UK Macro Daily(Beta Mode)

BoE Steady Amid Iran Jitters

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,261.15 | -0.43% |

| FTSE 250 | 22,022.47 | -0.22% |

| GBP/USD | 1.33 | -0.49% |

| GBP/EUR | 1.16 | -0.12% |

| GBP/JPY | 211.87 | -0.33% |

| Brent Crude | 103.76 | +3.54% |

| Gold | 5,034.60 | +0.81% |

| UK Nat Gas | 3.04 | +0.43% |

| Bitcoin | 74,028.94 | +1.70% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

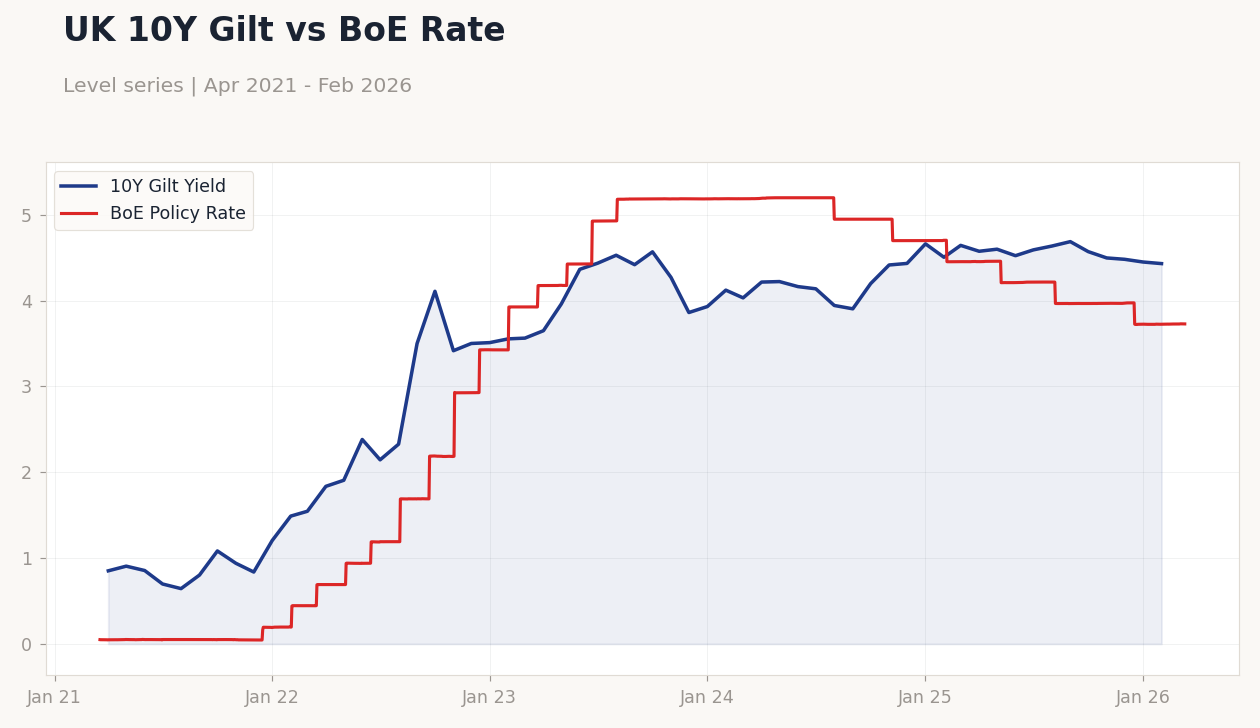

UK 10Y Gilt vs BoE Rate | Type: macro_line | 10Y Gilt Yield: 4.432 (2026-02-01) | Range: 0.644–4.689 | Trend(6pt): 0.8515,2.382,4.53,4.199,4.483,4.432 | BoE Policy Rate: 3.729 (2026-03-12) | Range: 0.045–5.2 | Trend(6pt): 0.0493,1.19,5.185,4.7,3.729,3.729

UK 10Y Gilt vs BoE Rate | Type: macro_line | 10Y Gilt Yield: 4.432 (2026-02-01) | Range: 0.644–4.689 | Trend(6pt): 0.8515,2.382,4.53,4.199,4.483,4.432 | BoE Policy Rate: 3.729 (2026-03-12) | Range: 0.045–5.2 | Trend(6pt): 0.0493,1.19,5.185,4.7,3.729,3.729

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoE Evans Speech | - | - | 03:30 |

| Thursday (2026-03-19) | |||

| Headline Unemployment Rate | 5.20 | 5.20 | 23:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.20 | 3.90 | 23:00 |

| Employment Change | 52,000 | - | 23:00 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 04:00 |

| BoE MPC Vote Cut | 4 | - | 04:00 |

| BoE MPC Vote Hike | 0 | - | 04:00 |

| BoE MPC Vote Unchanged | 5 | - | 04:00 |

| MPC Meeting Minutes | - | - | 04:00 |

- UK markets dipped on energy volatility and rate hold expectations, with FTSE 100 down 0.43% and GBP/USD off 0.49%.

- Broader news highlights BoE caution on inflation amid Iran conflict, stalling growth, and AI bias concerns.

- Upcoming BoE speech and data releases to shape policy outlook, with rate decision eyed for Thursday.

Yesterday's Recap

UK markets closed lower on March 16, with the FTSE 100 falling 0.43% to 10,261.15, pressured by global risk aversion despite Brent crude rising 3.54% to 103.76 amid Iran tensions. The FTSE 250 edged down 0.22% to 22,022.47, reflecting domestic caution on consumer spending. Sterling weakened, with GBP/USD dropping 0.49% to 1.33, GBP/EUR slipping 0.12% to 1.16, and GBP/JPY declining 0.33% to 211.87, driven by safe-haven demand.

UK 10Y Gilt yields fell 0.42% to 4.43%, signaling caution amid geopolitical risks. No major data releases occurred, but news noted flatlining January GDP due to reduced eating out, weighing on sentiment before the Iran energy shock. Gold rose 0.81% to 5,034.60, while Bitcoin gained 1.70% to 74,028.94, offering diversification as UK natural gas edged up 0.43% to 3.04.

Overall, markets reflected uncertainty from the Iran crisis testing BoE models.

The Day Ahead

Today's key event is the BoE Evans speech at 03:30 ET, expected to provide insights on monetary policy amid ongoing inflation pressures. Tomorrow brings high-impact headline unemployment rate at 23:00 ET, with consensus at 5.2% matching the previous 5.2%, alongside medium-impact average earnings including bonus at 3.9% consensus versus prior 4.2%, and employment change with no consensus after 52,000 previous. Thursday features the BoE interest rate decision at 04:00 ET, consensus holding at 3.73% from previous, accompanied by MPC vote details and meeting minutes.

These releases could influence gilt yields and sterling, particularly if unemployment holds steady. Friday's CBI industrial trends orders at 03:00 ET, consensus -29 from -28 previous, will gauge manufacturing sentiment. Markets anticipate no surprises, but deviations could shift rate cut bets.

Other Economic Notes

The UK economy showed signs of stagnation in January, with flat GDP attributed to reduced consumer spending on dining out, exacerbating pre-existing slowdowns before the Iran energy shock. Persistent services inflation, as seen in recent CPI at 3.40% YoY, continues to challenge the BoE's 2% target, while unemployment at 5.20% indicates labor market resilience but potential slack. (cont...)