Other Economic Notes

Broader UK economic themes include persistent inflationary pressures, with CPI holding at 3.40% year-over-year, complicating the Bank of England's path to easing. Unemployment at 5.10% underscores labor market softening, potentially supporting dovish policy shifts if growth data weakens further. Housing and retail sectors face headwinds from elevated borrowing costs, as evidenced by yesterday's BRC miss and upcoming RICS data.

Global Macro News

Escalating Middle East conflict, particularly involving Iran, has driven oil prices above $100 per barrel in recent sessions, rattling commodity markets and prompting reassessments of global rate cut timelines. This energy shock raises stagflation risks, reminiscent of the 1970s, with investors bracing for higher inflation and slower growth that could pressure UK imports and consumer prices. In the US, strong jobs data has bolstered the dollar, indirectly supporting GBP/USD gains but adding to global hawkishness.

European Central Bank dovishness contrasts with this, stabilizing GBP/EUR but exposing UK vulnerabilities to energy-driven inflation. Geopolitical tensions, including Israel's use of white phosphorus in Lebanon, heighten safe-haven demand for gold, which fell 0.45% to 5,206.10 but remains elevated. Bitcoin's 1.68% rise to 69,552.30 reflects crypto resilience amid fiat volatility.

Overall, these factors amplify UK exposure to imported inflation, with potential spillovers into BoE policy. China's weak demand signals further weigh on global commodities, indirectly affecting UK trade balances.

BoE Watch

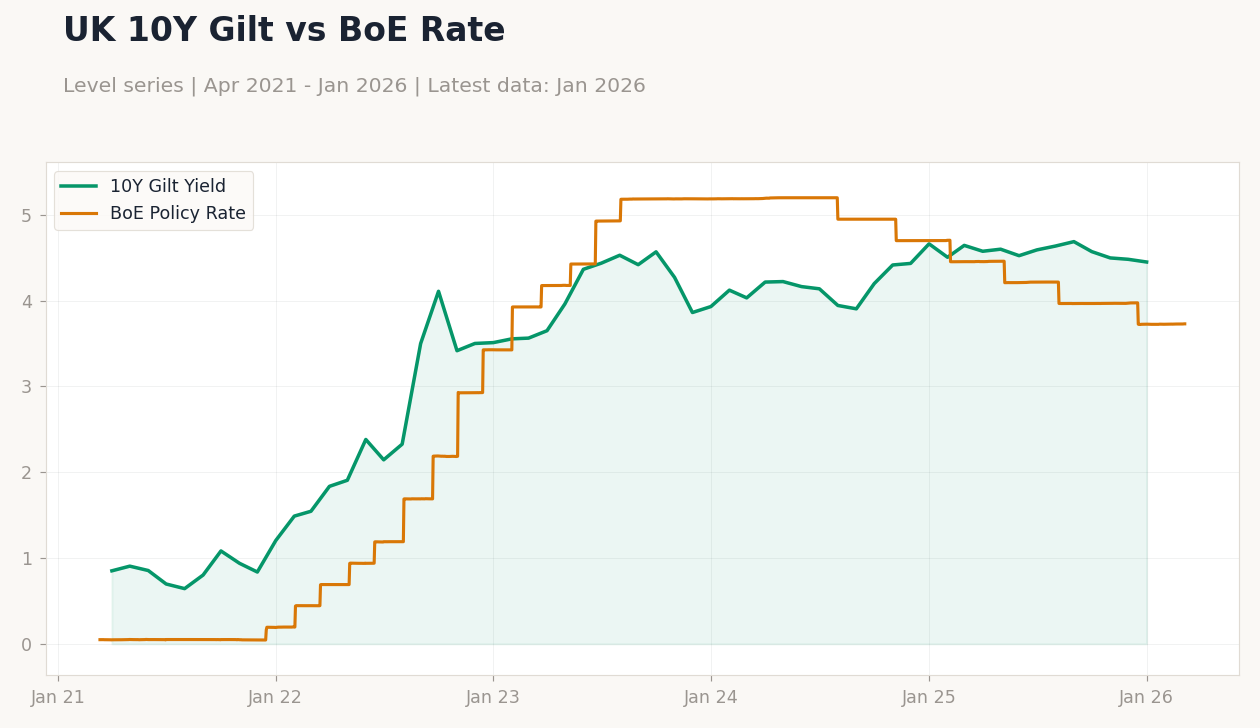

The Bank of England maintained its Bank Rate at 3.73% in the latest decision, aligning with forward guidance emphasizing data-dependent easing amid sticky inflation. Recent communications from MPC members have stressed vigilance on services inflation, which remains elevated despite headline CPI at 3.40% year-over-year, suggesting no imminent cuts without clearer disinflation signals. The February inflation report highlighted upside risks from energy prices, particularly amid Middle East tensions, reinforcing a cautious quantitative tightening stance with ongoing balance sheet reduction.

