UK Macro Daily(Beta Mode)

UK Housing Data Beats Expectations

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,812.63 | -0.53% |

| FTSE 100 | 9,701.80 | -0.01% |

| UK Natural Gas | 2.85 | +1.23% |

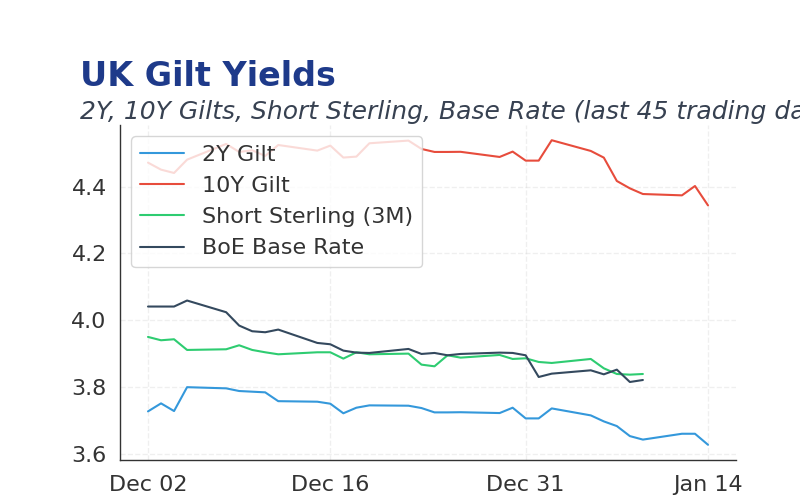

| 2 Year Gilt | 3.73 | -2 bps |

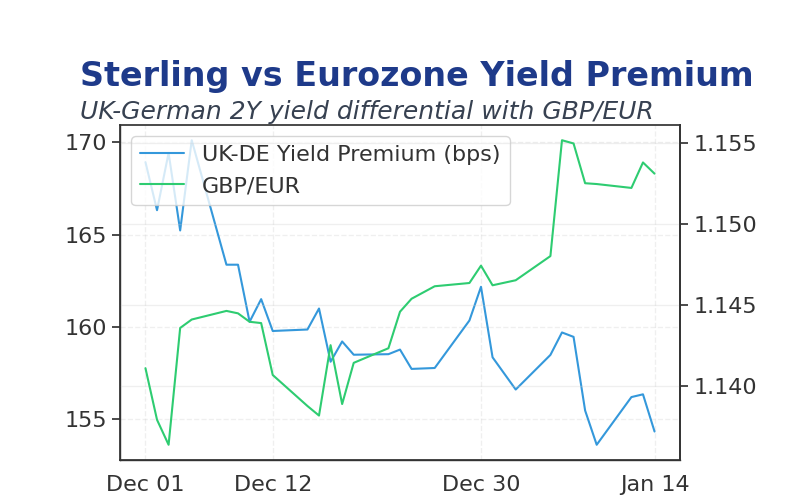

| 10 Year Gilt | 4.47 | -1 bps |

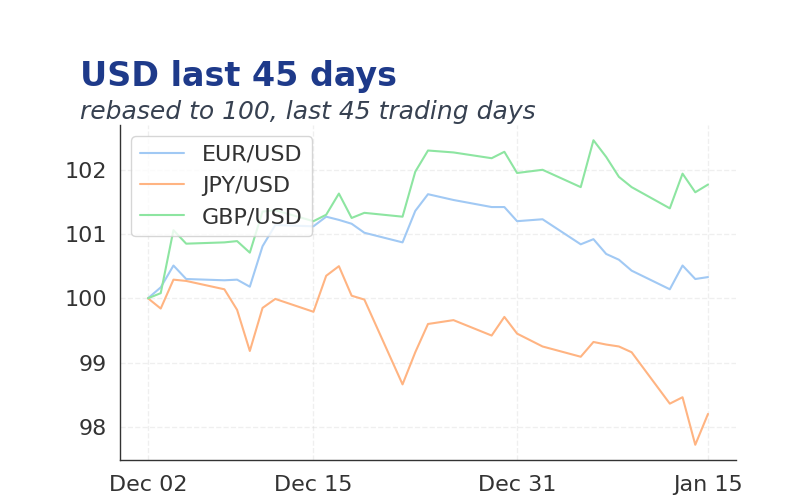

| GBP/USD | 1.324 | +0.23% |

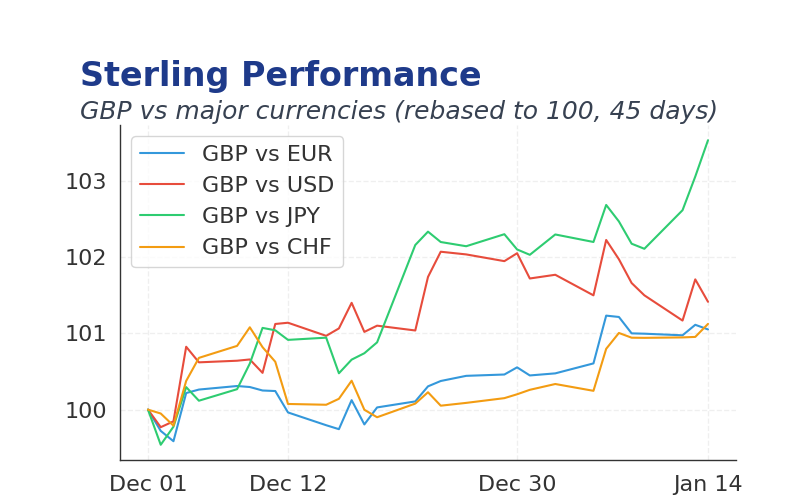

| GBP/EUR | 1.14 | +0.04% |

| GBP/JPY | 205.96 | +0.04% |

| Brent Oil | 86.45 | -0.12% |

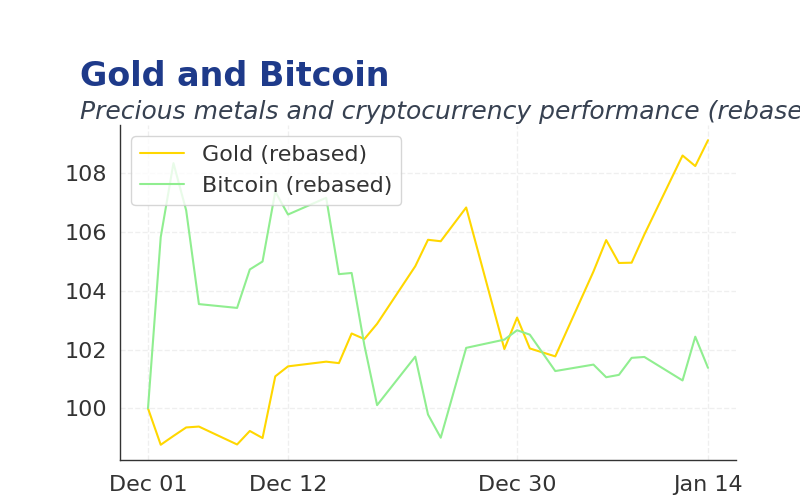

| Gold ($) | 2,456.70 | +0.85% |

| Bitcoin ($) | 93,901.07 | +2.84% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Nationwide Housing Prices m/m | 0.20 | 0 | 0.30 |

| Nationwide Housing Prices y/y | 2.40 | 1.40 | 1.80 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Constr PMI | 44.10 | 44.30 | 09:30 |

- Nationwide housing prices rose 0.3% m/m, beating consensus expectations and signaling resilient demand despite high borrowing costs.

- Today's S&P Global Construction PMI could reveal further weakness in UK building activity, impacting investor sentiment on economic recovery.

- BoE's cutting cycle may slow if data underscores persistent inflationary pressures from global energy costs.

Yesterday's Recap

Nationwide housing prices increased 0.3% month-on-month, surpassing the consensus of 0%, with the year-on-year rate at 1.8% below expectations of 1.4%.

This beat supported UK equities modestly, but overall markets traded calmly without major catalysts.

No BoE speeches occurred, leaving focus on data surprises amid ongoing rate cut expectations.

The Day Ahead

The S&P Global Construction PMI at 09:30 is expected to show continued contraction at around 44.3, potentially below Friday's 44.1 reading.

Investors will watch for implications on UK GDP growth and Sterling stability.

No BoE speeches are scheduled, allowing data to drive sentiment ahead of year-end policy decisions.

Other Economic Notes

UK housing prices remain elevated despite affordability challenges, per Nationwide data.

Brexit-related trade disruptions continue to weigh on manufacturing output in Northern Ireland.

Energy costs from global tensions sustain inflationary pressures, complicating disinflation efforts.