UK Macro Daily(Beta Mode)

UK Housing Beats, Cuts Steady

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,886.68 | +0.67% |

| FTSE 100 | 9,703.16 | +0.49% |

| UK Natural Gas | 4.59 | +0.46% |

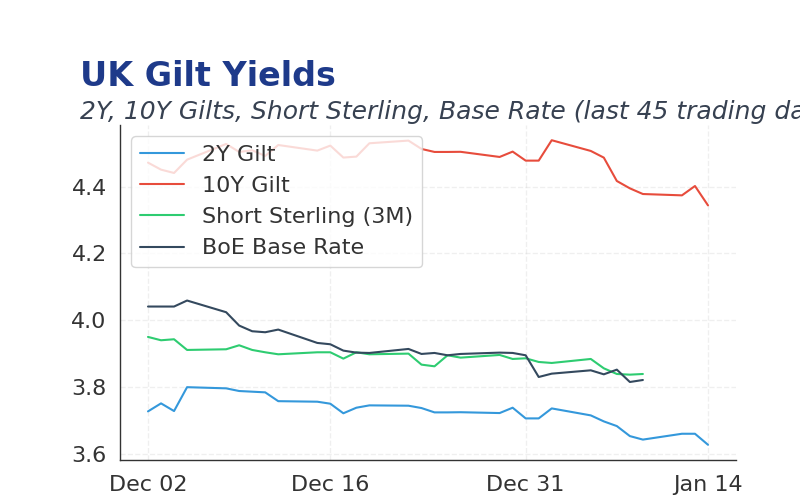

| 2 Year Gilt | 3.78 | +0 bps |

| 10 Year Gilt | 4.49 | -1 bps |

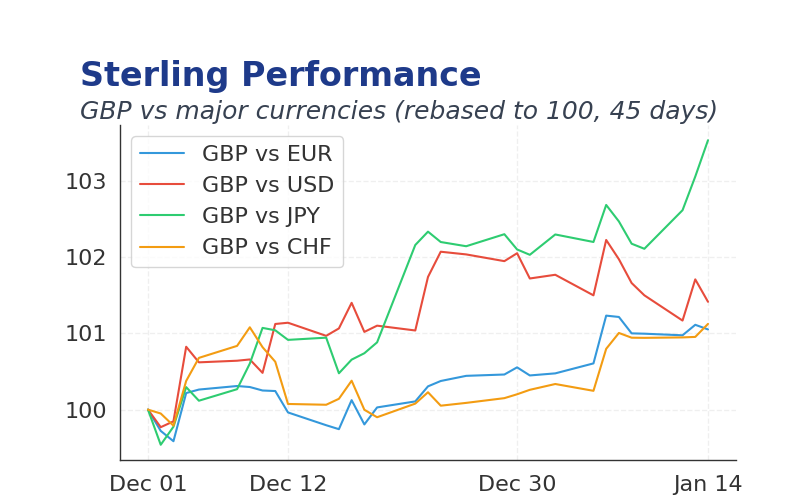

| GBP/USD | 1.340 | +0.01% |

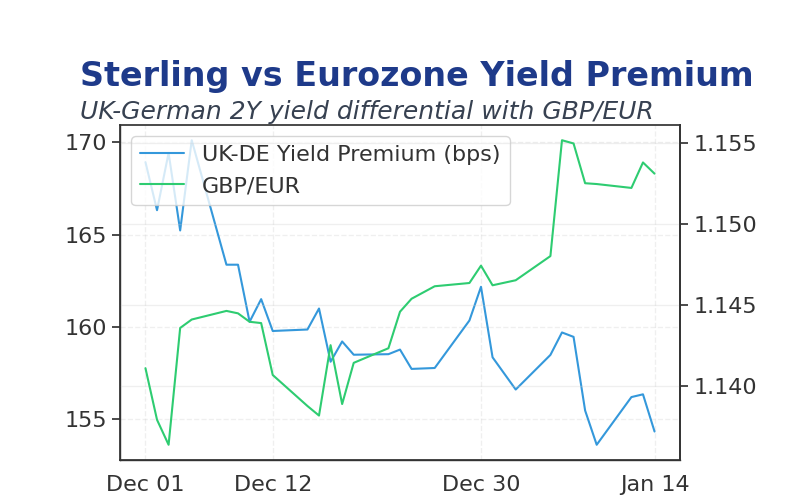

| GBP/EUR | 1.14 | +0.06% |

| GBP/JPY | 208.69 | +0.14% |

| Brent Oil | 62.21 | +0.44% |

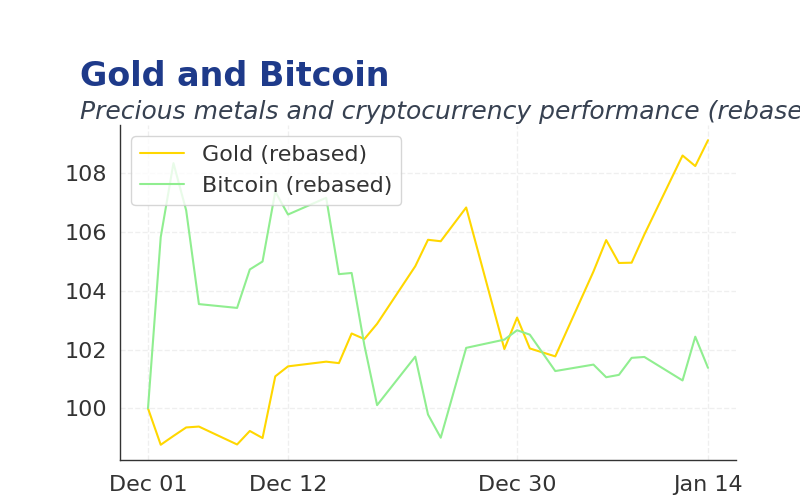

| Gold ($) | 4,196.40 | -0.24% |

| Bitcoin ($) | 92,602.21 | +0.07% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RICS House Pr Bal | -19 | -21 | -16 |

| BOE Kroszner Speech | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP m/m | -0.10 | 0.10 | 07:00 |

| GDP 3-Month Avg | 0.10 | 0 | 07:00 |

| Goods Trade Bal | -18.9m | -19.3m | 07:00 |

| Goods Trade Bal Non-EU | -6.8m | - | 07:00 |

| Ind Prod m/m | -2 | 0.70 | 07:00 |

| Mfg Production m/m | -1.70 | 1 | 07:00 |

- RICS House Price Balance improved to -16 from -19, beating consensus of -21, signaling resilience in UK property market amid easing inflation pressures.

- US markets hit records as Dow and S&P 500 rally on Fed cuts, while Nasdaq dips due to AI spending concerns, boosting global risk appetite.

- BoE's cutting cycle remains dovish, with markets pricing steady pace despite geopolitical risks.

