UK Macro Daily(Beta Mode)

UK Recovery Amid Tariffs

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,944.47 | 0.00% |

| FTSE 100 | 10,195.35 | -0.39% |

| UK Natural Gas | 3.13 | 0.00% |

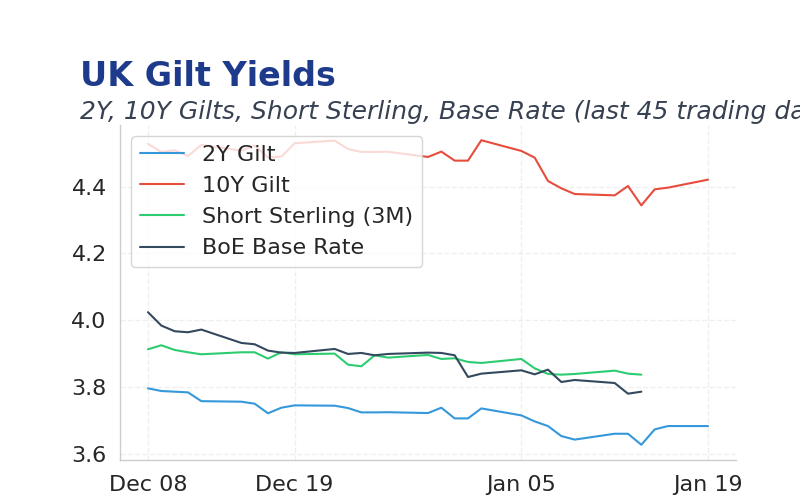

| 2 Year Gilt | 3.68 | +0 bps |

| 10 Year Gilt | 4.42 | +2 bps |

| GBP/USD | 1.344 | +0.10% |

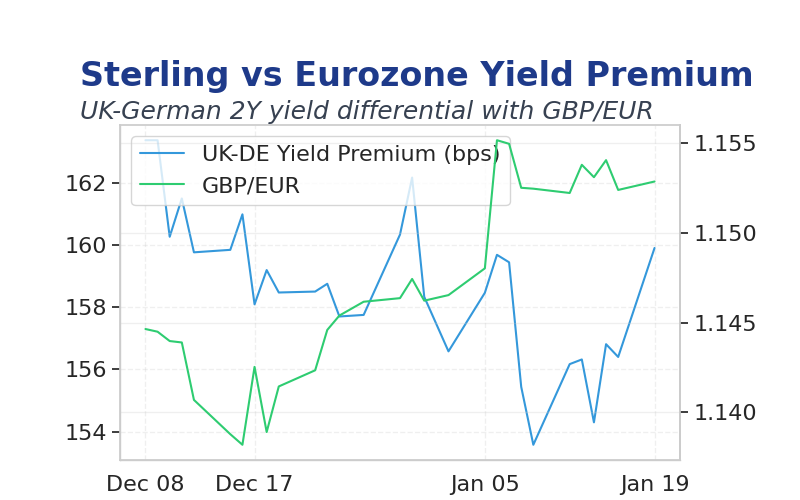

| GBP/EUR | 1.15 | -0.08% |

| GBP/JPY | 212.69 | +0.17% |

| Brent Oil | 63.76 | 0.00% |

| Gold ($) | 4,616.30 | 0.00% |

| Bitcoin ($) | 90,995.28 | -1.69% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemp Rate | 5.10 | 5 | 07:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.70 | 4.60 | 07:00 |

| Employ Change | -16,000 | 27,000 | 07:00 |

| Inflation Rate y/y | 3.20 | 3.30 | 07:00 |

| Core Inflation Rate y/y | 3.20 | 3.20 | 07:00 |

| Inflation Rate m/m | -0.20 | 0.40 | 07:00 |

| CBI Business Optimism Index | -31 | - | 11:00 |

| CBI Industrial Trends Orders | -32 | -33 | 11:00 |

- UK unemployment data at 07:00 expected at 5.0%, with earnings and employment changes signaling labor market resilience.

- Headline and core inflation releases at 07:00 forecasted at 0.4% and 0.3% m/m, watched for BoE policy implications.

