UK Macro Daily(Beta Mode)

Housing Data Awaited, FTSE Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,910.60 | +0.59% |

| FTSE 250 | 23,757.20 | +0.16% |

| GBP/USD | 1.34 | -0.81% |

| GBP/EUR | 1.14 | -0.26% |

| GBP/JPY | 209.94 | -0.15% |

| Brent Crude | 78.73 | +8.62% |

| Gold | 5,398.00 | +3.20% |

| UK Nat Gas | 2.96 | +3.60% |

| Bitcoin | 66,233.93 | +0.75% |

| UK 2Y Gilt | - | - |

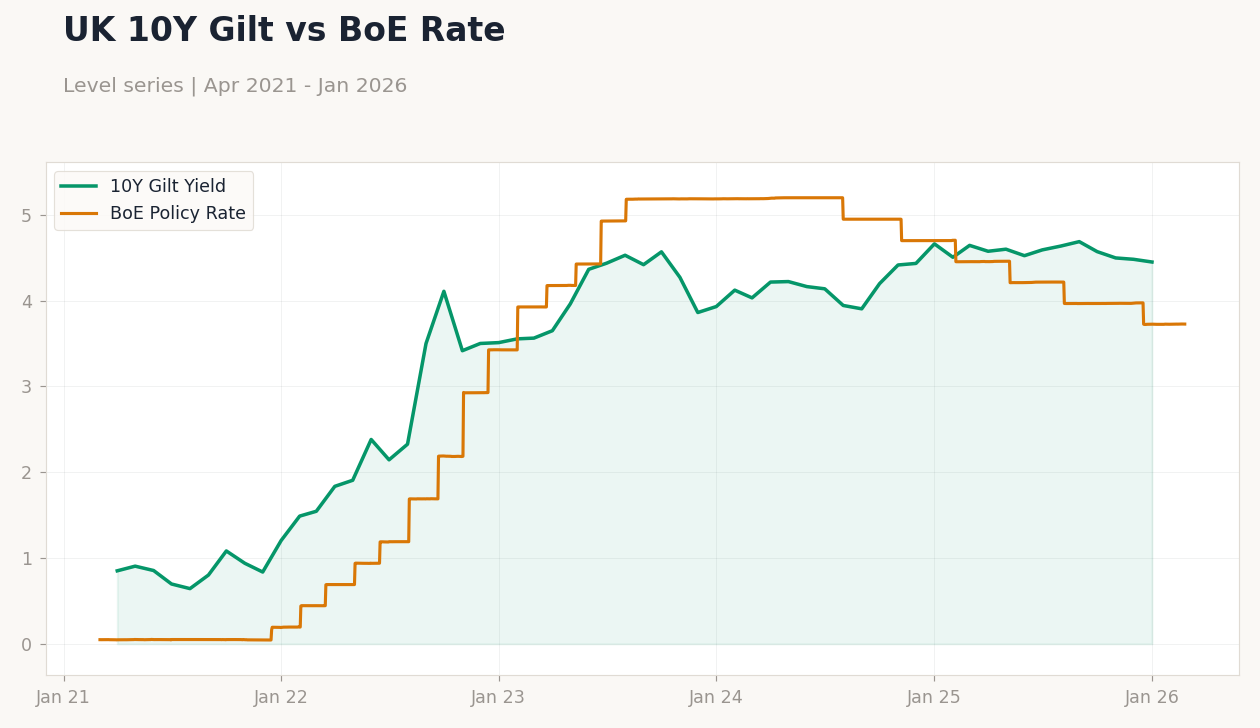

| UK 10Y Gilt | 4.45% | -0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Nationwide Housing Prices Month-over-Month | 0.30 | 0.30 | - |

| Nationwide Housing Prices Year-over-Year | 1 | 0.70 | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoE Consumer Credit | 1,524m | - | 23:30 |

| Mortgage Approvals | 61,010 | 62,000 | 23:30 |

| Mortgage Lending Level | 4,600m | - | 23:30 |

| Thursday (2026-03-05) | |||

| S&P Global Construction PMI | 46.40 | 47.90 | 23:30 |

| Friday (2026-03-06) | |||

| Halifax House Price Index Month-over-Month | 0.70 | 0.40 | 21:00 |

| Halifax House Price Index Year-over-Year | 1 | - | 21:00 |

- UK housing prices pending release showed consensus expectations, with MoM at 0.3% and YoY at 0.7%, amid market anticipation for domestic resilience.

- FTSE 100 rose 0.59% on commodity strength, while GBP weakened on global risks, with USD pair down 0.81%.

- Geopolitical tensions drove Brent Crude up 8.62%, boosting inflation concerns and safe-haven assets like gold.

Yesterday's Recap

Yesterday's UK calendar featured pending Nationwide Housing Prices, with Month-over-Month consensus at 0.3% matching prior, and Year-over-Year at 0.7% versus prior 1%, as actuals remained unreported. This anticipation contributed to a 0.81% decline in GBP/USD to 1.34, reflecting caution on housing trends. The FTSE 100 advanced 0.59% to 10,910.60, driven by energy stocks amid an 8.62% surge in Brent Crude to 78.73, fueled by Middle East conflicts.

FTSE 250 edged up 0.16% to 23,757.20, buoyed by slight domestic sentiment. GBP/EUR fell 0.26% to 1.14 and GBP/JPY dipped 0.15% to 209.94, as the 10-year Gilt yield eased 0.70% to 4.45%. Gold rallied 3.20% to 5,398.00 for safe-haven demand, while UK Natural Gas rose 3.60% to 2.96 on supply worries.

Bitcoin gained 0.75% to 66,233.93. Markets maintained stability, eyeing upcoming data for direction.

The Day Ahead

Today's UK releases include BoE Consumer Credit at 23:30 ET, prior 1.524 billion with no consensus, Mortgage Approvals expected at 62,000 versus prior 61,010, and Mortgage Lending Level prior 4.6 billion without forecast, providing borrowing insights amid high rates. No events tomorrow. Thursday features S&P Global Construction PMI at 23:30 ET, consensus 47.9 against prior 46.4, indicating sector trends.

Friday brings Halifax House Price Index MoM at 21:00 ET, consensus 0.4% versus prior 0.7%, and YoY prior 1% with no consensus. These could sway sterling and yields ahead of policy signals.

Other Economic Notes

UK economy faces ongoing inflation at verified CPI YoY of 3.40%, straining households despite moderation. Unemployment at 5.10% signals labor slack, potentially curbing wages and aiding BoE caution. Housing pressures from high rates may dampen confidence and spending, as recent indicators suggest affordability challenges.

Global Macro News

Escalating Middle East tensions, with US-Israel strikes on Iran and Hezbollah retaliation, including explosions in Gulf cities and Beirut evacuations, lifted Brent Crude and stoked UK energy inflation risks. (cont...)