UK Macro Daily(Beta Mode)

UK Housing Mixed, FTSE Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,780.10 | -1.20% |

| FTSE 250 | 22,694.21 | -3.11% |

| GBP/USD | 1.33 | -0.63% |

| GBP/EUR | 1.15 | +0.21% |

| GBP/JPY | 209.98 | -0.42% |

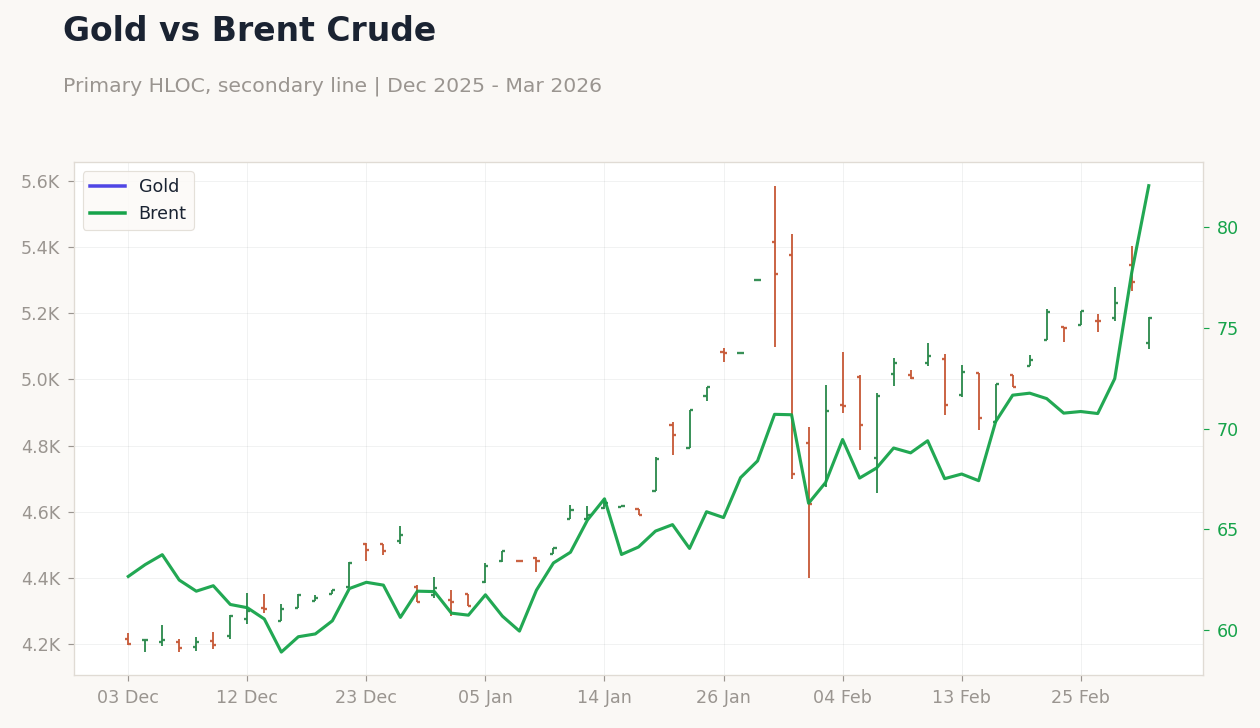

| Brent Crude | 81.88 | +5.33% |

| Gold | 5,183.70 | -2.09% |

| UK Nat Gas | 3.05 | +2.91% |

| Bitcoin | 68,423.76 | -0.51% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.45% | -0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Nationwide Housing Prices Month-over-Month | 0.30 | 0.30 | 0.30 |

| Nationwide Housing Prices Year-over-Year | 1 | 0.70 | 1 |

| BoE Consumer Credit | 1,652m | 1,700m | 1,812m |

| Mortgage Approvals | 61,010 | 62,000 | 60,000 |

| Mortgage Lending Level | 4,490m | - | 4,080m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-03-05) | |||

| S&P Global Construction PMI | 46.40 | 47 | 23:30 |

| Friday (2026-03-06) | |||

| Halifax House Price Index Month-over-Month | 0.70 | 0.30 | 21:00 |

| Halifax House Price Index Year-over-Year | 1 | 0.90 | 21:00 |

- Nationwide housing prices met MoM consensus at 0.3% but beat YoY at 1% vs 0.7%; consumer credit topped forecasts at £1.812bn.

- Mortgage approvals fell short at 60k vs 62k expected, with lending at £4.08bn below prior £4.49bn.

- FTSE 100 down 1.20%, 250 off 3.11%; GBP weaker vs USD but up on EUR; Brent surged 5.33%.

Yesterday's Recap

Yesterday's data revealed mixed UK housing and credit signals. Nationwide Housing Prices rose 0.3% MoM, aligning with consensus and prior, while YoY hit 1%, exceeding the 0.7% forecast. BoE Consumer Credit increased to £1.812 billion, above the £1.7 billion expected and previous £1.652 billion, indicating strong borrowing.

However, Mortgage Approvals slipped to 60,000, missing the 62,000 consensus from prior 61,010, and Mortgage Lending dropped to £4.08 billion versus £4.49 billion. These results weighed on sentiment, with the FTSE 100 closing down 1.20% at 10,780.10 amid energy and mining weakness. The FTSE 250 declined 3.11% to 22,694.21, hit by domestic spending fears.

GBP/USD fell 0.63% to 1.33, GBP/JPY dropped 0.42% to 209.98, but GBP/EUR rose 0.21% to 1.15. UK 10Y Gilt yield eased 0.70% to 4.45%, suggesting safe-haven flows.

The Day Ahead

No key UK releases today, allowing markets to digest recent data. Focus turns to Thursday's S&P Global Construction PMI, forecasted at 47 from 46.4, potentially indicating sector improvement despite challenges. Friday's Halifax House Price Index is eyed, with MoM consensus at 0.3% from 0.7% and YoY at 0.9% from 1%, providing more housing clarity.

Globally, watch Middle East tensions for energy impacts on UK imports. Any surprise BoE remarks on inflation could move sterling and gilts.

Other Economic Notes

UK CPI YoY is at 3.40%, above the BoE's 2% target, driven by services and wage pressures. Unemployment stands at 5.10%, signaling labor market cooling that may temper wages but heighten downturn risks. The trade deficit leaves households exposed to global energy and food price spikes, as seen in recent oil and gas surges.

Global Macro News

Brent crude jumped 5.33% to 81.88 amid Strait of Hormuz concerns, raising UK import costs and inflation risks. UK natural gas rose 2.91% to 3.05, tied to global dynamics and weather. Gold fell 2.09% to 5,183.70, while Bitcoin dipped 0.51% to 68,423.76, reflecting risk aversion.

(cont...)