South Africa Macro Daily(Beta Mode)

Rand Holds as Trade Balance Swings to Deficit

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| JSE Top 40 | 101,428.13 | +0.15% |

| USD/ZAR | 16.37 | -0.05% |

| EUR/ZAR | 18.68 | -0.06% |

| Platinum | 1,624.20 | +2.22% |

| Gold | 4,088.30 | +0.49% |

| Brent Crude | 70.86 | -0.99% |

| Naspers | 82,062.00 | -2.19% |

| Bitcoin | 60,393.59 | +0.65% |

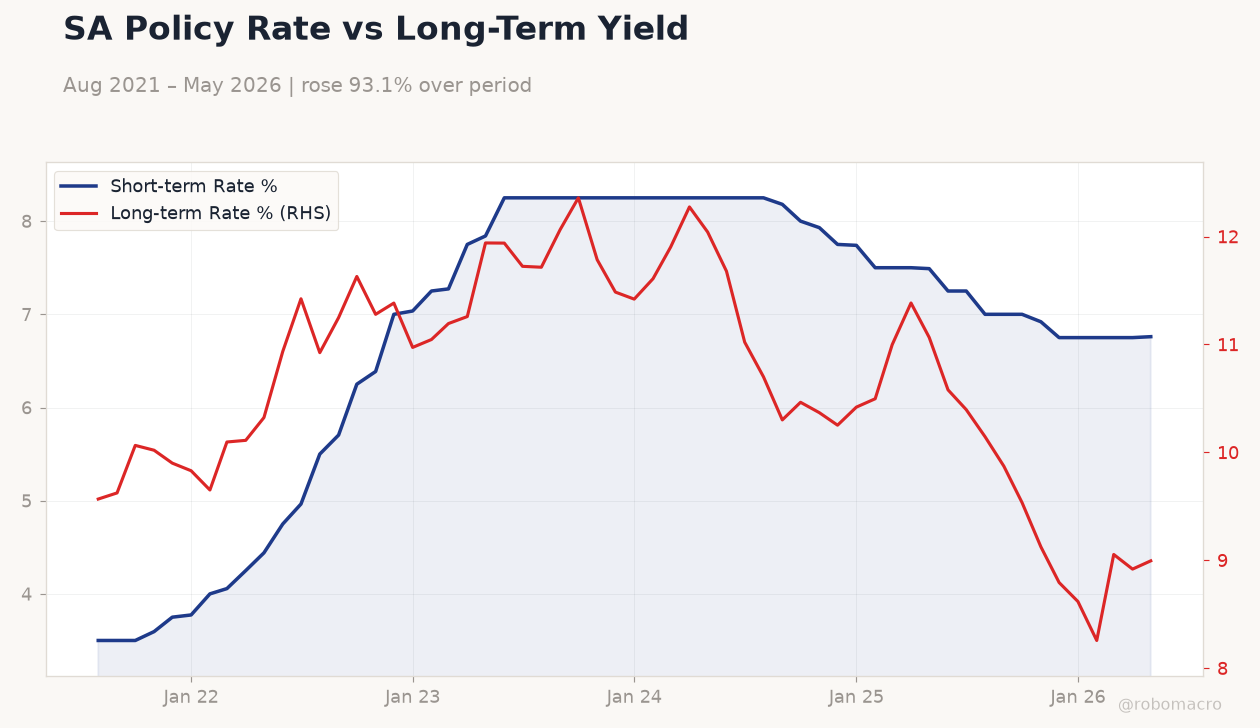

| South Africa Short-term Rate | 6.76% | +0.15% |

| South Africa Long-term Rate | 8.99% | +0.86% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 14,430m | - | -1,790m |

SA Policy Rate vs Long-Term Yield | Type: macro_line | Short-term Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,6.25,8.25,7.5,6.75,6.76 | Long-term Rate %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.568,11.63,11.49,10.5,8.918,8.995

SA Policy Rate vs Long-Term Yield | Type: macro_line | Short-term Rate %: 6.76 (2026-05-01) | Range: 3.5–8.25 | Trend(6pt): 3.5,6.25,8.25,7.5,6.75,6.76 | Long-term Rate %: 8.995 (2026-05-01) | Range: 8.257–12.36 | Trend(6pt): 9.568,11.63,11.49,10.5,8.918,8.995

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- South Africa’s trade balance flipped to a ZAR 1.79 bn deficit in May from a ZAR 14.43 bn surplus, highlighting softening external demand.

- JSE Top 40 edged 0.15 % higher to 101,428 while USD/ZAR eased 0.05 % to 16.37 amid firmer platinum and gold prices.

- SARB short-term rate stood at 6.76 % after a 15 bp rise; Governor Kganyago flagged upside risks to inflation expectations above the 3 % target.

Yesterday's Recap

South Africa recorded a sharp reversal in external trade, posting a ZAR 1.79 bn deficit against the prior ZAR 14.43 bn surplus. The JSE Top 40 advanced 0.15 % to close at 101,428.13, supported by a 2.22 % gain in platinum to USD 1,624.20 and a 0.49 % rise in gold. USD/ZAR finished 0.05 % lower at 16.37 while the long-term government bond yield climbed 86 bp to 8.99 %.

Brent crude declined 0.99 % to USD 70.86, weighing on energy-related names. Naspers fell 2.19 % despite the broader equity advance. Short-term rates rose 15 bp to 6.76 %, reflecting the market’s reassessment of policy direction.

The Day Ahead

No scheduled South African data releases are listed for 2 July. Markets will monitor global commodity flows and any follow-up comments from SARB officials on inflation risks. Positioning in USD/ZAR remains light after month-end flows, leaving the currency sensitive to external drivers.

Platinum and gold prices will continue to influence JSE mining stocks and rand sentiment. Attention also turns to any updates on load-shedding schedules from Eskom that could affect industrial output readings later in the week.

Other Economic Notes

Rising anti-migrant protests have triggered the departure of roughly 25,000 foreign nationals, disrupting retail and logistics operations near Durban. South Africa began commercial plum exports to China, offering a modest boost to agricultural revenues. Persistent housing shortages and infrastructure gaps remain structural drags on domestic demand.

Global Macro News

Brent crude’s 0.99 % decline to USD 70.86 reflected softer global demand signals despite OPEC+ supply discipline. Stronger platinum and gold prices provided a tailwind for South African resource exports and the rand. US policy uncertainty under the Trump administration continues to strain bilateral trade and investment ties with Pretoria.

Nigerian repatriation flights underscore regional spill-overs from South African social tensions that could dampen investor appetite. <i>↓ p.2</i>