UK Macro Daily(Beta Mode)

UK Housing Eyes Soft Landing

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,829.37 | +0.25% |

| FTSE 100 | 9,710.87 | +0.19% |

| UK Natural Gas | Data Unavailable | Data Unavailable |

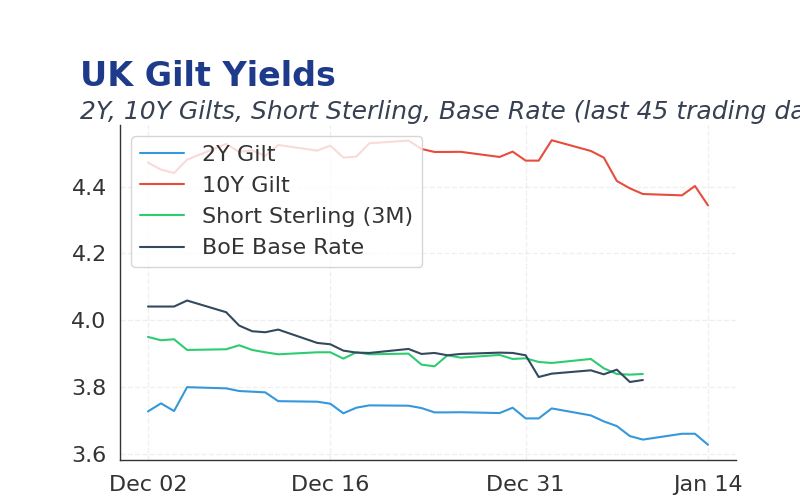

| 2 Year Gilt | 3.73 | -2 bps |

| 10 Year Gilt | 4.44 | +0 bps |

| GBP/USD | 1.333 | -0.12% |

| GBP/EUR | 1.15 | +0.07% |

| GBP/JPY | 206.73 | -0.23% |

| Brent Oil | Data Unavailable | Data Unavailable |

| Gold ($) | Data Unavailable | Data Unavailable |

| Bitcoin ($) | 92,221.98 | -1.32% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Halifax House Pr Index m/m | 0.60 | 0.40 | 07:00 |

| Halifax House Pr Index y/y | 1.90 | - | 07:00 |

- FTSE 100 edged up 0.19% amid calm trading, with no major economic surprises influencing sentiment.

- Today's Halifax House Price Index release could signal housing market resilience or weakness.

- BoE cutting cycle endures, with markets pricing slower cuts as disinflation supports gradual easing.

Yesterday's Recap

UK equities traded calmly, with FTSE 100 rising 0.19% to 9710.87 on steady sentiment lacking major catalysts.

Gilt yields showed minimal shifts, 2-year down 2bps to 3.73% and 10-year flat at 4.44%, maintaining expectations for BoE cuts.

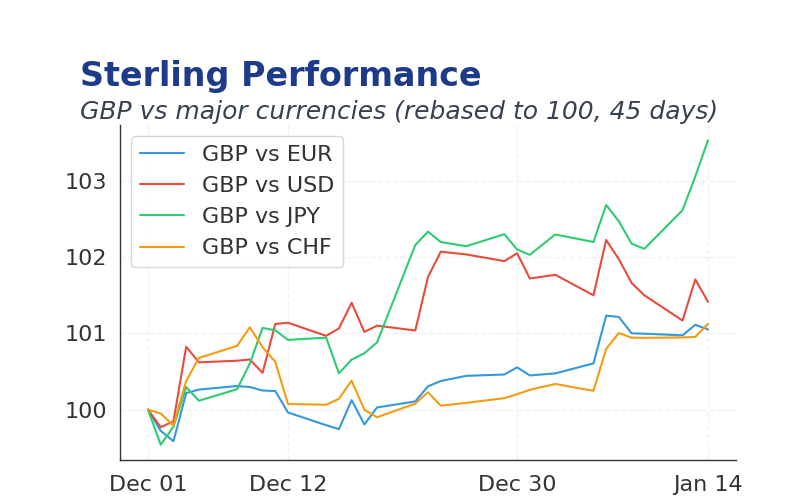

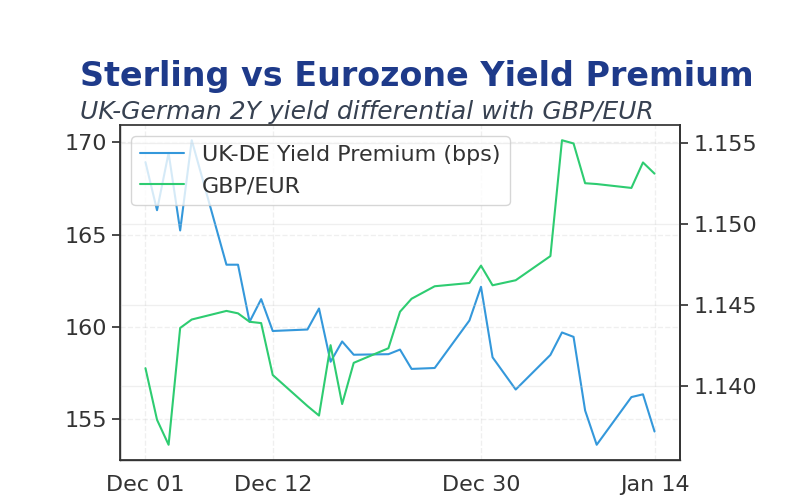

Sterling moved modestly, GBP/USD down 0.12% to 1.333 and GBP/EUR up 0.07% to 1.15, amid low volatility.

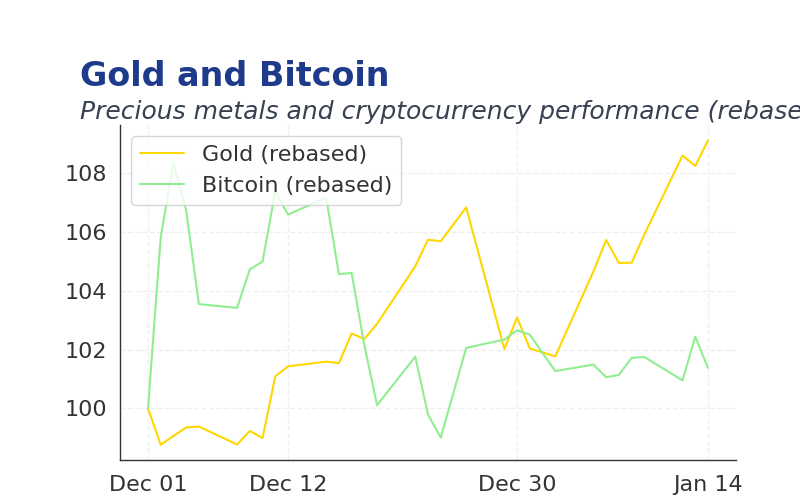

Commodities were quiet, with Brent oil unchanged, gold not reported, and Bitcoin down 1.32% to 92221.98 without significant drivers.

No BoE speeches occurred, leaving focus on ongoing fiscal debates.

The Day Ahead

Investors await the Halifax House Price Index at 07:00, with m/m consensus at 0.4% versus prior 0.6% and y/y at unknown versus 1.9%, potentially impacting Gilt yields if growth signals emerge.

No other UK data or BoE events are scheduled, shifting attention to European developments for spillover.

Markets may react modestly to housing data, with surprises tilting toward faster or slower rate cut pricing.

Other Economic Notes

Slow logistics network progress is hindering UK growth by increasing congestion costs and delaying supply chains.

Dependency on cars continues to clog Britain, exacerbating economic inefficiencies.