UK Macro Daily(Beta Mode)

UK Inflation Steady, Cuts Loom

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,843.22 | 0.00% |

| FTSE 100 | 10,686.18 | +1.23% |

| UK Natural Gas | 3.03 | 0.00% |

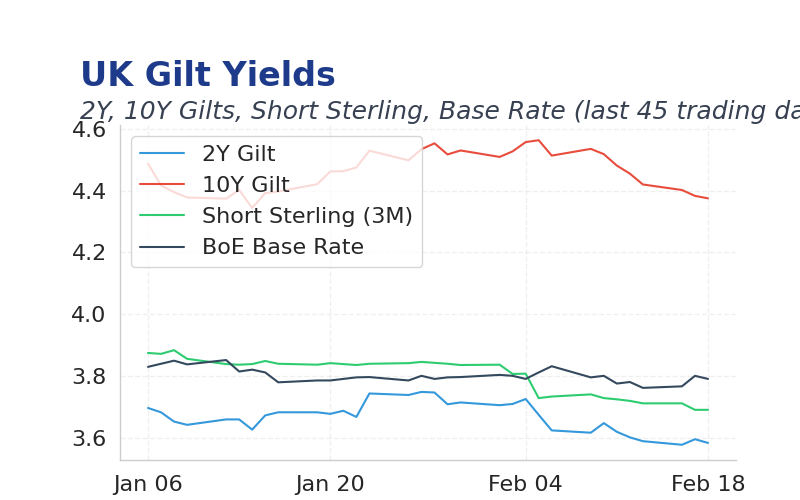

| 2 Year Gilt | 3.58 | -1 bps |

| 10 Year Gilt | 4.38 | +0 bps |

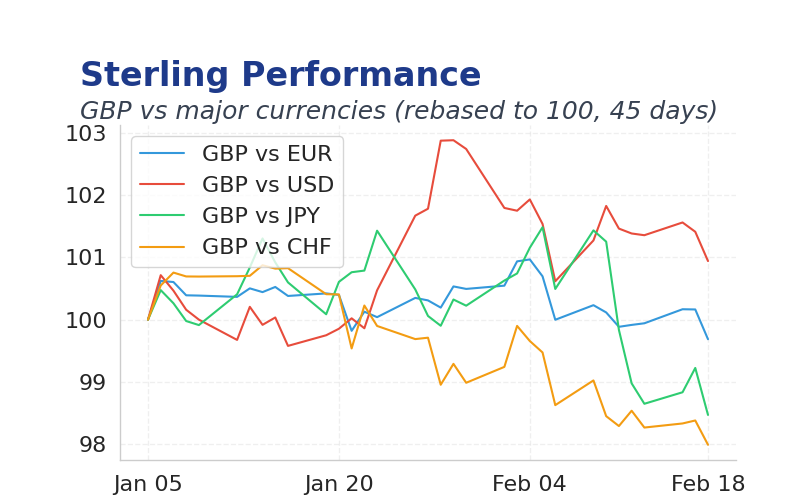

| GBP/USD | 1.350 | -0.02% |

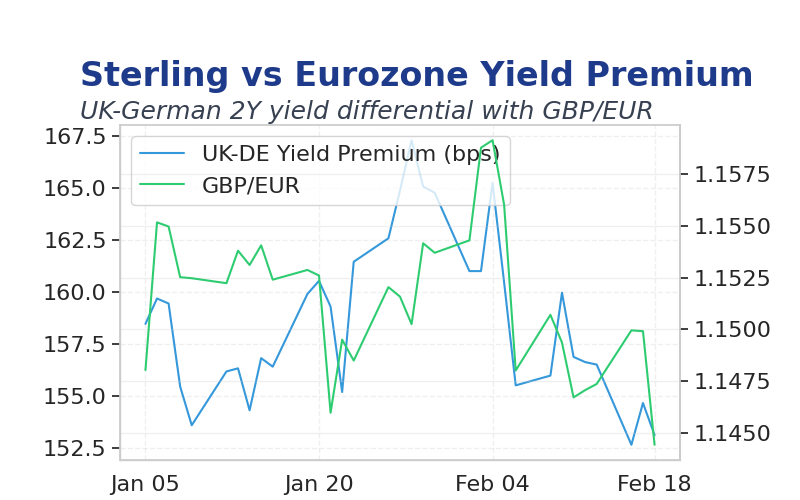

| GBP/EUR | 1.14 | -0.15% |

| GBP/JPY | 209.33 | +0.16% |

| Brent Oil | 67.42 | 0.00% |

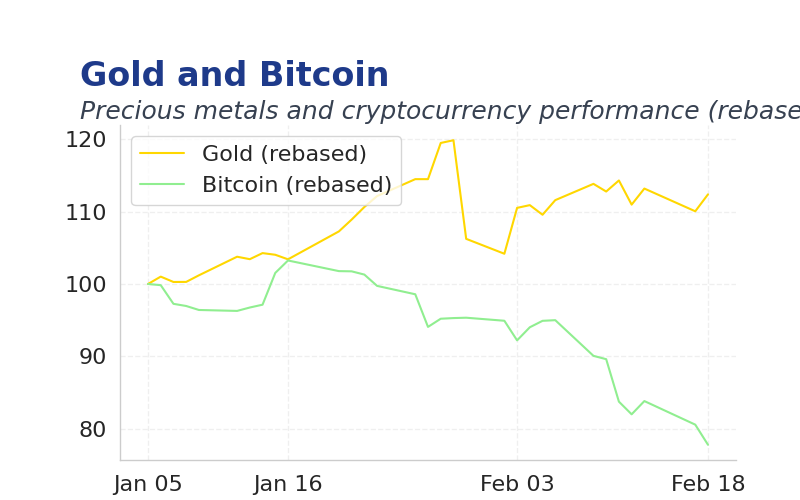

| Gold ($) | 4,882.90 | 0.00% |

| Bitcoin ($) | 67,147.43 | +1.09% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate y/y | 3.40 | 3 | 3 |

| Core Inflation Rate y/y | 3.20 | 3.10 | 3.10 |

| Inflation Rate m/m | 0.40 | -0.50 | -0.50 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| CBI Industrial Trends Orders | -30 | -28 | 11:00 |

| Retail Sales m/m | 0.40 | 0.20 | 07:00 |

| Retail Sales y/y | 2.50 | 2.80 | 07:00 |

| S&P Global Mfg PMI Flash | 51.80 | 51.80 | 09:30 |

| S&P Global Services PMI Flash | 54 | 53.60 | 09:30 |

- UK inflation y/y held at 3.0%, meeting consensus and signaling persistent but cooling pressures ahead of potential BoE easing.

- Japan's core machine orders surged 19.1% m/m, far exceeding estimates, boosting Asian equities and global risk appetite.

- FTSE 100 climbed 1.23% to 10686.18, a larger-than-normal advance driven by positive Asian cues and energy sector gains amid steady commodities.

