UK Macro Daily(Beta Mode)

UK Growth Misses Weigh on Pound

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,941.47 | -0.00% |

| FTSE 100 | 10,402.44 | -0.67% |

| UK Natural Gas | 3.16 | +1.41% |

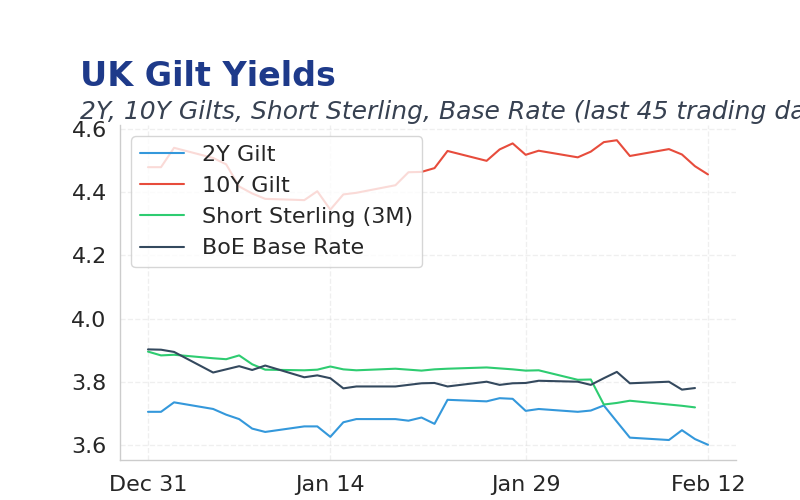

| 2 Year Gilt | 3.60 | -1 bps |

| 10 Year Gilt | 4.46 | -2 bps |

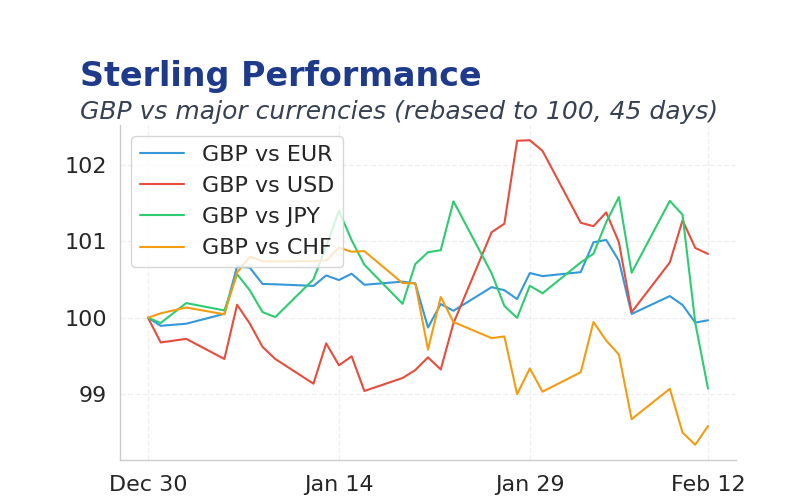

| GBP/USD | 1.360 | -0.18% |

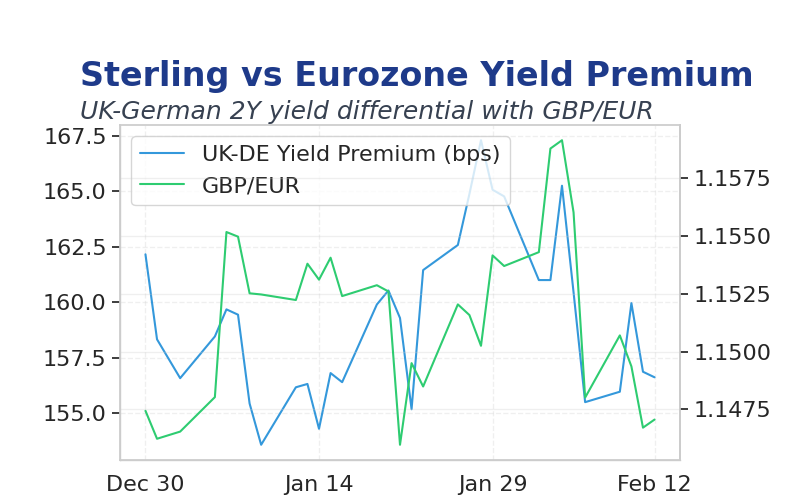

| GBP/EUR | 1.15 | -0.08% |

| GBP/JPY | 208.37 | +0.18% |

| Brent Oil | 69.40 | +0.87% |

| Gold ($) | 5,071.60 | +1.35% |

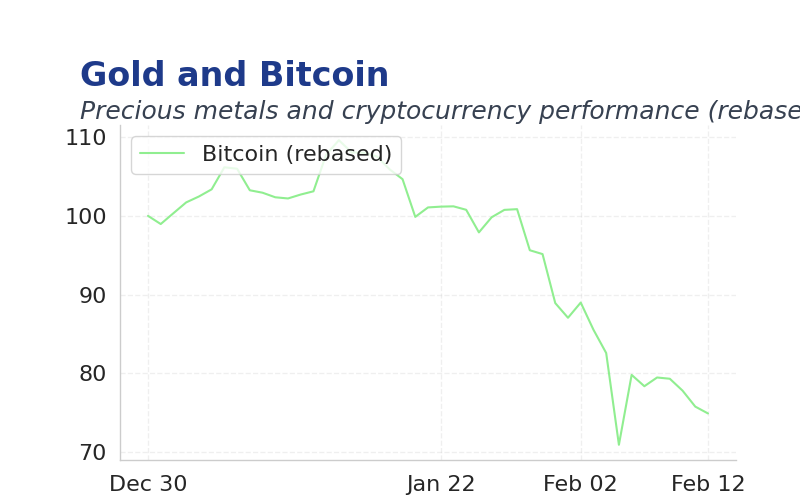

| Bitcoin ($) | 66,030.89 | -0.27% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RICS House Pr Bal | -13 | -11 | -10 |

| GDP Growth q/q Prel | 0.10 | 0.20 | 0.10 |

| GDP Growth y/y Prel | 1.20 | 1.20 | 1 |

| GDP m/m | 0.20 | 0.10 | 0.10 |

| Bus Invest q/q Prel | 1.60 | 0.40 | -2.70 |

| GDP 3-Month Avg | -0.10 | 0.20 | 0.10 |

| Goods Trade Bal | -23.6m | -22.7m | -22.7m |

| Goods Trade Bal Non-EU | -11.3m | - | -11.0m |

| Ind Prod m/m | 1.30 | 0 | -0.90 |

| Mfg Production m/m | 2.10 | 0 | -0.50 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK GDP growth missed expectations at 0.1% q/q, signaling weakening economic momentum alongside plunging business investment.

- FTSE 100 fell 0.67%, a larger-than-normal decline driven by profit-taking in financials amid subdued UK data.

