UK Macro Daily(Beta Mode)

Calm Markets, Global Shifts

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,929.94 | 0.00% |

| FTSE 100 | 9,866.53 | -0.04% |

| UK Natural Gas | 4.37 | 0.00% |

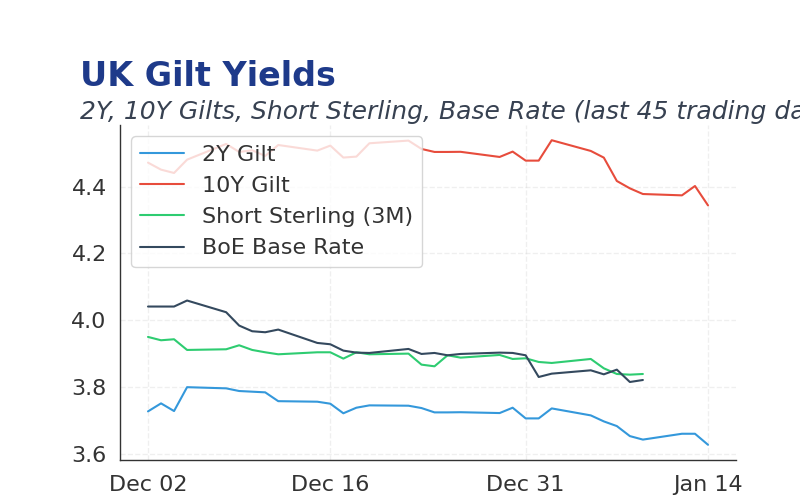

| 2 Year Gilt | 3.72 | +0 bps |

| 10 Year Gilt | 4.49 | -1 bps |

| GBP/USD | 1.352 | +0.09% |

| GBP/EUR | 1.15 | +0.04% |

| GBP/JPY | 210.87 | +0.05% |

| Brent Oil | 60.64 | 0.00% |

| Gold ($) | 4,529.10 | 0.00% |

| Bitcoin ($) | 87,254.86 | +0.16% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- FTSE 100 edged down 0.04% to 9866.53 amid thin holiday volumes and subdued UK economic activity.

- No major UK data releases today, with focus on year-end positioning and potential geopolitical updates.

- BoE maintains cautious easing stance as inflation data supports gradual cuts, amid global energy transitions.

Yesterday's Recap

UK markets traded calmly with limited economic data, as FTSE 100 dipped 0.04% to 9866.53, reflecting profit-taking in energy stocks.

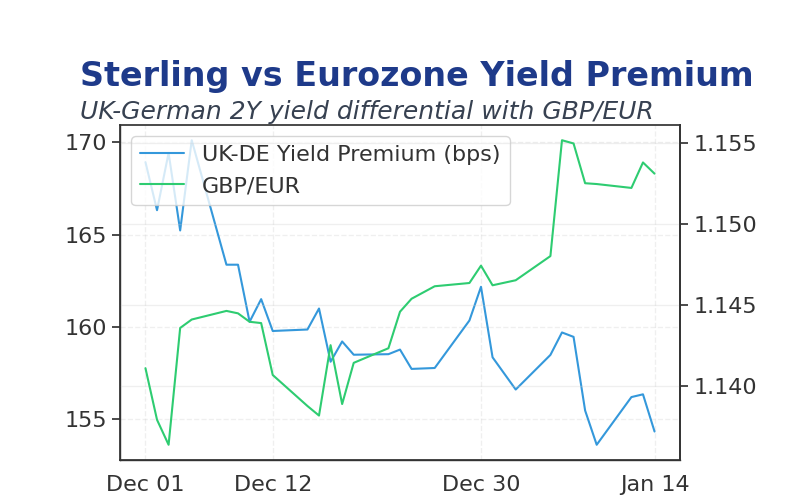

Gilt yields showed minor shifts, with 2-year holding at 3.72% and 10-year easing 1bps to 4.49%, signaling steady bond demand.