Yesterday's Recap

UK inflation y/y came in at 3.0%, matching consensus expectations after a previous 3.4%, while core inflation held steady at 3.1% and m/m fell -0.5% as anticipated.

No BoE speeches were delivered, leaving focus on data implications for rate policy.

FTSE 100 rose 1.23% to 10686.18, a larger-than-normal gain fueled by energy and banking shares benefiting from stable Brent oil prices and global risk-on sentiment.

Gilt yields were stable, with 2-year down 1bps to 3.58% and 10-year unchanged at 4.38%, reflecting limited inflation surprises.

Sterling edged lower, GBP/USD off 0.02% to 1.350 and GBP/EUR down 0.15% to 1.14, pressured by a resilient dollar.

Commodities held firm, Brent oil at 67.42 and gold at 4882.90, while Bitcoin added 1.09% to 67147.43 amid thin trading.

The Day Ahead

UK retail sales m/m at 07:00 is expected at 0.2%, below prior 0.4%, potentially highlighting consumer caution.

Retail sales y/y at 07:00 consensus at 2.8%, up from previous 2.5%, may gauge inflationary trends.

S&P Global Manufacturing PMI Flash at 09:30 is seen at 51.8%, matching prior, alongside Services PMI at 53.6% vs 54.0%, offering insights into economic momentum.

CBI Industrial Trends Orders at 11:00 consensus -28, below prior -30, could signal manufacturing sentiment shifts.

Other Economic Notes

Australia's unemployment held at 4.1%, defying expectations for a rise, underscoring labor market resilience that could influence UK export demand. (cont...)