UK Macro Daily(Beta Mode)

Retail Miss, FTSE Slips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,353.80 | -0.56% |

| FTSE 250 | 22,168.74 | -0.95% |

| GBP/USD | 1.33 | -0.37% |

| GBP/EUR | 1.16 | -0.03% |

| GBP/JPY | 212.87 | +0.34% |

| Brent Crude | 96.54 | -3.90% |

| Gold | 5,106.40 | -0.18% |

| UK Nat Gas | 3.28 | +1.48% |

| Bitcoin | 71,608.59 | +2.00% |

| UK 2Y Gilt | - | - |

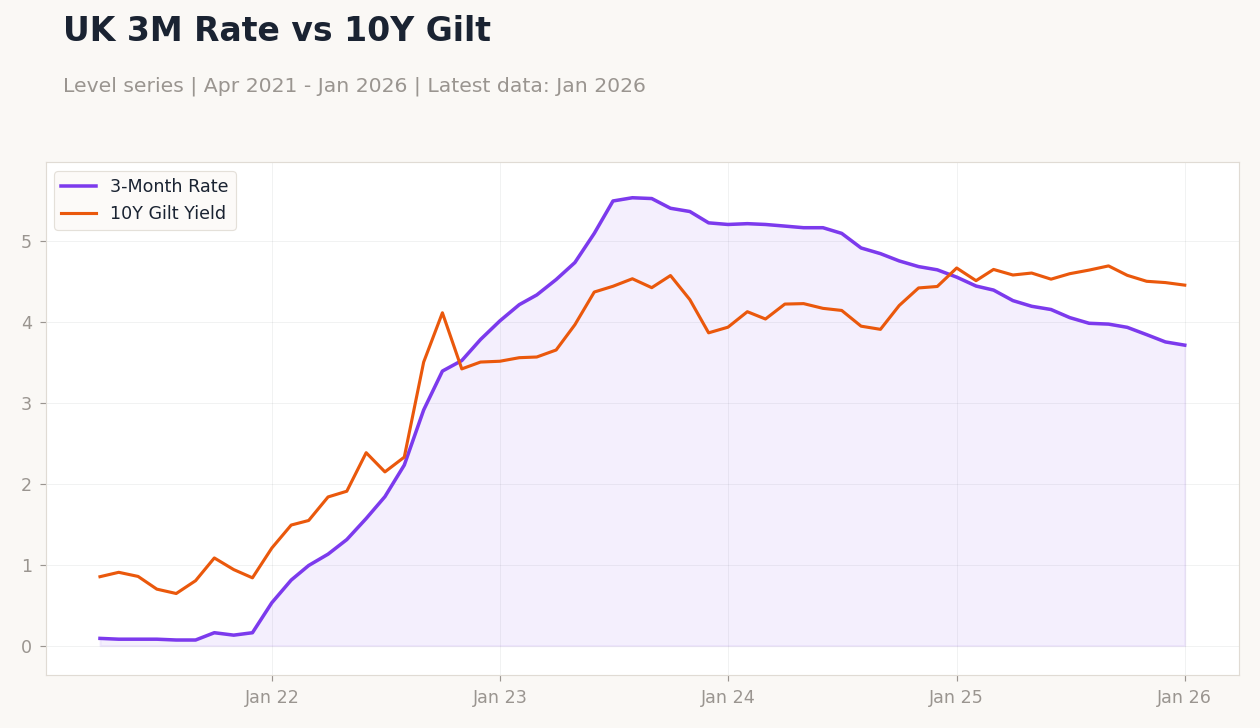

| UK 10Y Gilt | 4.45% | -0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BRC Retail Sales Monitor Year-over-Year | 2.30 | 2.40 | 0.70 |

| RICS House Price Balance | -10 | -9 | -12 |

| BoE Gov Bailey Speech | - | - | - |

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.729 (2026-03-10) | Range: 0.045–5.2 | Trend(6pt): 0.0497,0.9399,5.185,4.7,3.73,3.729 | 3M Interbank Rate: 3.71 (2026-01-01) | Range: 0.07–5.53 | Trend(6pt): 0.09,1.57,5.53,4.75,3.75,3.71

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.729 (2026-03-10) | Range: 0.045–5.2 | Trend(6pt): 0.0497,0.9399,5.185,4.7,3.73,3.729 | 3M Interbank Rate: 3.71 (2026-01-01) | Range: 0.07–5.53 | Trend(6pt): 0.09,1.57,5.53,4.75,3.75,3.71

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Month-over-Month | 0.10 | 0.20 | 23:00 |

| GDP 3-Month Avg | 0.10 | 0.30 | 23:00 |

| Goods Trade Balance | -22,720m | -22,200m | 23:00 |

| Goods Trade Balance Non-EU | -10,990m | - | 23:00 |

| Industrial Production Month-over-Month | -0.90 | 0.20 | 23:00 |

| Manufacturing Production Month-over-Month | -0.50 | 0.20 | 23:00 |

- UK retail sales disappointed with BRC YoY at 0.7% vs 2.4% consensus, signaling consumer weakness.

- RICS house prices fell to -12 vs -9 expected, pressuring housing market outlook.

- FTSE 100 dropped 0.56% amid oil volatility and global tensions.

Yesterday's Recap

UK data releases yesterday highlighted softening economic momentum, with BRC Retail Sales Monitor YoY coming in at 0.7%, well below the 2.4% consensus and prior 2.3%, indicating subdued consumer spending amid high costs. RICS House Price Balance deteriorated to -12, missing the -9 forecast and worsening from -10, reflecting ongoing affordability challenges in the property sector. BoE Governor Bailey delivered a speech emphasizing data-dependent policy amid persistent inflation risks, though no new guidance shifted market bets.

Market moves saw the FTSE 100 close at 10,353.80, down 0.56%, driven by energy sector drags from Brent crude's 3.90% fall to 96.54. FTSE 250 fell 0.95% to 22,168.74, hit by broader risk aversion. Sterling weakened modestly, with GBP/USD at 1.33 (-0.37%) and GBP/EUR at 1.16 (-0.03%), while GBP/JPY rose 0.34% to 212.87 on yield support.

UK 10Y Gilt yield eased 0.70% to 4.45%, reflecting safe-haven flows amid global uncertainty.

The Day Ahead

Today's key releases include GDP Month-over-Month at 23:00 ET, with consensus at 0.2% following prior 0.1%, potentially signaling modest growth recovery. GDP 3-Month Average is expected at 0.3% vs previous 0.1%, offering insight into quarterly trends. Goods Trade Balance is forecasted at -22.2 billion vs prior -22.72 billion, alongside Non-EU balance, which could highlight export challenges post-Brexit.

Industrial Production MoM consensus is 0.2% after -0.9%, and Manufacturing Production MoM also at 0.2% vs -0.5%, both critical for assessing sector resilience. No major BoE events are scheduled, but markets will watch for any spillover from global oil dynamics. These figures could influence sterling and gilt yields if they deviate from expectations.

Other Economic Notes

Broader UK themes point to stagflation risks, with verified CPI YoY at 3.40% as of March 2025 remaining above target, complicating BoE's balancing act. Unemployment at 5.10% as of October 2025 underscores labor market slack, potentially easing wage pressures but raising recession concerns. Housing data like RICS suggests affordability strains from high rates, which could dampen consumer confidence and investment.