UK Macro Daily(Beta Mode)

BoE Edges Toward Cuts

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,798.40 | -1.23% |

| FTSE 100 | 10,369.75 | +0.59% |

| UK Natural Gas | 3.51 | +1.27% |

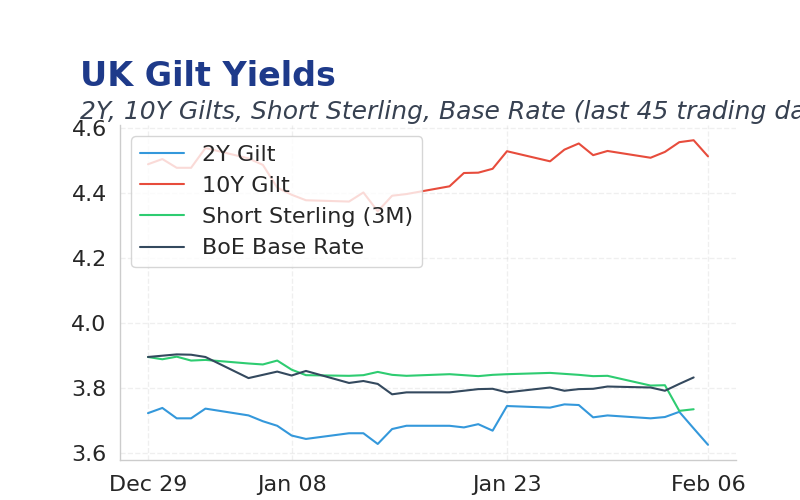

| 2 Year Gilt | 3.62 | +0 bps |

| 10 Year Gilt | 4.51 | +0 bps |

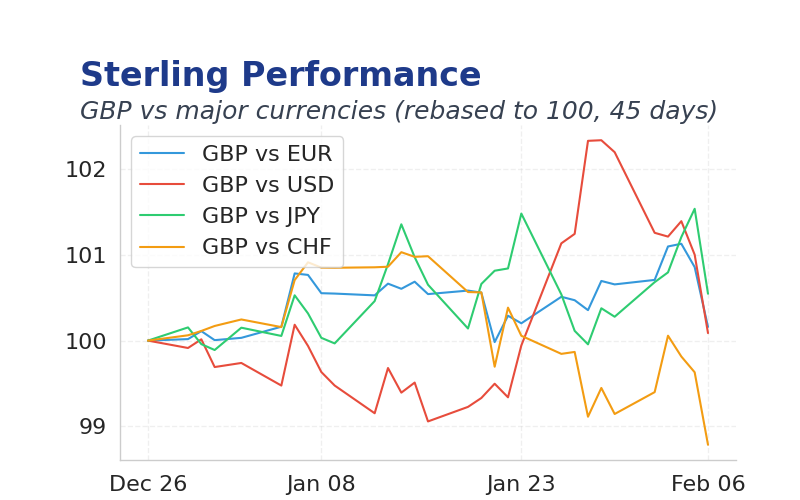

| GBP/USD | 1.361 | -0.07% |

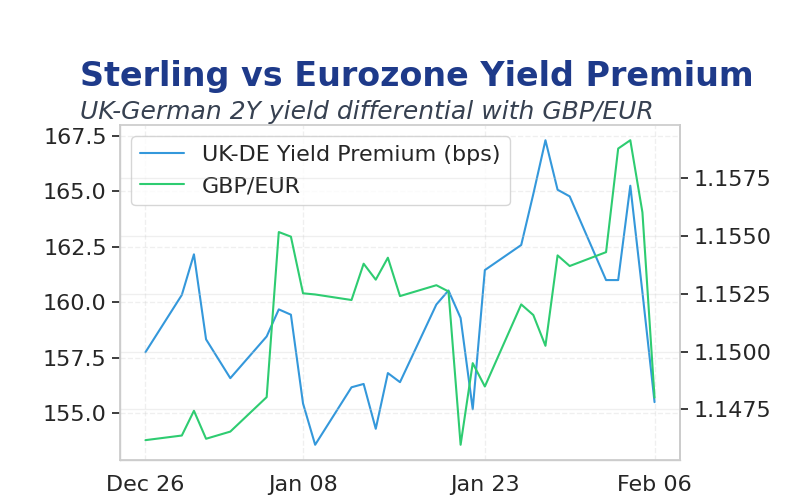

| GBP/EUR | 1.15 | -0.27% |

| GBP/JPY | 212.88 | -0.50% |

| Brent Oil | 67.55 | -2.75% |

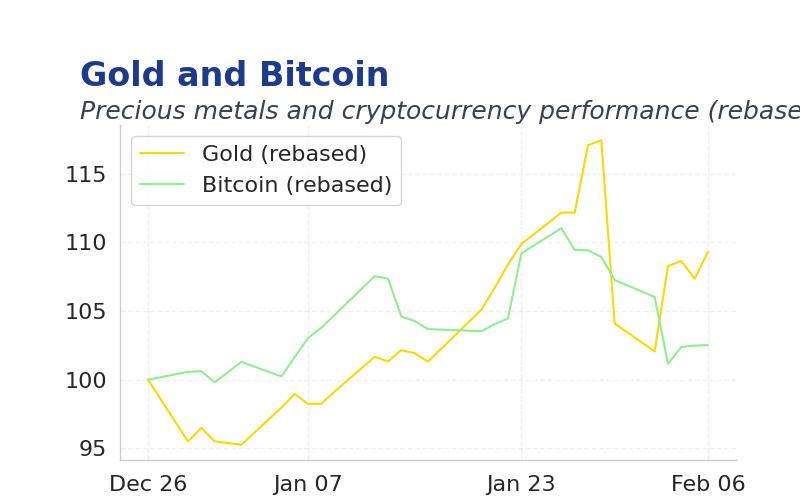

| Gold ($) | 4,861.40 | -1.20% |

| Bitcoin ($) | 70,352.65 | +0.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Gov Bailey Speech | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BRC Retail Sales Monitor y/y | 1 | 1.20 | 00:01 |

- BoE came within a vote of lowering rates, reviving hopes for a near-term cut amid inflation cooling.

- US labor market fragility and US-India trade deal supported risk assets but pressured oil prices.

- Markets pricing fewer BoE cuts in 2025 as data shows economic resilience.

Friday's Recap

BoE Governor Bailey's speech highlighted inflation progress but maintained a cautious tone, coming within a vote of rate cuts as inflation is expected to fall below target soon.

FTSE 100 rose 0.59% to 10369.75, a larger-than-normal gain driven by optimism over US-India trade deals and easing geopolitical risks.

Gilt yields held steady at 3.62% for 2-year and 4.51% for 10-year, reflecting neutral BoE expectations.

Sterling edged down 0.07% to 1.361 against USD, while weakening 0.27% versus EUR as dollar strength from Fed hawkish signals persisted.

Commodities saw mixed moves, with Brent oil falling 2.75% to 67.55 amid US-Iran talks easing supply concerns, natural gas up 1.27% to 3.51 on UK demand, gold down 1.20% to 4861.40 from speculative outflows, and bitcoin flat at 70352.65.

The Day Ahead

BRC Retail Sales Monitor y/y expected at 1.2%, up from previous 1%, will gauge UK consumer spending ahead of key inflation data.

Markets will watch for any BoE commentary on rate timing, with no scheduled speeches but potential media interactions.

Global focus on US jobs data delayed due to shutdown may spillover to UK sentiment if labor weakness persists.

Other Economic Notes

UK manufacturing PMI rose modestly, signaling steady industrial recovery despite global headwinds.

Housing market stability supports consumer confidence, with prices moderating YoY. (cont...)