UK Macro Daily(Beta Mode)

Jobs Beat Amid Tariff Fears

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,940.01 | 0.00% |

| FTSE 100 | 10,126.78 | -0.67% |

| UK Natural Gas | 3.10 | 0.00% |

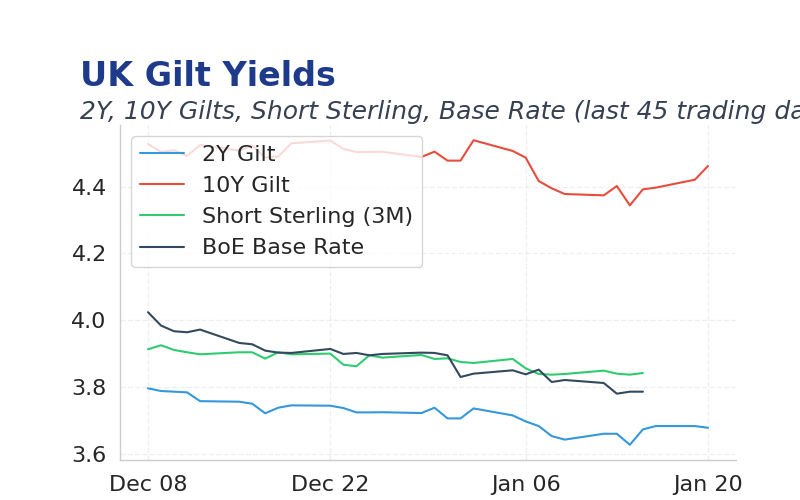

| 2 Year Gilt | 3.68 | +0 bps |

| 10 Year Gilt | 4.46 | +4 bps |

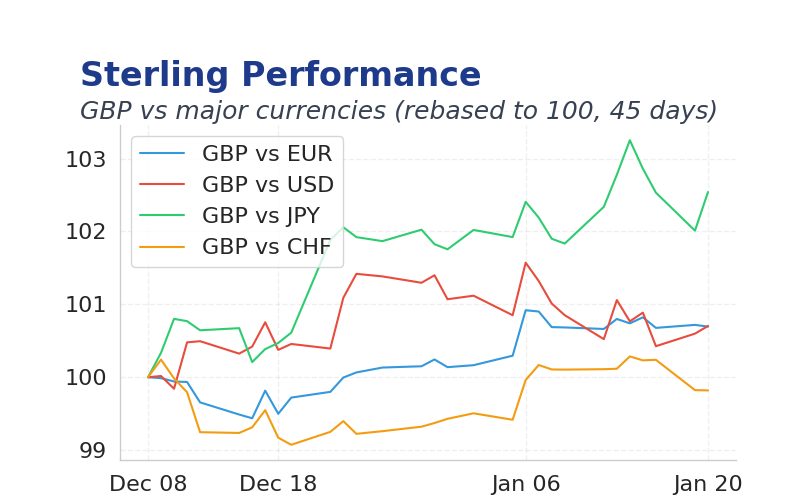

| GBP/USD | 1.344 | +0.03% |

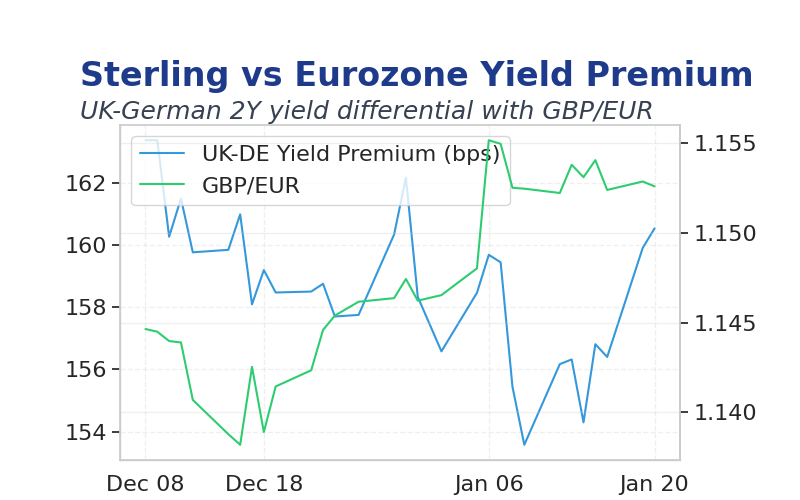

| GBP/EUR | 1.15 | +0.03% |

| GBP/JPY | 212.52 | -0.01% |

| Brent Oil | 64.13 | 0.00% |

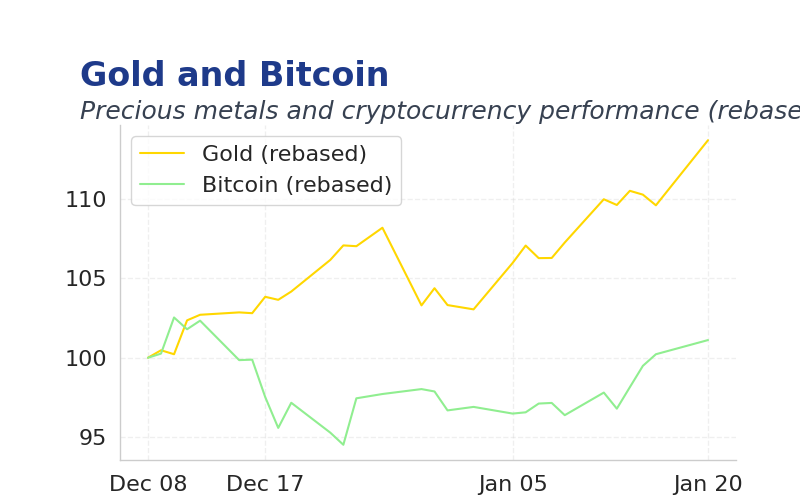

| Gold ($) | 4,588.40 | 0.00% |

| Bitcoin ($) | 89,746.31 | +1.62% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemp Rate | 5.10 | 5 | 5.10 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.80 | 4.60 | 4.70 |

| Employ Change | -16,000 | 27,000 | 82,000 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate y/y | 3.20 | 3.30 | 07:00 |

| Core Inflation Rate y/y | 3.20 | 3.20 | 07:00 |

| Inflation Rate m/m | -0.20 | 0.40 | 07:00 |

| CBI Business Optimism Index | -31 | - | 11:00 |

| CBI Industrial Trends Orders | -32 | -33 | 11:00 |

| BoE Woods Speech | - | - | 14:15 |

| CBI Distributive Trades | -44 | -35 | 11:00 |

- UK employment rose 82,000 in November, beating expectations and signaling labor market resilience despite slowing wage growth.

- Today's inflation data at 07:00 may confirm y/y at 3.3%, guiding BoE rate decisions amid global uncertainties.

