UK Macro Daily(Beta Mode)

Oil Slides on Iran Talks

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,917.81 | -0.84% |

| FTSE 100 | 10,402.34 | +0.85% |

| UK Natural Gas | 3.31 | +2.29% |

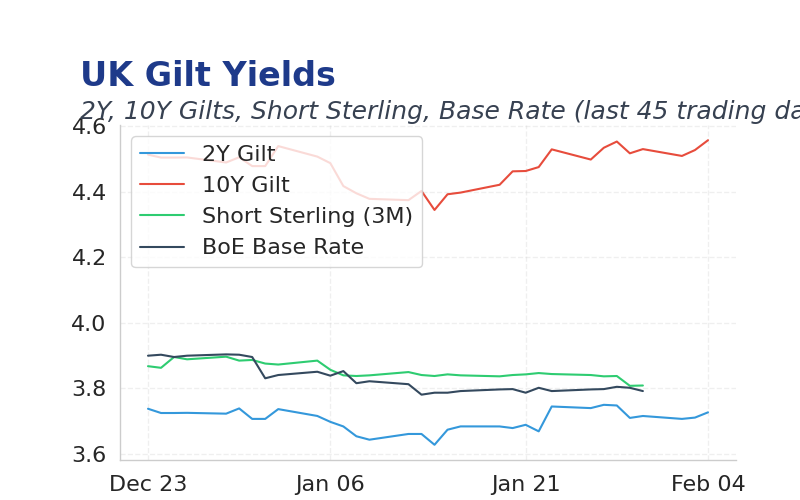

| 2 Year Gilt | 3.73 | +1 bps |

| 10 Year Gilt | 4.56 | +3 bps |

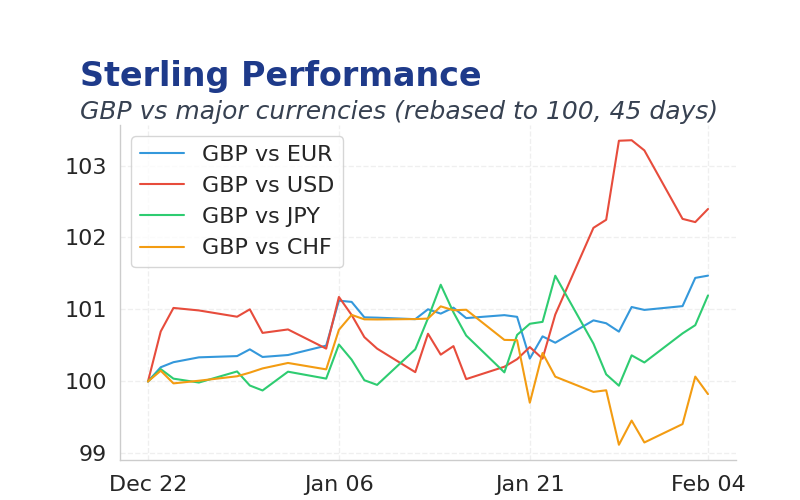

| GBP/USD | 1.362 | -0.22% |

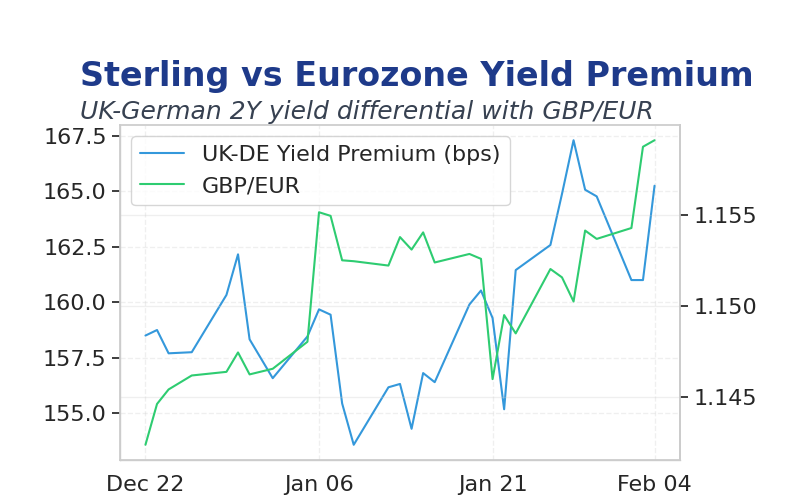

| GBP/EUR | 1.16 | -0.07% |

| GBP/JPY | 213.66 | -0.26% |

| Brent Oil | 67.33 | +1.55% |

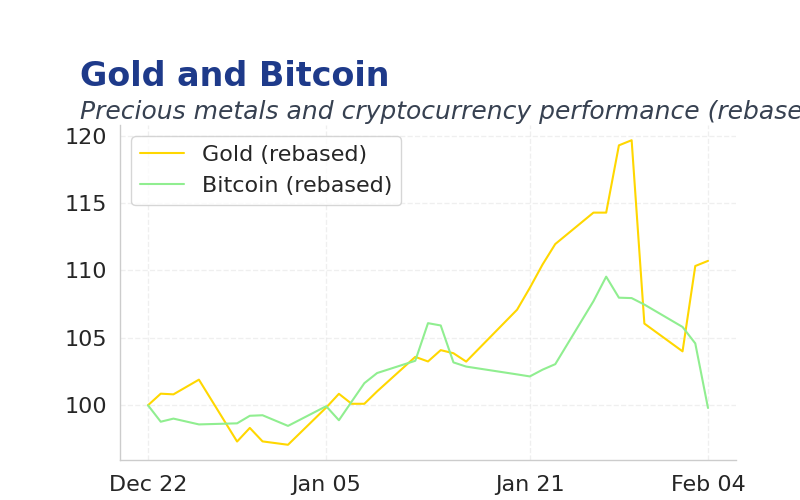

| Gold ($) | 4,903.70 | +6.08% |

| Bitcoin ($) | 70,265.34 | -3.75% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Constr PMI | 40.10 | 42 | 09:30 |

| BoE Rate Decision | 3.75 | 3.75 | 12:00 |

| BoE Policy Report | - | - | 12:00 |

| BoE MPC Vote Cut | 5 | - | 12:00 |

| BoE MPC Vote Hike | 0 | - | 12:00 |

| BoE MPC Vote Unchanged | 4 | - | 12:00 |

| MPC Meeting Minutes | - | - | 12:00 |

| Halifax House Pr Index m/m | -0.60 | 0.20 | 07:00 |

| Halifax House Pr Index y/y | 0.30 | - | 07:00 |

- Brent crude fell 2% to $67.33, pressured by US-Iran diplomatic progress easing Middle East tensions.

- BoE rate decision at noon expected to hold at 3.75%, with MPC split favoring fewer cuts amid inflation vigilance.