Yesterday's Recap

The RICS House Price Balance came in at -16, better than the consensus of -21 and previous -19, reflecting improving sentiment in the UK housing market.

BoE Deputy Governor Kroszner delivered a speech, though details were limited, focusing on financial stability without shifting rate cut expectations.

Markets traded calmly, with FTSE 100 rising 0.49% to 9703.16 amid subdued volatility.

Gilt yields were stable, 2-year at 3.78% (+0bps) and 10-year at 4.49% (-1bps), while Sterling edged higher, GBP/USD up 0.01% to 1.340 and GBP/EUR up 0.06% to 1.14.

Commodities held steady, Brent oil climbing 0.44% to 62.21, gold falling 0.24% to 4196.40, and bitcoin up 0.07% to 92602.21.

The Day Ahead

UK GDP month-on-month is expected at 0.1%, up from previous -0.1%, potentially signaling economic stabilization ahead of BoE decisions.

The 3-month GDP average at 0.0% versus prior 0.1% will gauge quarterly growth trends.

Goods trade balance is forecast at -193B versus -188.8B previous, while industrial production may rise 0.7% from -2.0%.

Manufacturing production is seen at 1.0% versus prior -1.7%, influencing inflation and rate outlook.

Other Economic Notes

UK house prices continue to stabilize, with Nationwide data showing YoY gains moderating amid lower mortgage rates.

Labor market dynamics remain tight, with unemployment edging down as wage pressures ease slowly. (cont...)