Bitcoin declined 1.79% to $59,064, weighing on broader risk sentiment across emerging markets. SARB statements noted that Middle East conflict had increased rand volatility without derailing domestic inflation or growth paths.

<i>↓ p.2</i>