UK Macro Daily(Beta Mode)

UK Growth Forecast Cut on War Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,484.10 | -2.75% |

| FTSE 250 | 22,896.67 | +0.89% |

| GBP/USD | 1.34 | +0.11% |

| GBP/EUR | 1.15 | -0.06% |

| GBP/JPY | 210.66 | -0.10% |

| Brent Crude | 83.08 | +2.06% |

| Gold | 5,185.10 | +1.52% |

| UK Nat Gas | 2.96 | -3.01% |

| Bitcoin | 72,462.42 | +6.10% |

| UK 2Y Gilt | - | - |

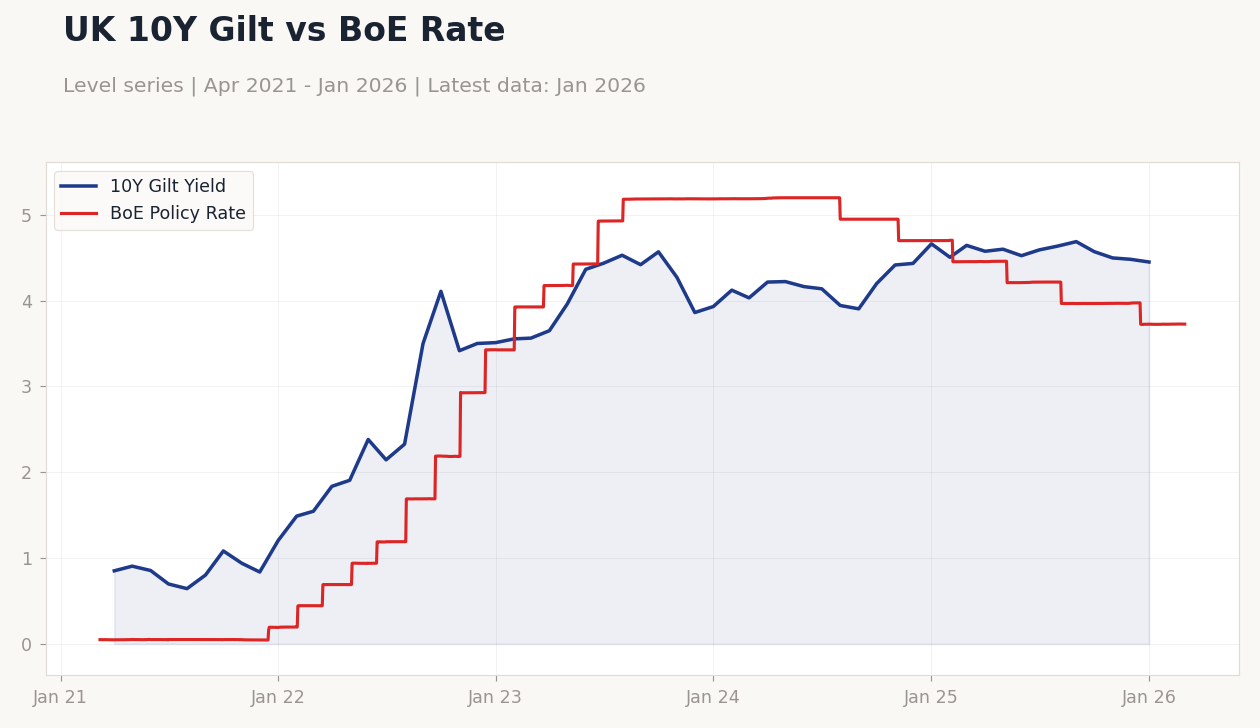

| UK 10Y Gilt | 4.45% | -0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Nationwide Housing Prices Month-over-Month | 0.30 | 0.30 | 0.30 |

| Nationwide Housing Prices Year-over-Year | 1 | 0.70 | 1 |

| BoE Consumer Credit | 1,652m | 1,700m | 1,812m |

| Mortgage Approvals | 61,010 | 62,000 | 60,000 |

| Mortgage Lending Level | 4,490m | - | 4,080m |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-03-05) | |||

| S&P Global Construction PMI | 46.40 | 47 | 23:30 |

| Friday (2026-03-06) | |||

| Halifax House Price Index Month-over-Month | 0.70 | 0.30 | 21:00 |

| Halifax House Price Index Year-over-Year | 1 | 0.90 | 21:00 |

- UK government slashes 2026 growth forecast, citing Iran war risks and weaker outlook.

- Housing data mixed: Nationwide prices met MoM consensus but beat YoY; consumer credit rose while mortgage approvals fell.

- Markets volatile: FTSE 100 down 2.75%, FTSE 250 up 0.89%, gilt yields ease, sterling mixed.

Yesterday's Recap

Yesterday's UK data showed mixed signals in housing and credit. Nationwide Housing Prices rose 0.3% month-over-month, matching consensus and previous, while year-over-year gained 1% against expected 0.7%. BoE Consumer Credit increased to £1.812 billion, beating consensus £1.7 billion and prior £1.652 billion, suggesting solid borrowing.

However, Mortgage Approvals dropped to 60,000 versus consensus 62,000 and previous 61,010, with Mortgage Lending at £4.08 billion below prior £4.49 billion. Markets were uneven: FTSE 100 fell 2.75% to 10,484.10 on global risk-off, while FTSE 250 rose 0.89% to 22,896.67 amid domestic resilience. Sterling had slight gains with GBP/USD up 0.11% to 1.34, but GBP/EUR down 0.06% to 1.15 and GBP/JPY down 0.10% to 210.66.

Brent Crude climbed 2.06% to 83.08, Gold up 1.52% to 5,185.10, UK Nat Gas down 3.01% to 2.96, Bitcoin up 6.10% to 72,462.42. UK 10Y Gilt yield eased 0.70 percentage points to 4.45%, reflecting safe-haven demand after the growth forecast cut.

The Day Ahead

Today's highlight is the S&P Global Construction PMI at 23:30 ET, with consensus at 47 from previous 46.4, which could indicate a slight sector uptick. This follows recent housing weakness and may shape views on UK growth. Tomorrow brings the Halifax House Price Index at 21:00 ET, with month-over-month consensus at 0.3% versus prior 0.7%, and year-over-year at 0.9% from 1%.

These will offer more on property trends amid high rates. No BoE events today, but markets eye reactions to fiscal updates and geopolitical risks. Focus remains on alignment with the revised economic outlook.

Other Economic Notes

Chancellor Rachel Reeves' Spring Forecast 2026 cut growth projections, noting Iran war risks could worsen inflation and trade disruptions, even before escalation. This highlights challenges like 3.40% YoY CPI and 5.10% unemployment. Anti-immigration steps, including ending study visas for Myanmar, Afghanistan, Cameroon, and Sudan, may affect labor supply.

(cont...)