UK Macro Daily(Beta Mode)

UK Labor & Inflation Focus

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,832.76 | 0.00% |

| FTSE 100 | 10,473.69 | +0.26% |

| UK Natural Gas | 3.22 | 0.00% |

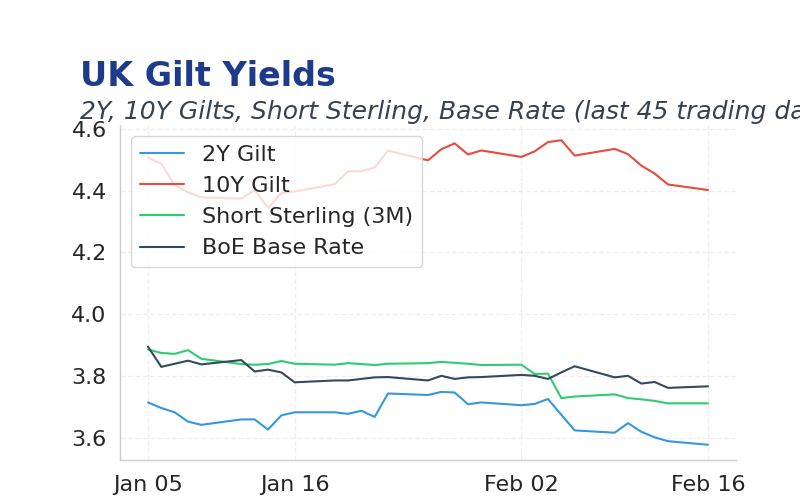

| 2 Year Gilt | 3.58 | -1 bps |

| 10 Year Gilt | 4.40 | -1 bps |

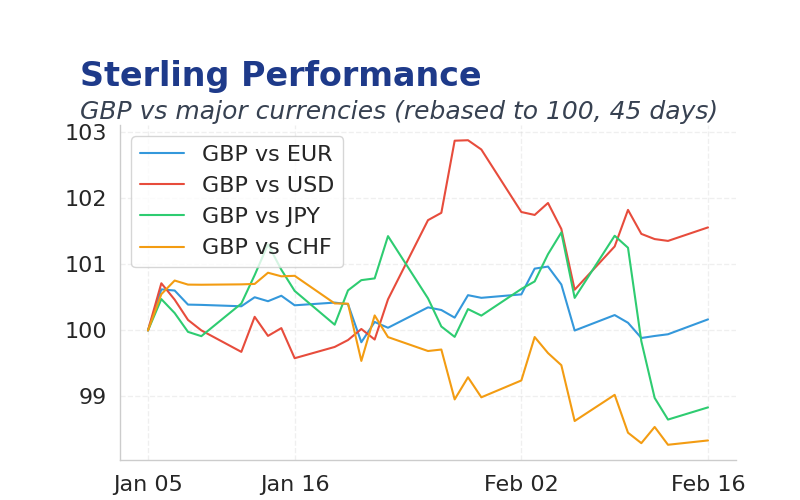

| GBP/USD | 1.361 | -0.12% |

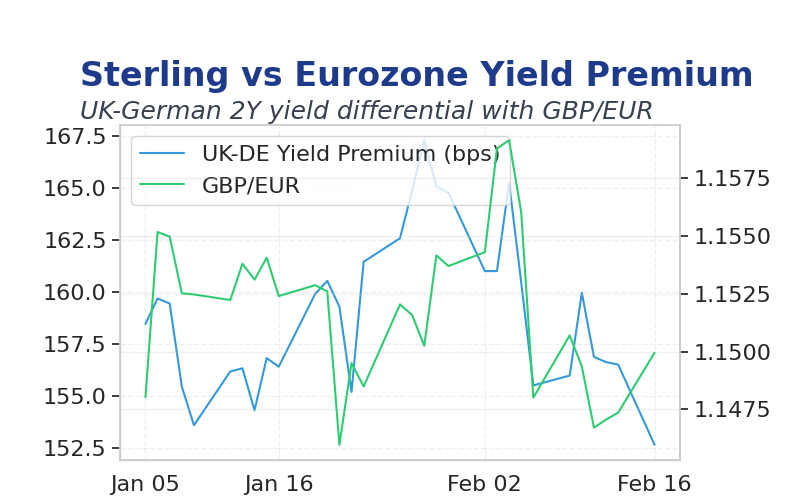

| GBP/EUR | 1.15 | -0.04% |

| GBP/JPY | 208.10 | -0.54% |

| Brent Oil | 67.52 | 0.00% |

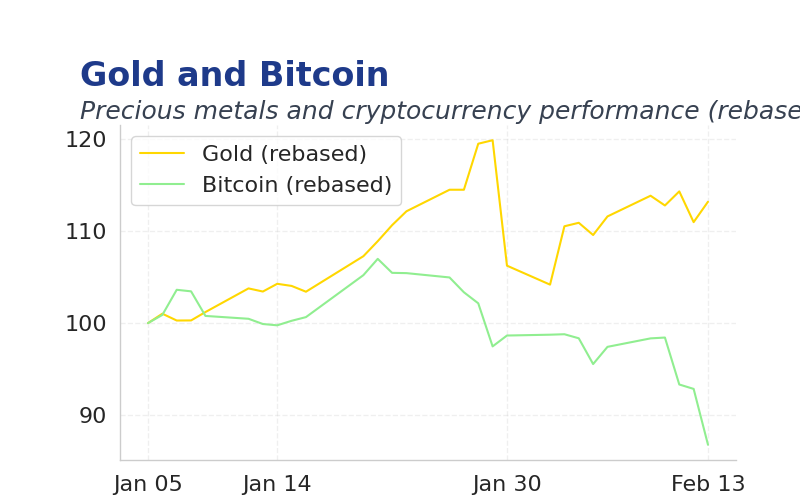

| Gold ($) | 4,923.70 | 0.00% |

| Bitcoin ($) | 68,328.96 | -0.77% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemp Rate | 5.10 | 5.10 | 07:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.70 | 4.60 | 07:00 |

| Employ Change | 82,000 | - | 07:00 |

| Inflation Rate y/y | 3.40 | 3 | 07:00 |

| Core Inflation Rate y/y | 3.20 | 3.10 | 07:00 |

| Inflation Rate m/m | 0.40 | -0.50 | 07:00 |

- UK unemployment data expected to hold steady at 5.1%, with earnings growth in focus amid cooling inflation signals.

- Markets edged higher on Friday, with FTSE 100 up 0.26% as investors digested softer US CPI readings.

- Global trade tensions persist, pressuring Sterling and highlighting UK export vulnerabilities.

Yesterday's Recap

