UK Macro Daily(Beta Mode)

Data Beats Lift Sterling

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,858.47 | 0.00% |

| FTSE 100 | 10,004.57 | +0.54% |

| UK Natural Gas | 3.62 | 0.00% |

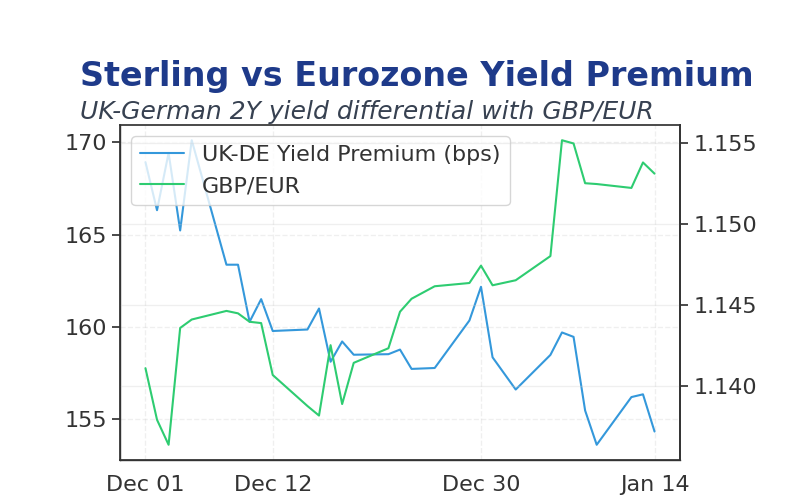

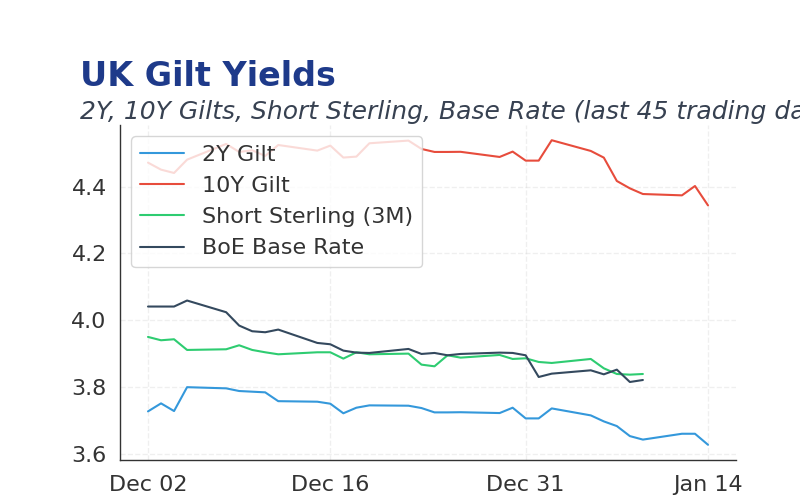

| 2 Year Gilt | 3.72 | -2 bps |

| 10 Year Gilt | 4.51 | -3 bps |

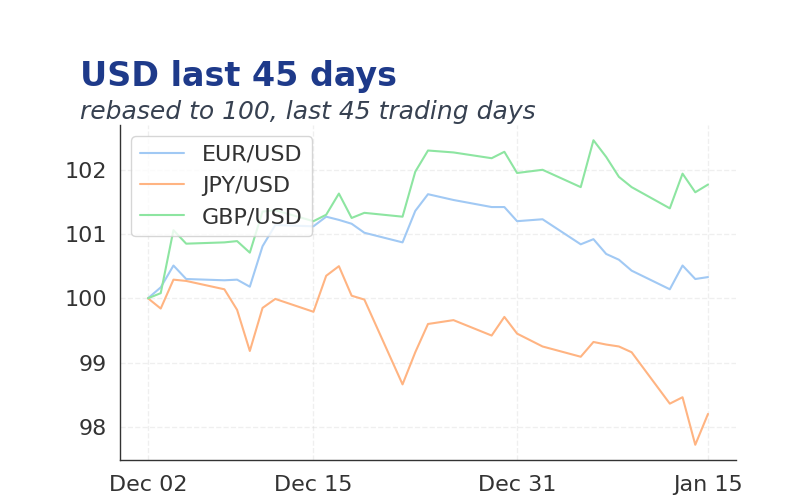

| GBP/USD | 1.355 | +0.05% |

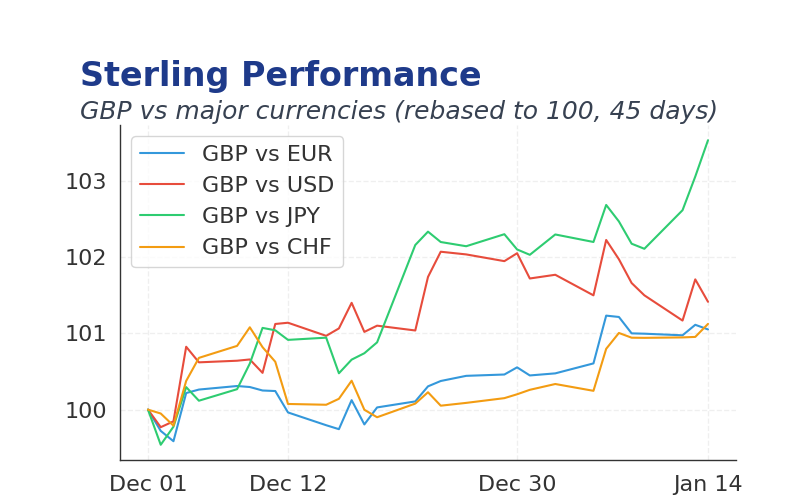

| GBP/EUR | 1.16 | -0.01% |

| GBP/JPY | 211.97 | +0.11% |

| Brent Oil | 60.75 | 0.00% |

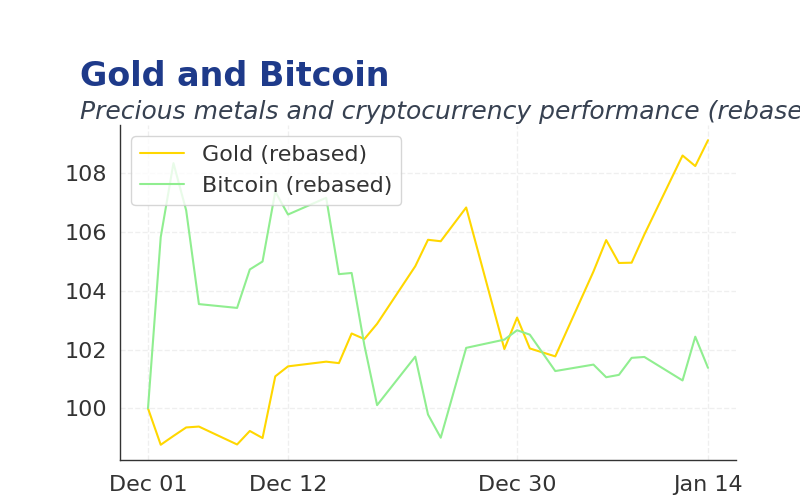

| Gold ($) | 4,314.40 | 0.00% |

| Bitcoin ($) | 93,717.82 | -0.16% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Consumer Credit | 1.7m | 1.1m | 2.1m |

| Mortgage Approvals | 65,010 | 64,400 | 64,530 |

| Mortgage Lending Level | 4.2m | 4.5m | 4.5m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Constr PMI | 39.40 | 42.50 | 09:30 |

- UK mortgage lending and approvals data exceeded expectations, signaling housing market stability and supporting BoE easing outlook.

- Venezuela raid by US forces raised oil prices, boosting energy stocks but calming broader market volatility.

- Global energy scarcity concerns persist, potentially pressuring UK inflation and policy decisions.

Yesterday's Recap