- Global AI investments surge, but China's EV sales slump signals demand weakness impacting UK exports.

Yesterday's Recap

UK construction PMI at 40.1 met expectations, highlighting ongoing weakness in the housing sector despite Brexit recovery efforts.

BoE Governor Bailey's comments on data-dependent policy reinforced a cautious easing path, with markets pricing three cuts by year-end.

FTSE 100 rose 0.85% to 10402.34, a steady advance amid global tech rotations.

Gilt yields ticked up 3bps to 4.56% on 10-year notes, reflecting hawkish Fed signals.

GBP/USD dipped 0.22% to 1.362, while Brent oil gained 1.55% to 67.33 on supply concerns.

Gold surged 6.08% to 4903.70, benefiting from risk aversion.

The Day Ahead

S&P Global Construction PMI at 9:30am is expected at 42, providing early insights into UK sector momentum.

BoE Interest Rate Decision and MPC Report at noon likely confirm no change, with voting split at 5 cuts, 0 hikes, 4 holds.

Halifax House Price Index at 7am forecasts 0.2% m/m rise, signaling housing market stabilization.

Other Economic Notes

UK housing prices edged up 0.3% y/y in December, per Halifax, supporting consumer spending but lagging pre-pandemic peaks.

Brexit impacts persist in trade, with EU relations strained by migration and tariffs, limiting export growth.