UK Macro Daily(Beta Mode)

Oil Surge Hawks BoE Cuts

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,881.31 | +0.56% |

| FTSE 100 | 10,627.04 | -0.55% |

| UK Natural Gas | 3.01 | -0.66% |

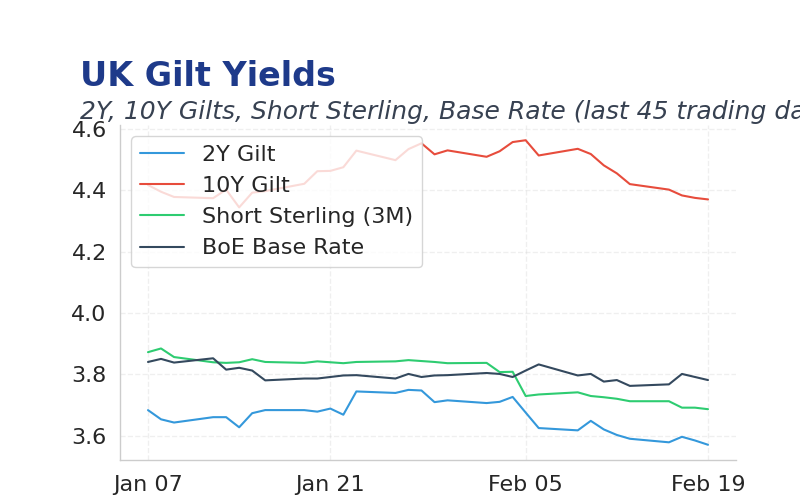

| 2 Year Gilt | 3.57 | -1 bps |

| 10 Year Gilt | 4.37 | +0 bps |

| GBP/USD | 1.345 | -0.09% |

| GBP/EUR | 1.14 | +0.03% |

| GBP/JPY | 208.71 | -0.01% |

| Brent Oil | 70.35 | +4.35% |

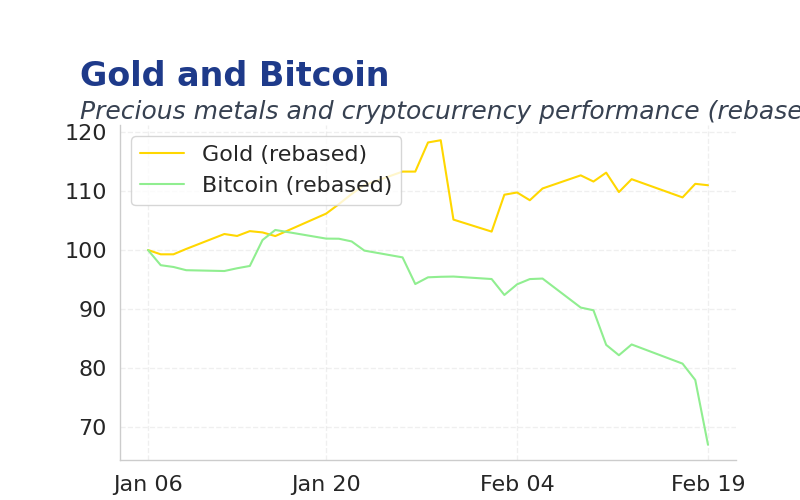

| Gold ($) | 4,986.50 | +2.12% |

| Bitcoin ($) | 67,699.10 | +1.09% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| CBI Industrial Trends Orders | -30 | -28 | -28 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Retail Sales m/m | 0.40 | 0.20 | 02:00 |

| Retail Sales y/y | 2.50 | 2.80 | 02:00 |

| S&P Global Mfg PMI Flash | 51.80 | 51.50 | 04:30 |

| S&P Global Services PMI Flash | 54 | 53.50 | 04:30 |

| Tuesday (2026-02-24) | |||

| CBI Distributive Trades | -17 | - | 06:00 |

| Friday (2026-02-27) | |||

| GFK Consumer Confidence Index | -16 | - | 19:01 |

| Nationwide Housing Prices m/m | 0.30 | - | 02:00 |

| Nationwide Housing Prices y/y | 1 | - | 02:00 |

- Brent crude surged 4.35% to $70.35 amid US-Iran tensions, boosting UK inflation risks.

- UK industrial orders met expectations at -28, signaling ongoing economic softness.