- Global tariff threats from US revive trade war fears, pressuring Sterling and UK export outlook.

Yesterday's Recap

Markets traded calmly on Friday, with FTSE 100 closing at 10195.35, a modest 0.39% decline amid light economic activity.

Gilt yields edged higher, with 2-year steady at 3.68% and 10-year up 2bps to 4.42%, reflecting steady bond demand.

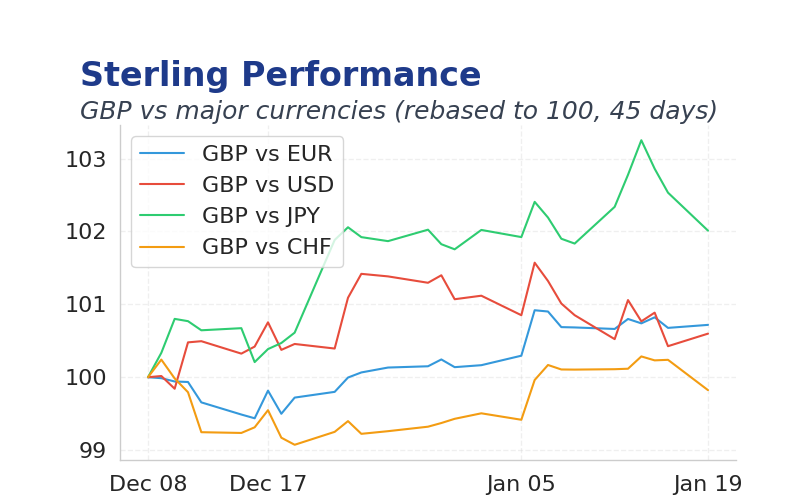

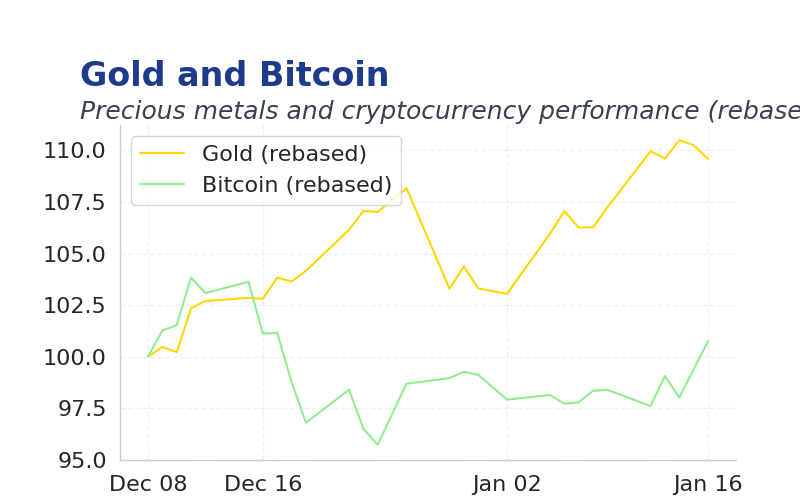

Sterling showed mild gains, with GBP/USD at 1.344 and GBP/EUR at 1.15, while commodities held firm with Brent at 63.76 and gold at 4616.30.

No major BoE speeches, but prior comments underscored data-dependent easing.

The Day Ahead

Unemployment rate and average earnings data at 07:00 are crucial, expected at 5.0% and 4.6% respectively, to gauge labor market strength ahead of MPC decisions.

Inflation figures at 07:00, forecasted at 0.4% headline and 0.3% core, will influence expectations for rate cut timing.

CBI business optimism and industrial trends orders at 11:00 may reveal manufacturing sentiment, with consensus at -31 and -33.

Other Economic Notes

KPMG highlights steady UK economic recovery, with Q4 GDP projected at 0.2% growth driven by manufacturing resurgence and renewable energy investments.

Household spending is picking up on lower inflation, though credit strains persist with rising unsecured borrowing and default risks.

Brexit impacts linger, but offshore wind contracts signal long-term energy stability.