UK Macro Daily(Beta Mode)

UK Inflation Edges Up on Retail Beat

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,913.35 | +0.55% |

| FTSE 100 | 10,143.44 | -0.07% |

| UK Natural Gas | 5.05 | +3.49% |

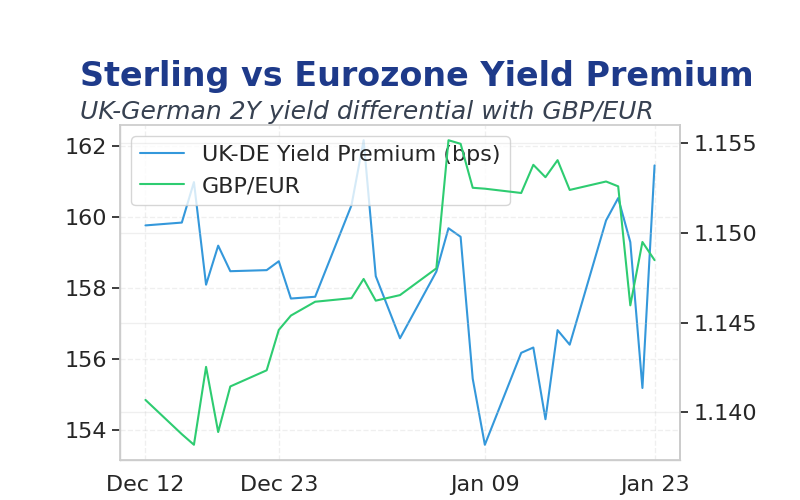

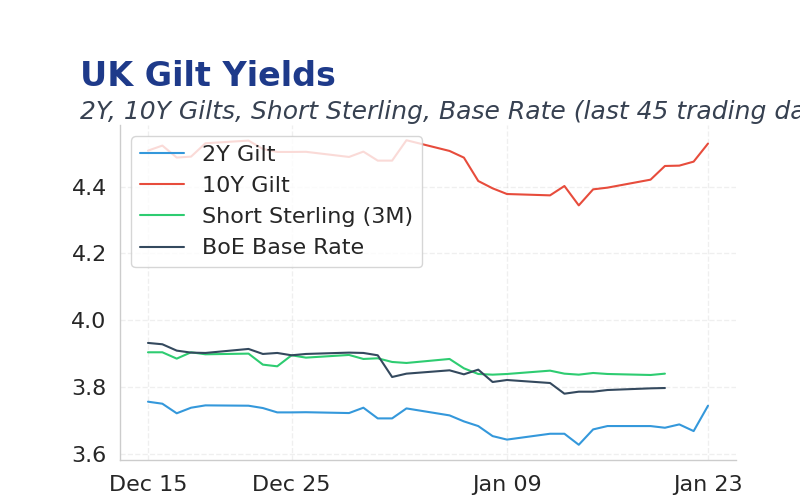

| 2 Year Gilt | 3.74 | +0 bps |

| 10 Year Gilt | 4.53 | +0 bps |

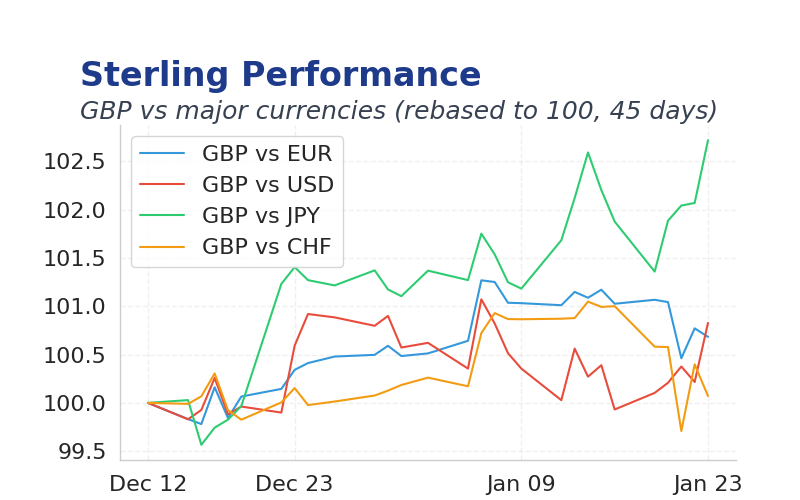

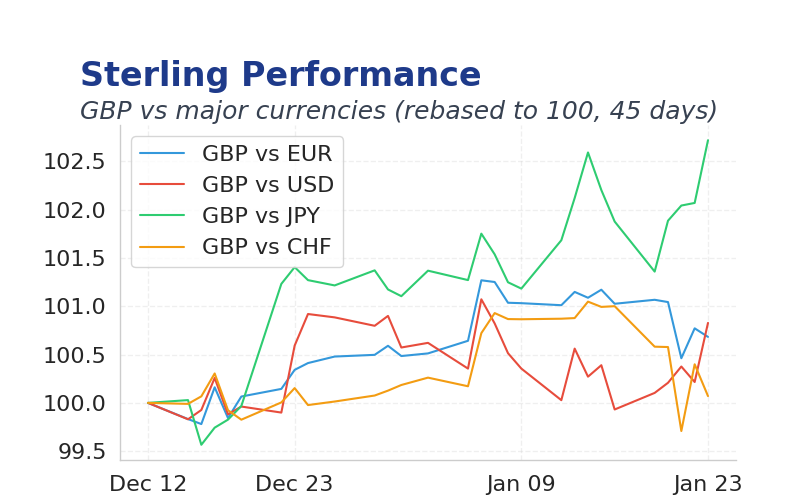

| GBP/USD | 1.367 | +0.20% |

| GBP/EUR | 1.15 | -0.10% |

| GBP/JPY | 210.73 | -0.82% |

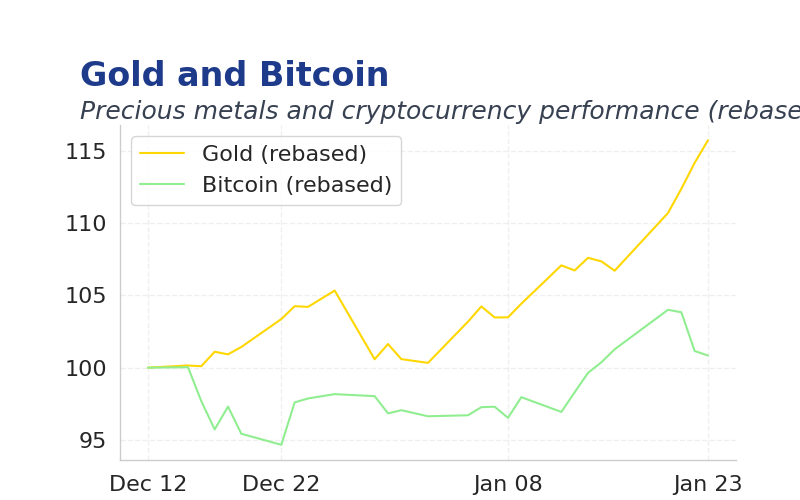

| Brent Oil | 64.06 | -1.81% |

| Gold ($) | 4,908.80 | +1.59% |

| Bitcoin ($) | 87,811.68 | +1.44% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK CPI rose to 3.4% YoY, beating expectations and fueling BoE caution on rate cuts.

- Retail sales surged 0.4% MoM, signaling resilient consumer demand amid moderating inflation.

- Global geopolitical tensions boosted gold prices, pressuring risk assets and Sterling stability.

Friday's Recap

UK CPI ticked up to 3.4% YoY in December, exceeding the 3.2% consensus and marking a first rise in five months, driven by higher housing costs.

Retail sales climbed 0.4% MoM, surpassing expectations for a decline and underscoring robust consumer spending despite tariff fears.

Manufacturing and services PMI data indicated continued expansion, reinforcing economic momentum and supporting Sterling's modest 0.2% gain against the USD.

FTSE 100 edged down 0.07% to 10,143.44, reflecting cautious trading amid mixed global cues, while Gilt yields held steady.

Commodities saw Brent oil dip 1.81% to 64.06, while gold rallied 1.59% to 4,908.80 on safe-haven flows.

The Day Ahead

No major UK economic releases are scheduled for today, allowing focus on weekend news digestion.

Markets will monitor for any BoE commentary, though no speeches are confirmed.

Global events, including US earnings and Fed policy signals, may influence Sterling and UK equities.

Other Economic Notes

UK housing prices remain under pressure from higher borrowing costs, with Nationwide data showing flat YoY growth.

Labour market slack persists, with unemployment at 5.1%, tempering wage inflation risks.

Brexit-related trade frictions continue to weigh on export volumes, offsetting domestic demand strength.