UK Macro Daily(Beta Mode)

UK Housing Surges in Calm Trade

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,896.24 | -0.14% |

| FTSE 100 | 9,931.38 | -0.09% |

| UK Natural Gas | 3.97 | -15.25% |

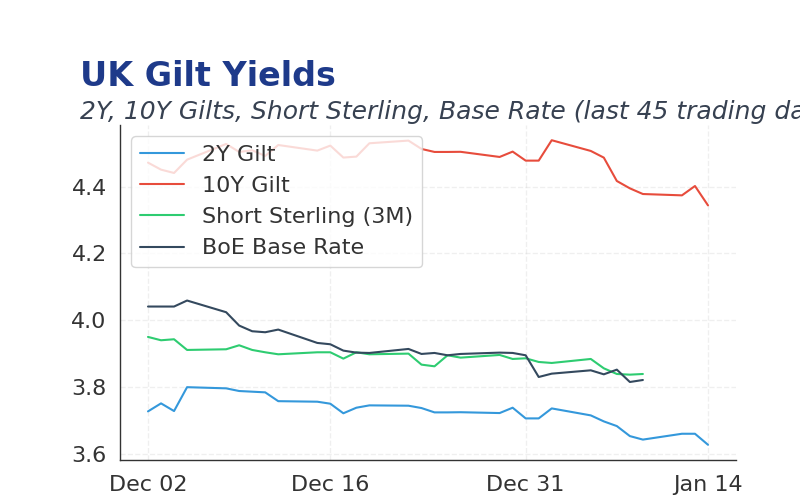

| 2 Year Gilt | 3.71 | -3 bps |

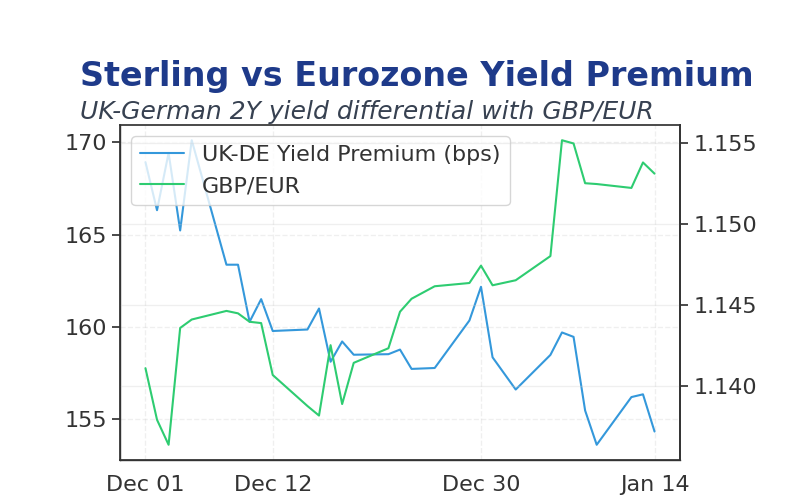

| 10 Year Gilt | 4.48 | -2 bps |

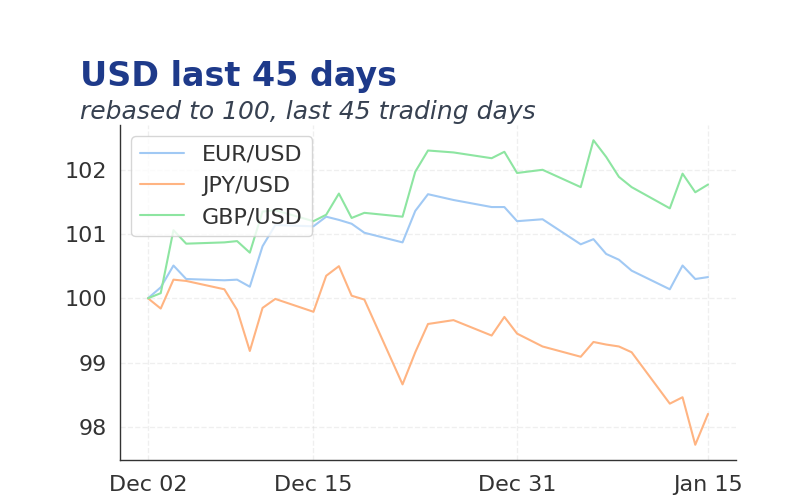

| GBP/USD | 1.347 | -0.10% |

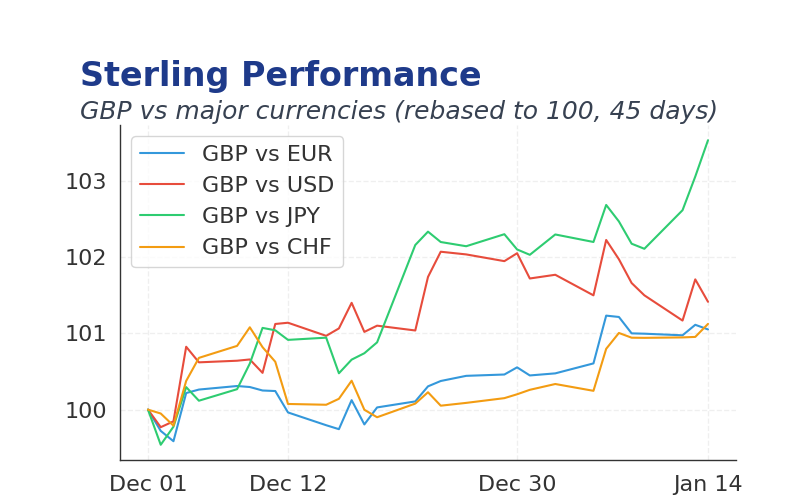

| GBP/EUR | 1.15 | -0.03% |

| GBP/JPY | 211.11 | -0.02% |

| Brent Oil | 61.92 | -0.03% |

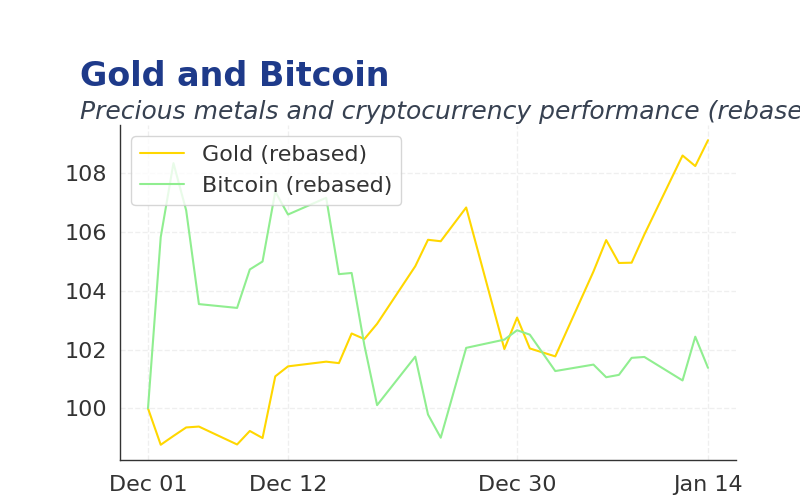

| Gold ($) | 4,370.10 | +1.04% |

| Bitcoin ($) | Data Unavailable | Data Unavailable |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Nationwide Housing Prices m/m | 0.30 | 0.10 | 07:00 |

| Nationwide Housing Prices y/y | 1.80 | 1.20 | 07:00 |

- Nationwide housing prices rose 0.3% m/m and 1.8% y/y, beating consensus expectations and signaling continued residential market resilience despite affordability pressures.

- UK business optimism remains high, with entrepreneurs ranking first globally for positive outlook, driven by professional services and tech sectors.

- Global trade tensions from US tariffs and fishing quota disputes are weighing on export-dependent economies, potentially impacting UK sterling and commodities.

Yesterday's Recap

Nationwide housing prices beat consensus, rising 0.3% month-on-month against expectations of 0.1% and 1.8% year-on-year versus 1.2%, reflecting steady demand in the UK residential sector.

Markets traded calmly with FTSE 100 down 0.09% to 9931.38, Gilt yields stable at 4.48% for 10-year and 3.71% for 2-year, and GBP/USD off 0.10% to 1.347 amid thin year-end volumes.

Commodities showed minimal moves, with Brent oil down 0.03% to 61.92 and gold up 1.04% to 4370.10 on safe-haven flows, while natural gas fell 15.25% to 3.97 due to seasonal factors.

No BoE speeches occurred, but economic data supported neutral policy stance.

The Day Ahead

No major UK economic data releases scheduled today, with markets focusing on thin liquidity and holiday impacts.

Investors will monitor any weekend news flow, including global trade developments, for potential spillover effects on sterling and equities.

Pending European data like Eurozone PMI could influence broader sentiment if released early.

Other Economic Notes

UK services PMI remains elevated, indicating robust economic activity despite global headwinds.

Brexit-related trade frictions continue to challenge export growth in manufacturing sectors.

Energy costs are stabilizing, supporting household spending but with lingering inflationary pressures.