UK Macro Daily(Beta Mode)

February 23, 2026

robomacro.com

BoE Easing Outlook Amid Tariff Reversal

| Prior Close | ||

|---|---|---|

| Asset | Level | Days Change |

| S&P 500 | 6,861.89 | -0.28% |

| FTSE 100 | 10,627.00 | -0.55% |

| UK Natural Gas | 3.00 | -0.50% |

| 2 Year Gilt | Data Unavailable | Data Unavailable |

| 10 Year Gilt | Data Unavailable | Data Unavailable |

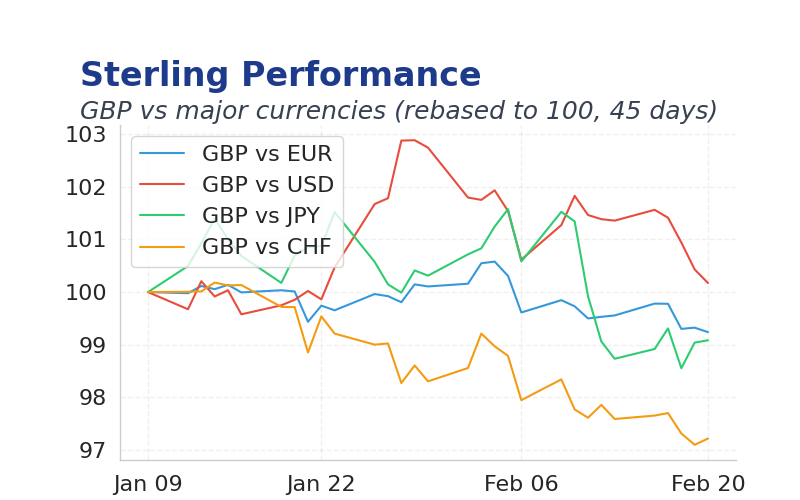

| GBP/USD | 1.350 | -0.51% |

| GBP/EUR | 1.14 | +0.02% |

| GBP/JPY | 208.75 | +0.49% |

| Brent Oil | 71.66 | +1.86% |

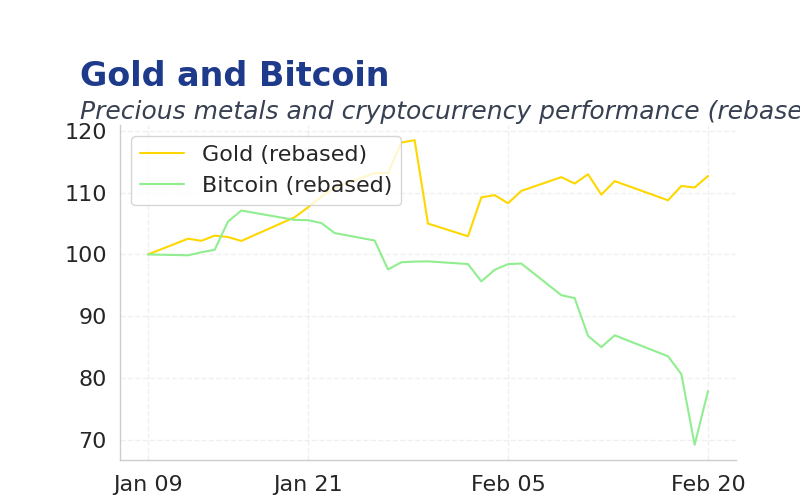

| Gold ($) | 4,975.90 | -0.21% |

| Bitcoin ($) | Data Unavailable | Data Unavailable |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Chart loading...

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UK inflation ticked higher, contributing to a hawkish tone as markets priced fewer BoE cuts.

- Today's BoE Governor speech may clarify easing pace amid weak GDP data.

- Global tariff reversal pressured equities but heightened UK export risks.

Friday's Recap

UK GDP growth disappointed at 1.4% annualized, missing consensus and signaling economic weakness.

Gilt yields remained stable on inflation data.

Sterling weakened 0.51% against the USD, pressured by tariff uncertainties.

FTSE 100 fell 0.55%, reflecting broader market caution.

The Day Ahead

Markets await BoE Governor Bailey's speech on monetary policy, potentially signaling rate cut timing.

UK retail sales data at 9:30am may show consumer resilience or fragility.

No major data releases, but global oil volatility could spillover to Sterling.

Other Economic Notes

UK housing prices rose 3.2% YoY per Nationwide, supporting consumer confidence.

Claimant count increased, indicating labor market slack.

Brexit-related trade disruptions persisted amid tariff debates.

Page 1