UK Macro Daily(Beta Mode)

Sterling Steady on Mixed Data

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,941.81 | -0.33% |

| FTSE 100 | 10,472.11 | +1.14% |

| UK Natural Gas | 3.12 | -0.73% |

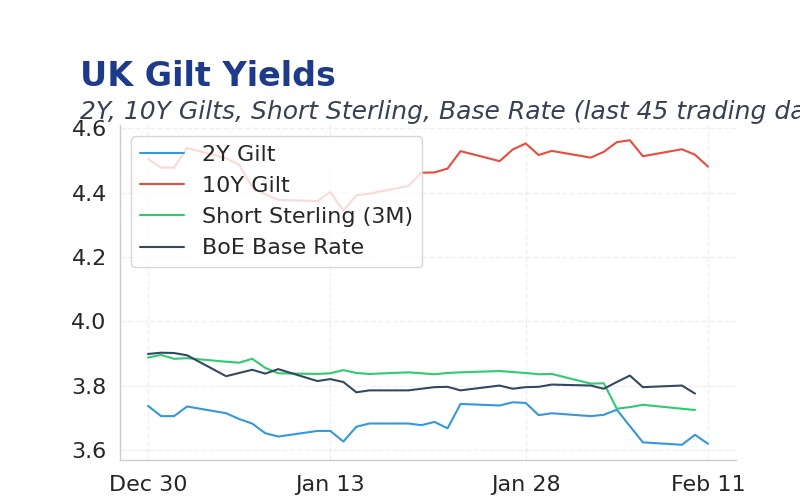

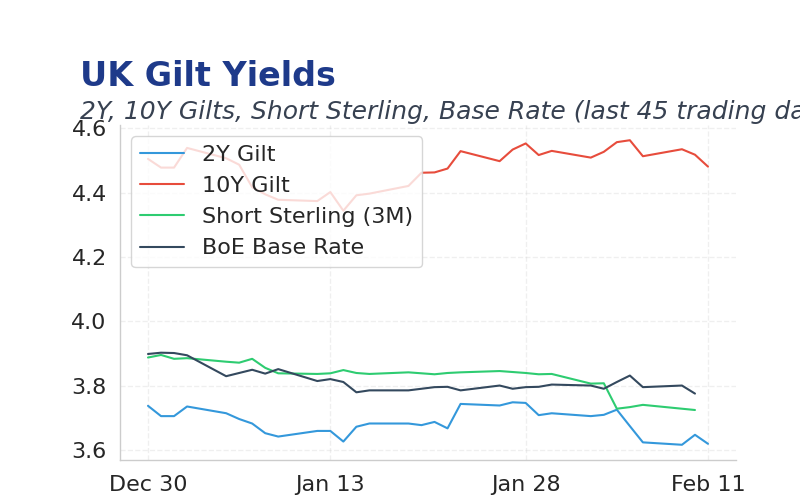

| 2 Year Gilt | 3.62 | -2 bps |

| 10 Year Gilt | 4.48 | -3 bps |

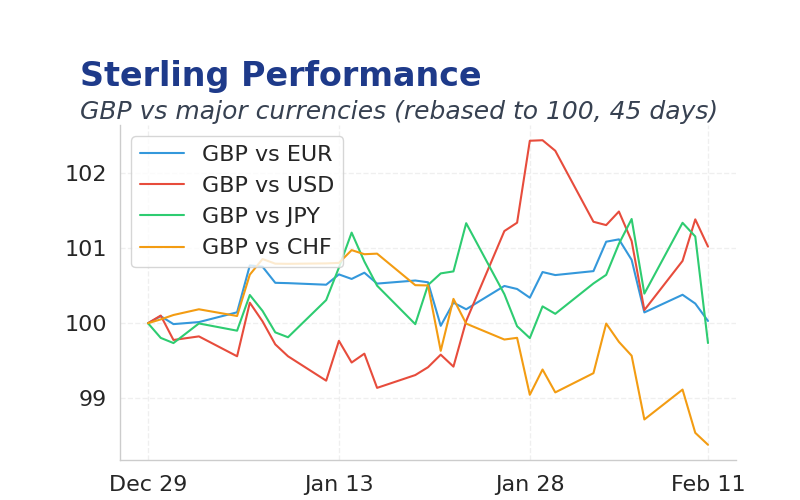

| GBP/USD | 1.363 | +0.08% |

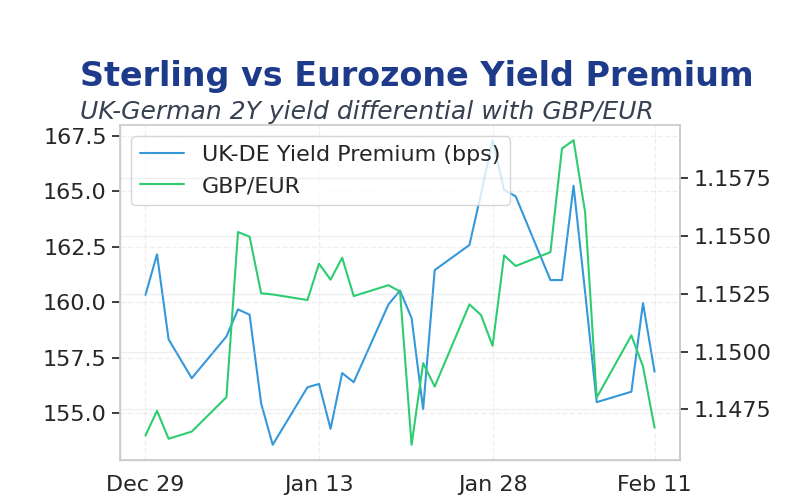

| GBP/EUR | 1.15 | +0.04% |

| GBP/JPY | 208.17 | -0.26% |

| Brent Oil | 68.80 | -0.35% |

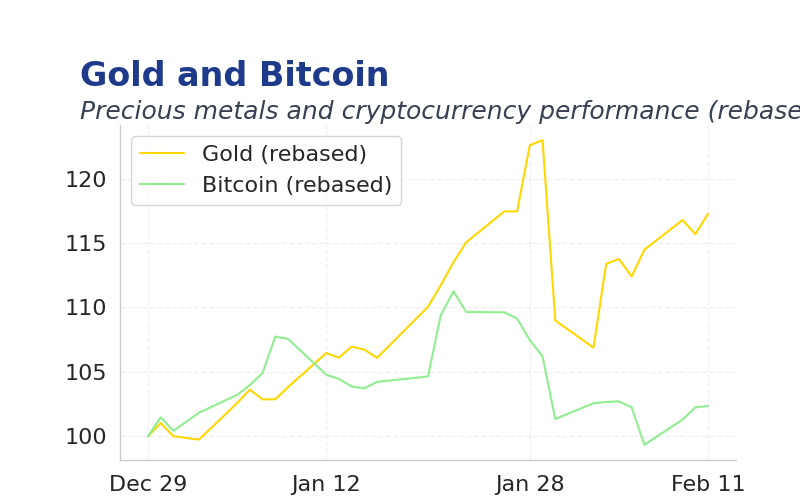

| Gold ($) | 5,003.80 | -0.93% |

| Bitcoin ($) | 67,517.04 | +0.72% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Talbot Speech | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth q/q Prel | 0.10 | 0.20 | 07:00 |

| GDP Growth y/y Prel | 1.30 | 1.20 | 07:00 |

| GDP m/m | 0.30 | 0.10 | 07:00 |

| Bus Invest q/q Prel | 1.50 | 0.40 | 07:00 |

| GDP 3-Month Avg | 0.10 | 0.20 | 07:00 |

| Goods Trade Bal | -23.7m | -22.7m | 07:00 |

| Goods Trade Bal Non-EU | -11.5m | - | 07:00 |

| Ind Prod m/m | 1.10 | 0 | 07:00 |

| Mfg Production m/m | 2.10 | 0 | 07:00 |

- UK GDP data signaled modest growth, bolstering expectations of gradual economic recovery.

- Asian equities rallied sharply, with Nikkei hitting record highs amid post-election optimism.

- Gilts yields edged lower, reflecting easing inflation pressures and supportive monetary policy.

Yesterday's Recap

UK economic data showed mixed signals, with the RICS House Price Balance at -10%, improving from -14% but below consensus expectations of -11%, highlighting persistent weakness in housing demand.

Markets reacted cautiously, with FTSE 100 rising 1.14% to 10472.11, driven by energy sector gains amid commodity demand concerns, while 10-year Gilt yields fell 3bps to 4.48% as investors digested steady inflation trends.

Brent crude dipped 0.35% to $68.80, pressured by rising US inventories, and gold slumped 0.93% to $5003.80 due to a stronger dollar following robust US jobs data.

The Day Ahead

Investors await UK GDP data, with preliminary quarterly growth expected at 0.2%, potentially revealing Q4 momentum amid slowing services activity.

Trade balance figures, anticipated at -£227B, could underscore Brexit-related export challenges.

No major BoE speeches scheduled, but market focus remains on MPC voting patterns for clues on rate cut timing.

Other Economic Notes

UK inflation pressures remain contained, with underlying rates supporting consumer spending despite global uncertainties.

Labor market dynamics show resilience, but housing market softness persists due to affordability issues.

Energy costs are moderating, aiding household budgets and broader economic stability.