FTSE 100 closed higher by 0.26% at 10473.69, supported by banking stocks amid mild risk appetite.

Gilt yields dipped modestly, with 2-year yields down 1bps to 3.58% and 10-year yields down 1bps to 4.40%, reflecting easing inflation concerns.

Sterling weakened slightly against the USD by 0.12% to 1.361, while holding steady against the Euro at 1.15.

Commodities traded flat, with Brent oil at 67.52 and gold at 4923.70, as geopolitical risks balanced supply dynamics.

The Day Ahead

UK unemployment rate at 07:00 is expected at 5.1%, matching previous figures, with markets watching for signs of labor market resilience.

Average earnings incl. bonus at 07:00 is forecasted at 4.6%, below the prior 4.7%, potentially signaling moderating wage pressures.

Inflation rate y/y at 07:00 is expected at 3%, down from 3.4%, with core inflation at 3.1%, guiding BoE policy expectations.

Employment change at 07:00 is projected at consensus levels, offering insights into economic momentum.

Other Economic Notes

UK services PMI remains a key indicator of domestic demand, with recent readings suggesting steady growth despite global headwinds.

Brexit-related trade frictions continue to weigh on manufacturing, highlighting the need for diversified export strategies.

Housing market dynamics show moderating prices, easing affordability concerns for consumers.