UK Macro Daily(Beta Mode)

Year-End Calm Persists

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,905.74 | -0.35% |

| FTSE 100 | 9,940.71 | +0.75% |

| UK Natural Gas | 4.69 | +7.35% |

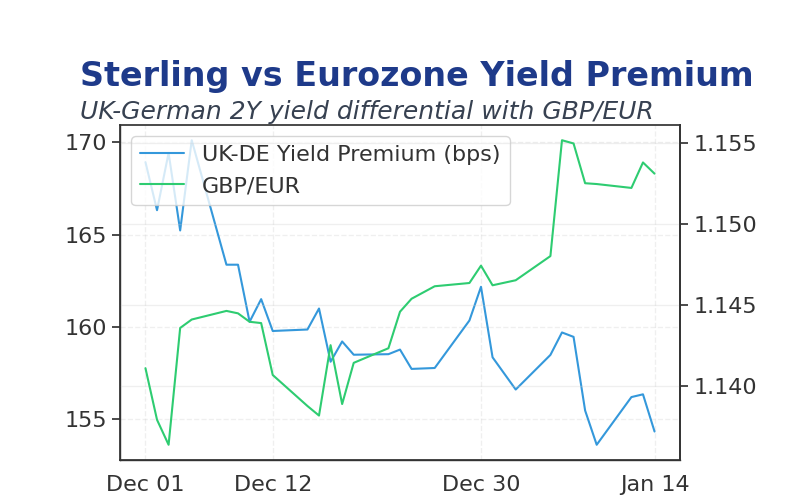

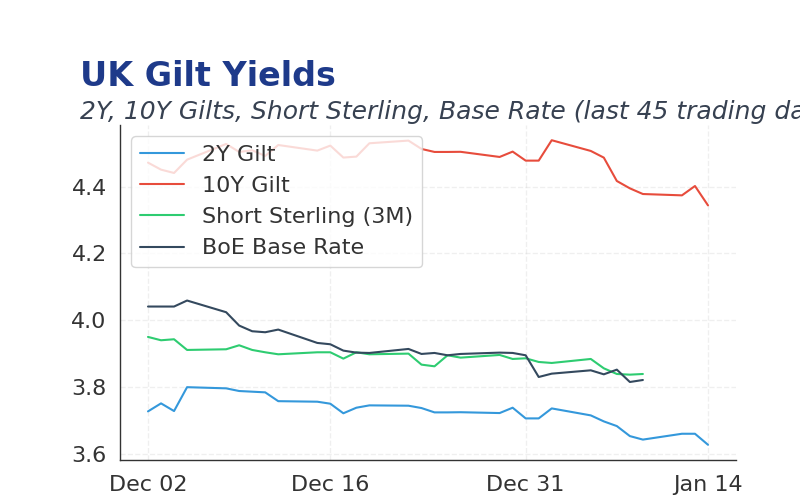

| 2 Year Gilt | 3.74 | +1 bps |

| 10 Year Gilt | 4.50 | +1 bps |

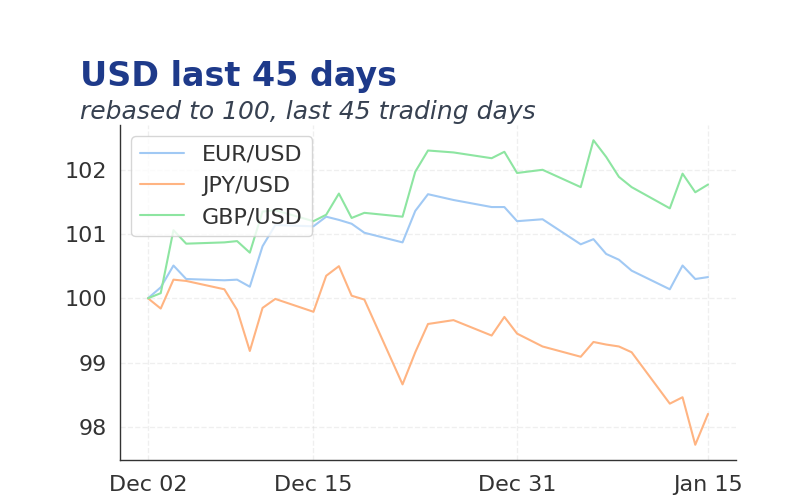

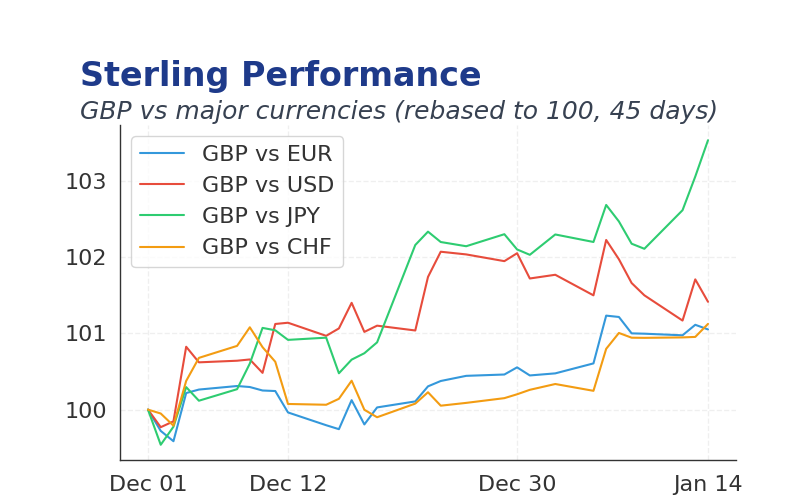

| GBP/USD | 1.346 | -0.06% |

| GBP/EUR | 1.15 | +0.01% |

| GBP/JPY | 210.74 | +0.04% |

| Brent Oil | 61.94 | +2.14% |

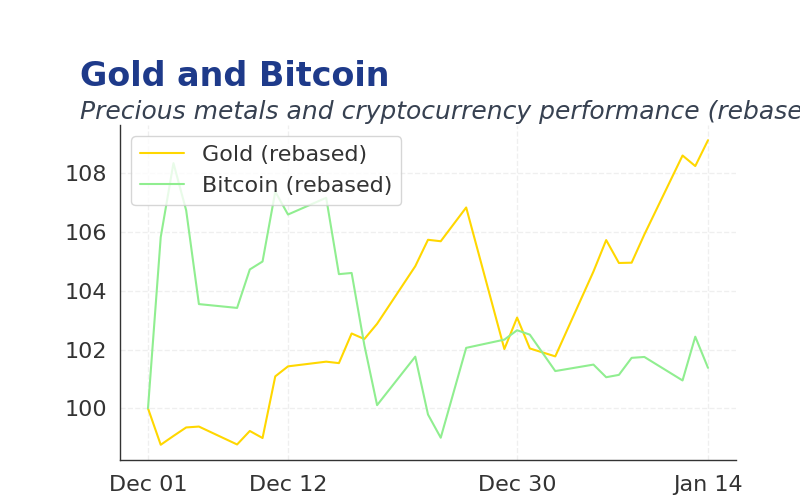

| Gold ($) | 4,325.10 | -4.50% |

| Bitcoin ($) | 88,424.00 | +0.03% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK markets closed mixed but calm, with FTSE 100 edging up amid thin holiday volumes and stable gilt yields.

- Global trade tensions from Trump's tariffs continued to weigh on commodities, though oil prices ticked higher.

- BoE outlook leans toward cautious rate cuts, supported by moderating inflation trends.

Yesterday's Recap

UK markets traded calmly on Tuesday, with the FTSE 100 closing up 0.75% to 9,940.71 amid year-end positioning and thin volumes.

Gilt yields edged higher by 1bps, with 2-year at 3.74% and 10-year at 4.50%, reflecting steady investor caution ahead of holidays.

Sterling was largely flat, with GBP/USD at 1.346 and GBP/EUR at 1.15, as geopolitical headlines failed to spark significant moves.

In commodities, Brent oil rose 2.14% to $61.94, driven by supply concerns from Middle East tensions, while natural gas surged 7.35% to 4.69 amid cold weather forecasts.

Gold fell 4.5% to $4,325.10 after margin hikes by CME tempered safe-haven demand, and Bitcoin held steady at $88,424.

No major UK economic data or BoE speeches were released, leaving markets focused on global year-end closures.

The Day Ahead

With UK markets closed for New Year's Day, trading attention shifts to potential weekend geopolitical developments, particularly US-Venezuela relations that could influence oil prices.

Investors will monitor any overnight news from Asia, where mixed equity performance may set the tone for global risk sentiment.

No UK data is scheduled, but eyes will be on early January signals from ECB and Fed policies impacting sterling.

Other Economic Notes

UK services PMI data from last week showed resilience at 51.2, beating expectations and supporting growth momentum despite tariff pressures. (cont...)