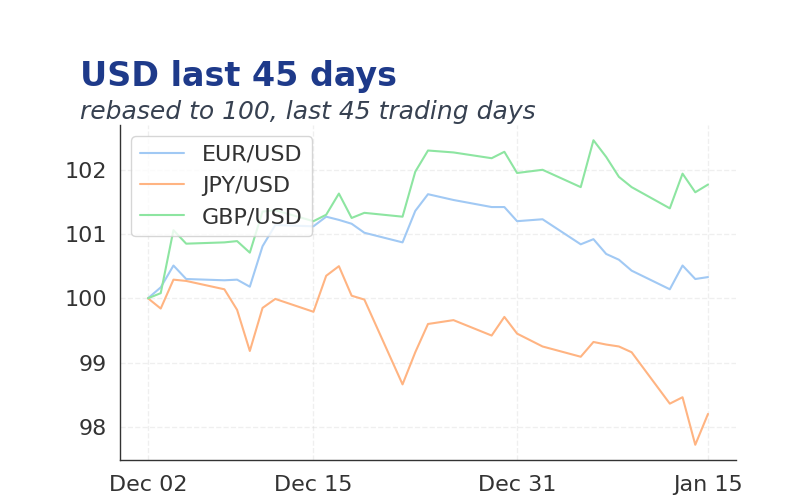

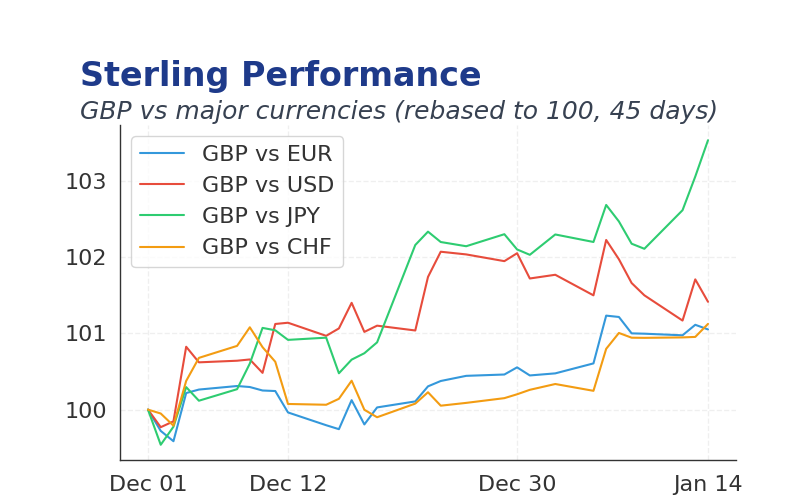

Sterling was stable, with GBP/USD up 0.09% to 1.352 and GBP/EUR rising 0.04% to 1.15, amid balanced FX flows.

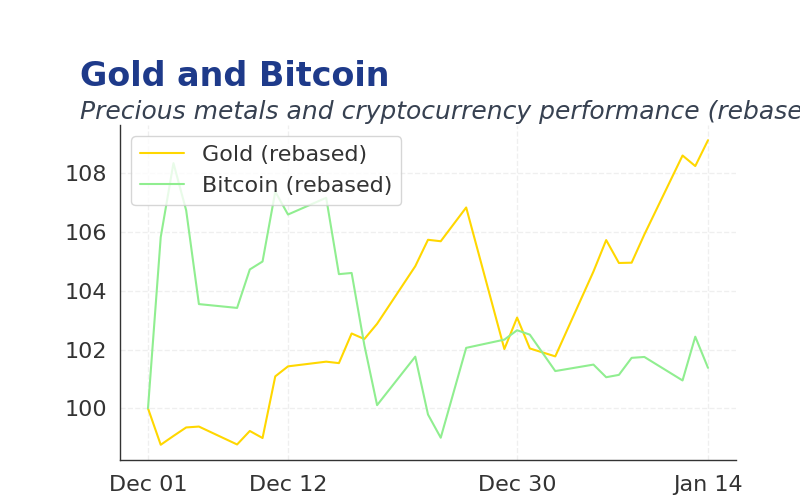

Commodities remained flat, Brent oil at 60.64 and natural gas at 4.37, while gold held at 4529.10.

No BoE speeches occurred, leaving policy outlook unchanged.

The Day Ahead

With no major UK economic releases scheduled for today, markets may focus on thin volumes and potential weekend geopolitical developments.

Investors will monitor for any updates on US-Venezuela tensions that could ripple into oil prices.

Early January signals on global growth and Fed policy may influence positioning ahead of year-end.

Other Economic Notes

Rising numbers of young Britons emigrating for better opportunities abroad highlight labor market pressures and cost-of-living challenges.

Brexit impacts continue to weigh on UK trade dynamics, potentially slowing services growth.

Housing market stability supports consumer confidence, though energy costs remain a drag.