- Trump's Greenland tariffs triggered European market declines, pressuring UK equities and highlighting geopolitical risks for Sterling.

Yesterday's Recap

UK unemployment held steady at 5.1% in the three months to November, matching consensus and reflecting persistent labor market slack.

Average earnings growth edged up to 4.7% from previous 4.8%, narrowly beating the 4.6% forecast but signaling moderating wage pressures.

Employment change surged to 82,000, far exceeding the 27,000 consensus, driven by public sector gains offsetting private sector weakness.

Markets traded calmly overall, with FTSE 100 down 0.67% to 10,126.78 amid broader European declines.

Gilts yields rose modestly, with 10-year up 4bps to 4.46%, while GBP/USD ticked up 0.03% to 1.344.

The Day Ahead

UK inflation rate y/y at 07:00 is expected at 3.3%, with m/m at 0.4%, closely watched for signs of persistent price pressures.

Core inflation y/y at 07:00 may hold at 3.2%, influencing BoE outlook on rate cuts.

CBI business optimism at 11:00 is forecast at consensus, while industrial trends orders at 11:00 may show -33, gauging manufacturing sentiment.

BoE's Woods speech at 14:15 could clarify policy stance amid labor data beats.

Other Economic Notes

Private sector wage growth has dropped to a five-year low at 3.6%, dampening consumer spending amid elevated costs.

Unemployment expectations rose to 5.3% by end-year, reflecting weaker hiring and rising staffing expenses.