UK Macro Daily(Beta Mode)

BoE Rate Cut Amid Inflation Pressures

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,774.76 | +0.79% |

| FTSE 100 | 9,897.42 | +0.61% |

| UK Natural Gas | 3.91 | -2.88% |

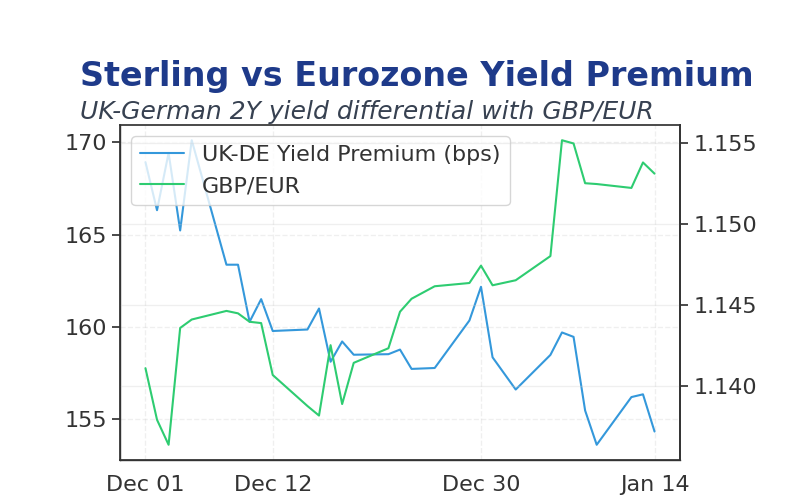

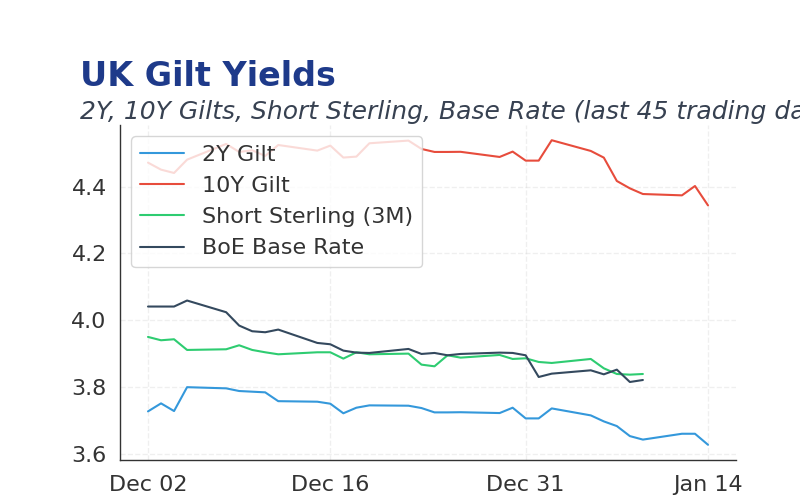

| 2 Year Gilt | 3.75 | +0 bps |

| 10 Year Gilt | 4.53 | +3 bps |

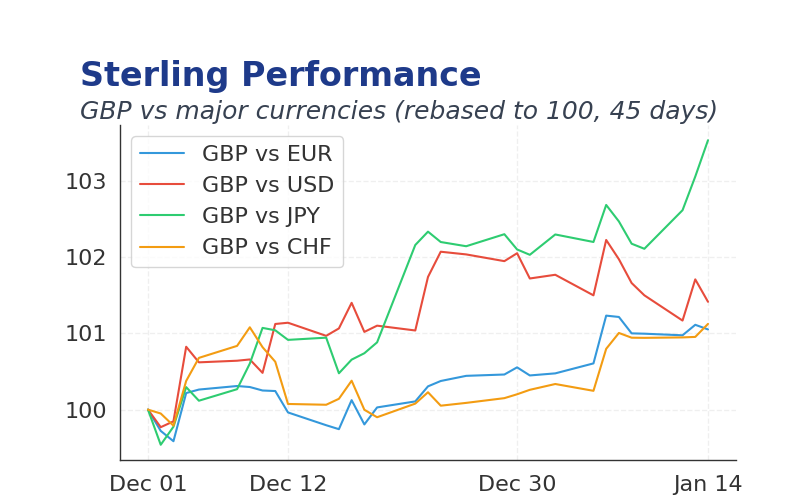

| GBP/USD | 1.337 | -0.03% |

| GBP/EUR | 1.14 | +0.07% |

| GBP/JPY | 210.90 | +1.31% |

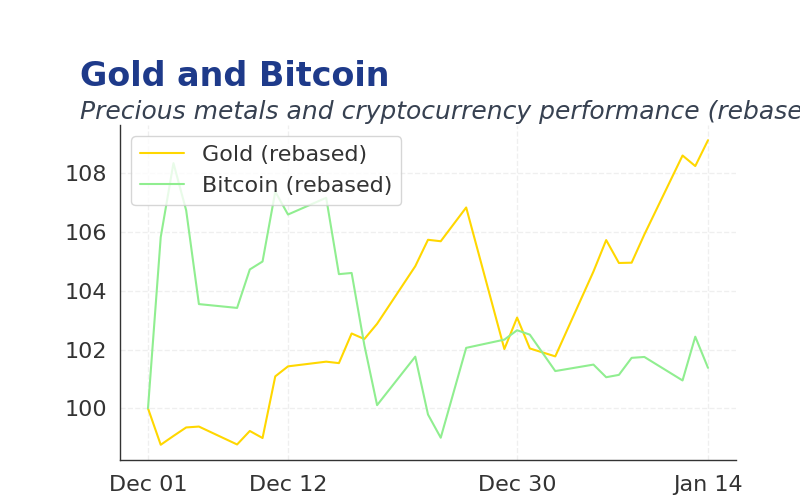

| Brent Oil | 59.82 | +0.23% |

| Gold ($) | 4,339.50 | -0.18% |

| Bitcoin ($) | 88,158.80 | +0.07% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Bal | -28.9m | -21.3m | 07:00 |

- Bank of England reduced interest rates by 25bps to 3.75%, signaling a cautious easing cycle.

- UK CPI data showed inflation cooling, supporting further potential cuts.

- Global oil prices stabilized, aiding UK energy costs.

Friday's Recap

The Bank of England cut its base rate by 25bps to 3.75% in a 5-4 vote, reflecting ongoing inflation pressures and a neutral stance with dovish leanings.

UK CPI rose 0.3% MoM and 2.8% YoY, beating expectations but indicating cooling trends.

Gilt yields rose 3bps on the 10-year and held steady on the 2-year, while sterling edged down 0.03% against the dollar.

The Day Ahead

The UK will release current account balance data at 07:00, with previous figures at -£28.9B and consensus at -£21.3B, potentially influencing sterling.

No major BoE speeches scheduled, but markets will watch for further rate cut signals.

Other Economic Notes

UK services PMI remains resilient amid Brexit challenges, supporting growth.

Housing market activity slowed, with Nationwide prices up 3.2% YoY.

Energy costs from Brexit and geopolitical tensions weigh on consumer spending.