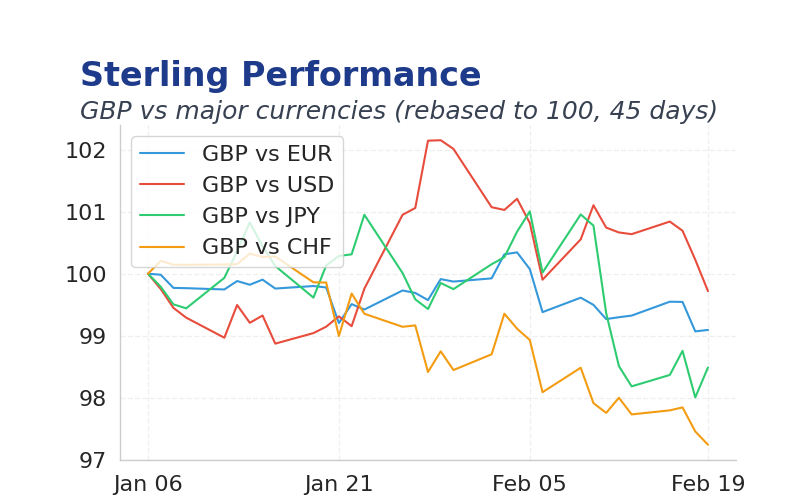

- Sterling edged down 0.09% to 1.345 against USD as global risk aversion rose.

Yesterday's Recap

UK industrial orders from CBI met consensus at -28, indicating flat business activity in a weak economic backdrop.

FTSE 100 fell 0.55% to 10,627.04, pressured by energy sector volatility.

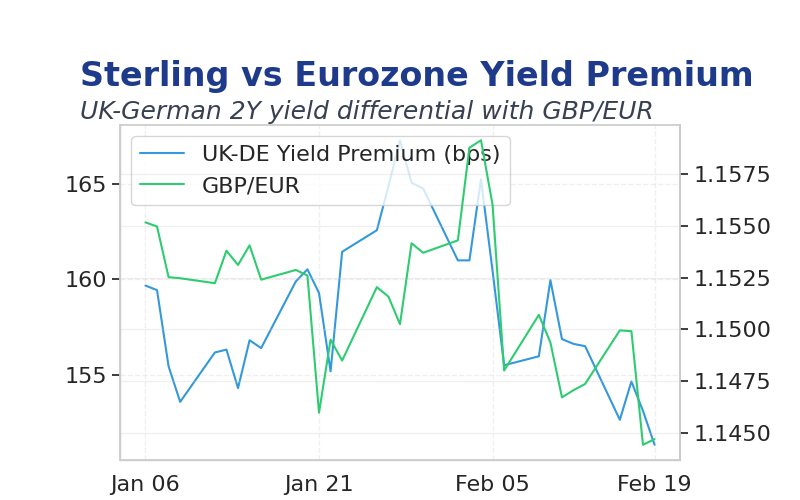

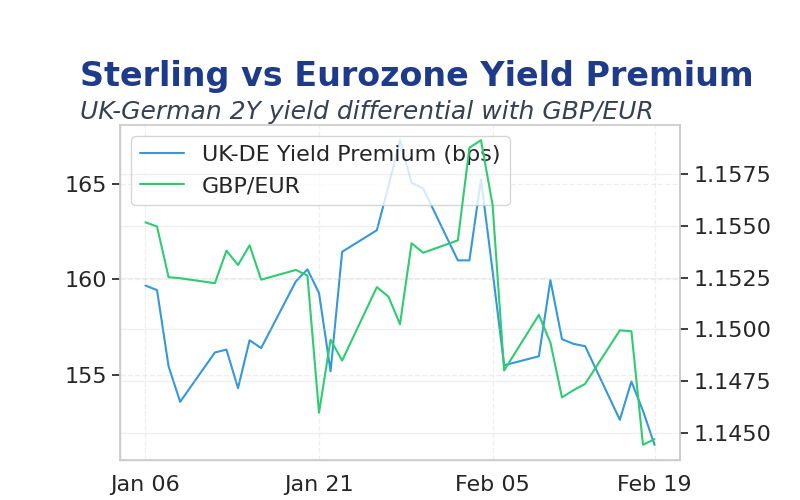

Gilt yields were steady, with 2-year down 1 bps to 3.57% and 10-year unchanged at 4.37%.

Sterling dipped 0.09% against USD to 1.345 but gained 0.03% versus EUR.

Commodities rallied, with Brent oil up 4.35% to $70.35 and gold 2.12% to $4,986.50, driven by geopolitical fears.

The Day Ahead

Retail sales data at 02:00 is expected at 0.2% m/m versus previous 0.4%, with y/y at 2.8% versus 2.5%, potentially revealing consumer weakness.

S&P Global PMI flashes at 04:30 may show manufacturing at 51.5 versus 51.8 and services at 53.5 versus 54.0, influencing BoE growth views.

CBI distributive trades survey at 06:00 lacks consensus, but could signal retail sentiment shifts.

Other Economic Notes

UK housing prices rose 3.2% YoY per Nationwide, supporting labor market resilience.

Brexit impacts persist in trade flows, with EU relations under scrutiny.

Energy costs remain elevated, pressuring inflation despite gas prices dipping 0.66%.