- Markets tilt dovish for BoE cuts, with US inflation data later today potentially influencing global risk sentiment.

Yesterday's Recap

UK GDP q/q growth came in at 0.1%, missing consensus of 0.2%, while y/y growth slowed to 1.0% from expected 1.2%, reflecting broader economic softness.

Business investment plunged 2.7% q/q, far below forecasts of 0.4%, exacerbating concerns over production capacity.

Industrial production dropped 0.9% m/m and manufacturing fell 0.5% m/m, both worse than expected, highlighting manufacturing weakness.

Gilts yields edged lower by 1-2 bps, while sterling dipped 0.18% against the dollar as investors digested the disappointing data.

The Day Ahead

No major UK data scheduled, but markets will monitor US CPI at 1330 GMT, expected at 0.3% m/m core, for clues on Fed rate paths.

BoE Governor Bailey may comment on policy in European forums, potentially clarifying views on UK inflation trends.

Focus shifts to European PMI releases next week, which could gauge recovery pace in the eurozone.

Other Economic Notes

UK housing market signals stabilization with RICS balance improving to -10, though broader trade deficits widened.

Brexit-related trade frictions persist, pressuring non-EU goods balance despite global commodity demand.

Energy costs remain elevated, supporting natural gas prices up 1.41% amid supply concerns.