UK Macro Daily(Beta Mode)

Oil Surges on Iran Tensions

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,978.60 | +0.41% |

| FTSE 100 | 10,154.43 | -0.52% |

| UK Natural Gas | 6.95 | +2.26% |

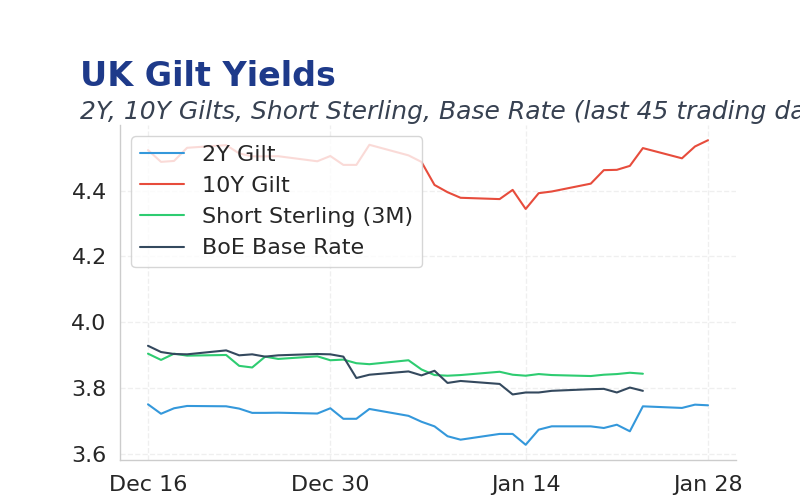

| 2 Year Gilt | 3.75 | +0 bps |

| 10 Year Gilt | 4.55 | +1 bps |

| GBP/USD | 1.384 | +0.28% |

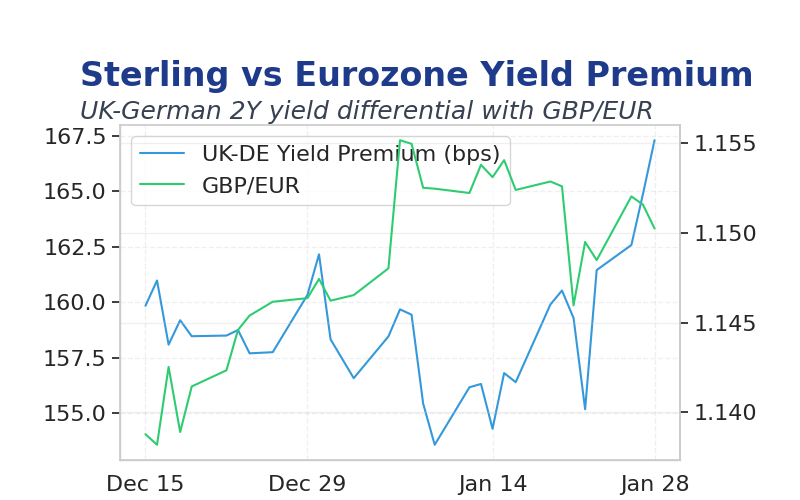

| GBP/EUR | 1.15 | -0.06% |

| GBP/JPY | 211.08 | -0.42% |

| Brent Oil | 67.57 | +3.02% |

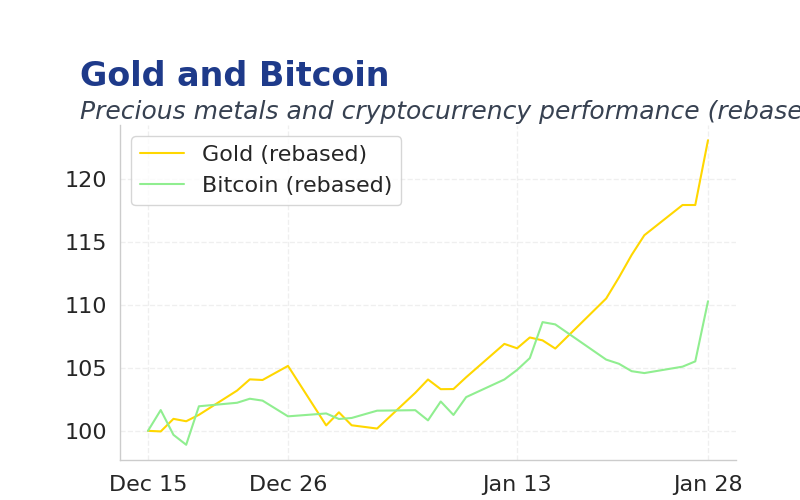

| Gold ($) | 5,079.90 | 0.00% |

| Bitcoin ($) | 88,101.90 | -1.19% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Nationwide Housing Prices m/m | -0.40 | - | 07:00 |

| Nationwide Housing Prices y/y | 0.60 | - | 07:00 |

| BoE Consumer Credit | 2.1m | 1.7m | 09:30 |

| Mortgage Approvals | 64,530 | 64,800 | 09:30 |

| Mortgage Lending Level | 4.5m | 4.5m | 09:30 |

- Brent crude climbed 3% to $67.57 amid escalating US-Iran nuclear standoff, raising global supply concerns.

- UK housing data looms, with Nationwide prices expected to show mixed trends in a slowing market.

- BoE faces mounting pressure for rate cuts as inflation cools, though data dependency remains key.

Yesterday's Recap

