Turkey Macro Daily(Beta Mode)

BIST Rises Amid Recovery Hopes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

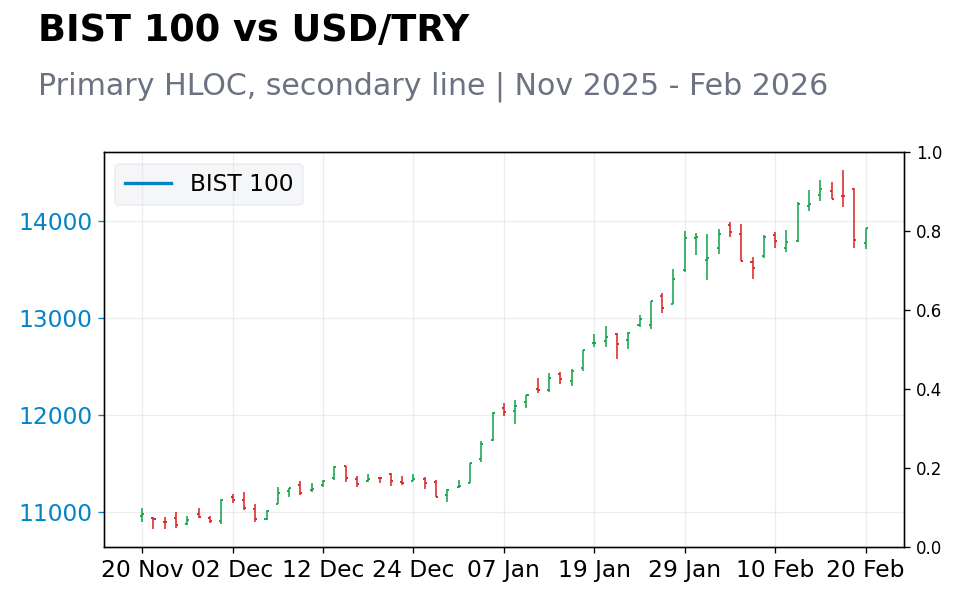

| BIST 100 | 13,934.10 | +0.94% |

| USD/TRY | 43.83 | -0.02% |

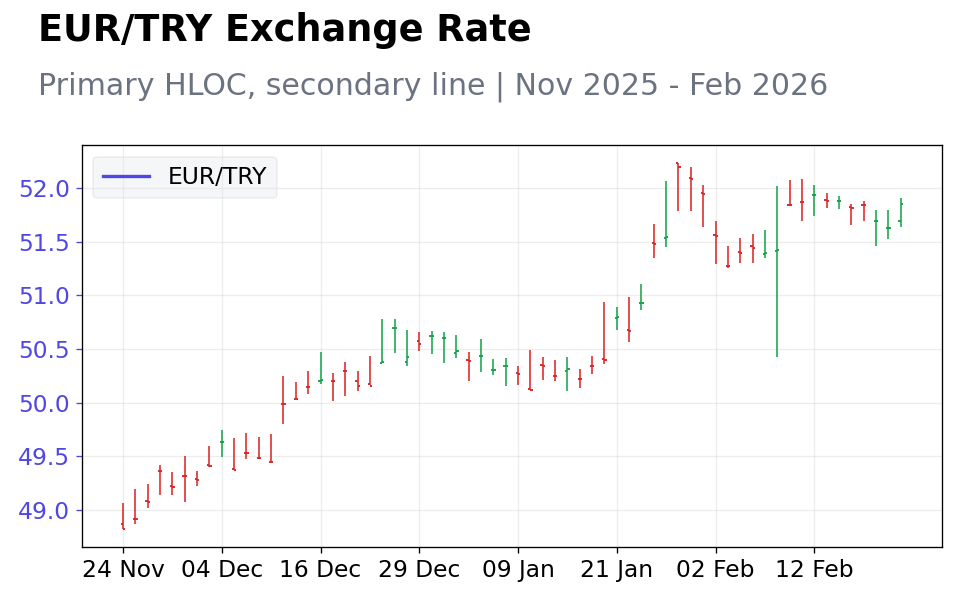

| EUR/TRY | 51.80 | +0.33% |

| GBP/TRY | 59.23 | +0.32% |

| Gold (TRY) | 5,183.00 | +2.45% |

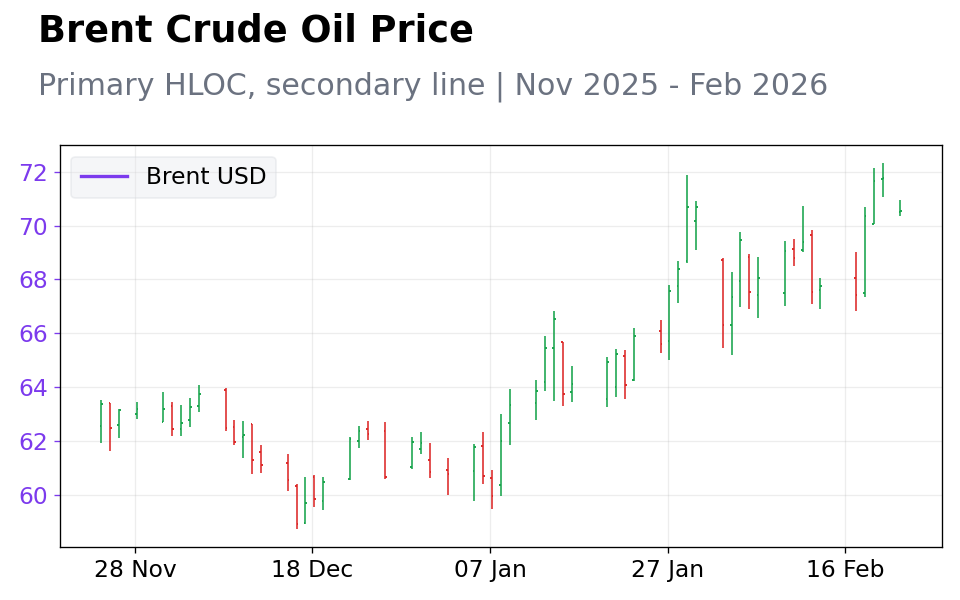

| Brent Crude | 70.53 | -1.71% |

| EUR/USD | 1.18 | +0.47% |

| Bitcoin | 64,955.29 | -4.48% |

| Turkey 2Y Govt Yield | - | - |

| Turkey 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BIST 100 climbed 0.94% to 13,934.10, fueled by optimism for 2026 stock market rebound after flat 2025.

- USD/TRY slipped 0.02% to 43.83, showing mild lira firmness, while EUR/TRY and GBP/TRY gained 0.33% and 0.32%.

- Gold in TRY jumped 2.45% to 5,183.00 on haven demand; Brent crude dropped 1.71% to 70.53.

Yesterday's Recap

On February 21, Turkish markets exhibited strength, with the BIST 100 index advancing 0.94% to 13,934.10, supported by reports of Borsa Istanbul's strongest January in 29 years, sparking hopes for a 2026 recovery following 2025's lackluster performance. The USD/TRY rate eased 0.02% to 43.83, suggesting slight lira appreciation in quiet trading without key data, though EUR/TRY rose 0.33% to 51.80 and GBP/TRY increased 0.32% to 59.23 due to strength in those currencies. Gold in TRY terms surged 2.45% to 5,183.00, reflecting global safe-haven buying, while Brent crude fell 1.71% to 70.53, potentially alleviating Turkey's energy import pressures and aiding the current account.

Bond yield data was unavailable, aligning with recent caution on inflation dynamics. The session focused on equity upside, with sectors like banking driving gains amid low volatility. Bitcoin declined 4.48% to 64,955.29, indicating risk aversion that helped contain lira swings.

These developments tie into improving external balances, as softer oil prices counter deficit vulnerabilities.

The Day Ahead

February 22 features no planned Turkish economic data, giving markets time to absorb recent advances and track international signals for lira guidance. Eyes will be on potential CBRT updates regarding reserves or liquidity, amid efforts to tame inflation. Informal metrics, such as tourism trends or export activity, may offer clues to external sector strength in the absence of releases.

Sentiment could hinge on U.S. bond yields or emerging market forex moves, influencing TRY pairs. Volatility should remain subdued unless Middle East developments affect oil, impacting import expenses.

Traders ought to monitor for equity fluctuations in BIST if global stocks shift.

Other Economic Notes

Turkey's trade position is showing signs of progress, with declining Brent prices lightening the energy import load and contributing to a narrower current account deficit seen in late 2025 figures. Maintaining fiscal restraint is essential, as infrastructure outlays might fuel inflation without offsetting tourism revenues. (cont...)