BoE consumer credit surged to £2.077B, significantly above consensus of £1.1B and prior £1.713B, reflecting robust borrowing activity amid easing credit conditions.

Mortgage approvals rose to 64,530, edging past expectations of 64,400 and previous 65,010, while mortgage lending climbed to £44.9B versus consensus £45B.

Markets remained calm with FTSE 100 up 0.54% to 10,004.57, Gilts stable with 2-year at 3.72% down 2bps and 10-year at 4.51% down 3bps, and Sterling firming 0.05% to 1.355 against USD.

Commodities were steady with Brent at $60.75 and gold at $4,314.40, while Bitcoin dipped 0.16% to $93,717.82.

The Day Ahead

S&P Global Construction PMI at 09:30 UK time, expected at 42.5 versus prior 39.4, may signal sector recovery or ongoing weakness in UK infrastructure.

No major BoE speeches scheduled, leaving focus on PMI data's implications for growth and rate cut timing.

Investors will monitor for beats that could boost Sterling and equities amid calm market conditions.

Other Economic Notes

Rising energy scarcity risks exacerbate UK inflation pressures, potentially delaying BoE cuts despite housing stability.

Brexit impacts continue to weigh on UK services, with global inequality trends hinting at uneven economic downturns.

Housing market resilience supports consumer spending, countering deflationary threats from resource constraints.