FTSE 100 dipped 0.52% to 10154.43, reflecting cautious sentiment ahead of US Fed decisions.

Gilt yields edged up, with 10-year rising 1bps to 4.55%, as investors digested stable inflation readings.

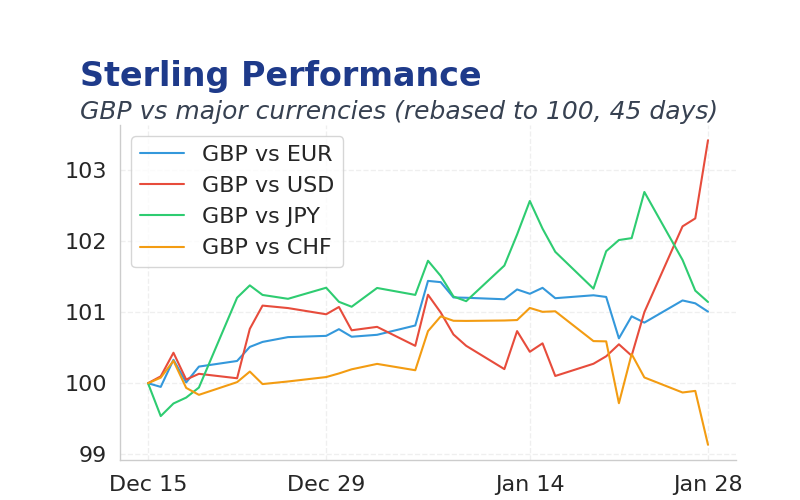

Sterling traded narrowly, gaining 0.28% to 1.384 against USD, while weakening 0.06% versus EUR.

Brent oil surged 3.02% to $67.57, driven by Trump's warnings of potential strikes on Iran.

Natural gas rose 2.26% to 6.95, benefiting from energy sector volatility.

The Day Ahead

Nationwide housing prices release at 07:00, consensus -0.4% m/m, may reveal cooling demand in the property sector.

BoE consumer credit at 09:30, expected at $1.7B versus $2.1B prior, could signal borrowing trends.

Mortgage approvals at 09:30, forecasted at 64,800, will gauge lending activity.

Mortgage lending level at 09:30, projected at $4.5B, may influence broader economic sentiment.

Other Economic Notes

UK Prime Minister Starmer's China visit aims to deepen trade ties amid domestic growth challenges.

India's FTA with the EU advances manufacturing and mobility, potentially boosting global supply chains.

Vietnam expands semiconductor capabilities, enhancing regional tech value chains.