Governor Bailey's upcoming speech could elaborate on these themes, potentially signaling patience on rate moves if growth data like Friday's GDP disappoints. Markets interpret this as reducing odds of a near-term cut, supporting higher Gilt yields despite yesterday's dip. Forward guidance continues to prioritize inflation returning sustainably to 2%, with no explicit vote split details available from recent meetings.

This positioning implies limited sterling volatility unless global shocks intensify.

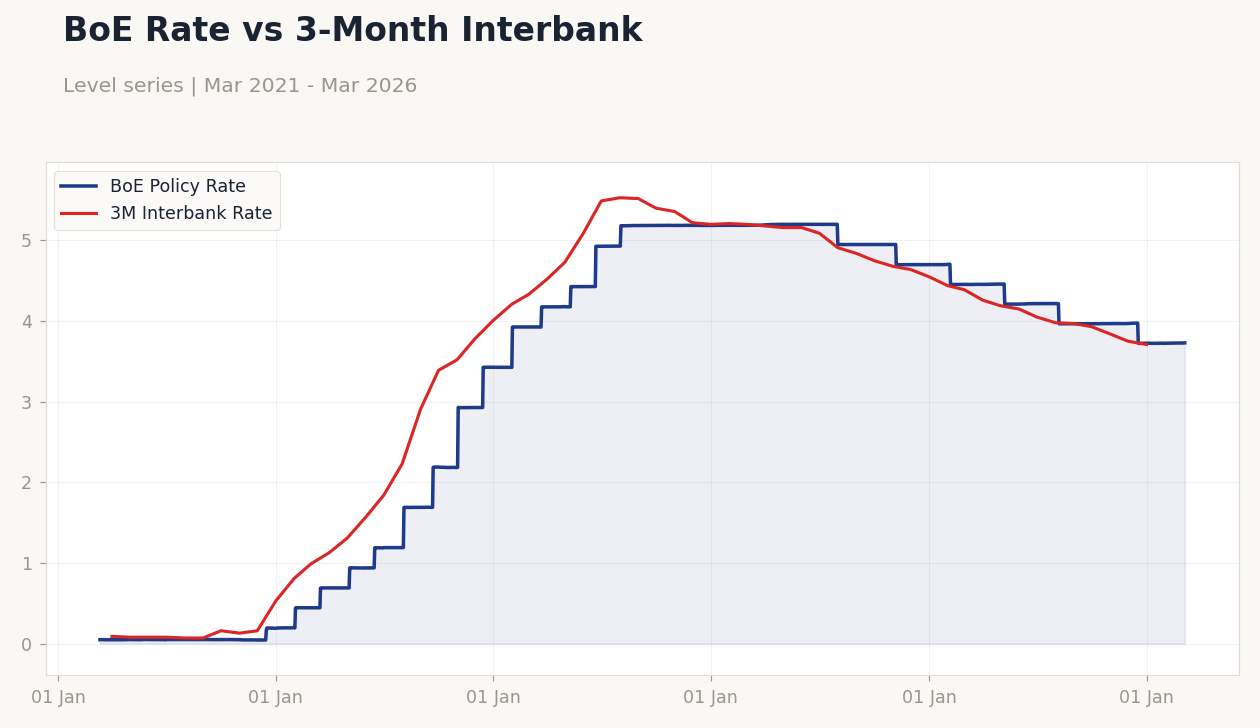

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.73 (2026-03-06) | Range: 0.045–5.2 | Trend(6pt): 0.049,0.9398,5.185,4.7,3.73,3.73 | 3M Interbank Rate: 3.71 (2026-01-01) | Range: 0.07–5.53 | Trend(6pt): 0.09,1.57,5.53,4.75,3.75,3.71

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.73 (2026-03-06) | Range: 0.045–5.2 | Trend(6pt): 0.049,0.9398,5.185,4.7,3.73,3.73 | 3M Interbank Rate: 3.71 (2026-01-01) | Range: 0.07–5.53 | Trend(6pt): 0.09,1.57,5.53,4.75,3.75,3.71