UK Macro Daily(Beta Mode)

FTSE Gains, BoE Hold Eyed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,317.69 | +0.55% |

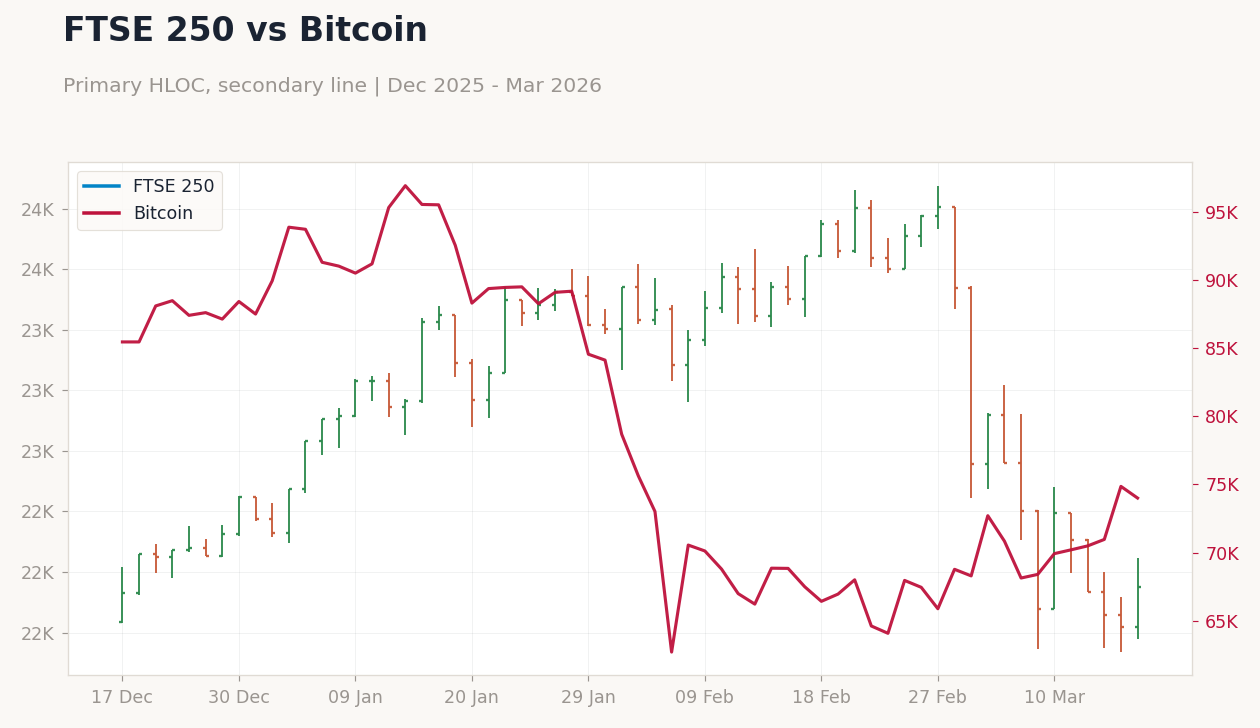

| FTSE 250 | 22,186.62 | +0.75% |

| GBP/USD | 1.34 | +0.43% |

| GBP/EUR | 1.16 | +0.04% |

| GBP/JPY | 212.21 | +0.18% |

| Brent Crude | 101.12 | -2.22% |

| Gold | 5,002.20 | +0.02% |

| UK Nat Gas | 2.94 | -3.10% |

| Bitcoin | 73,905.14 | -1.28% |

| UK 2Y Gilt | - | - |

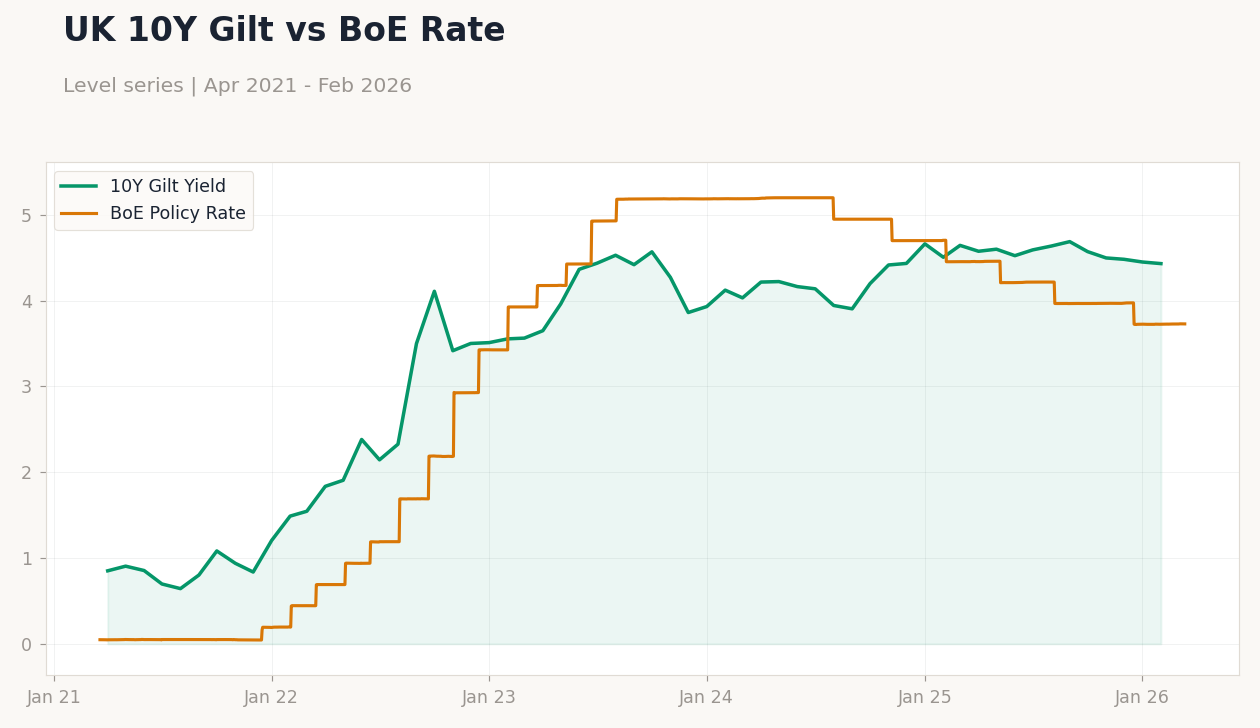

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

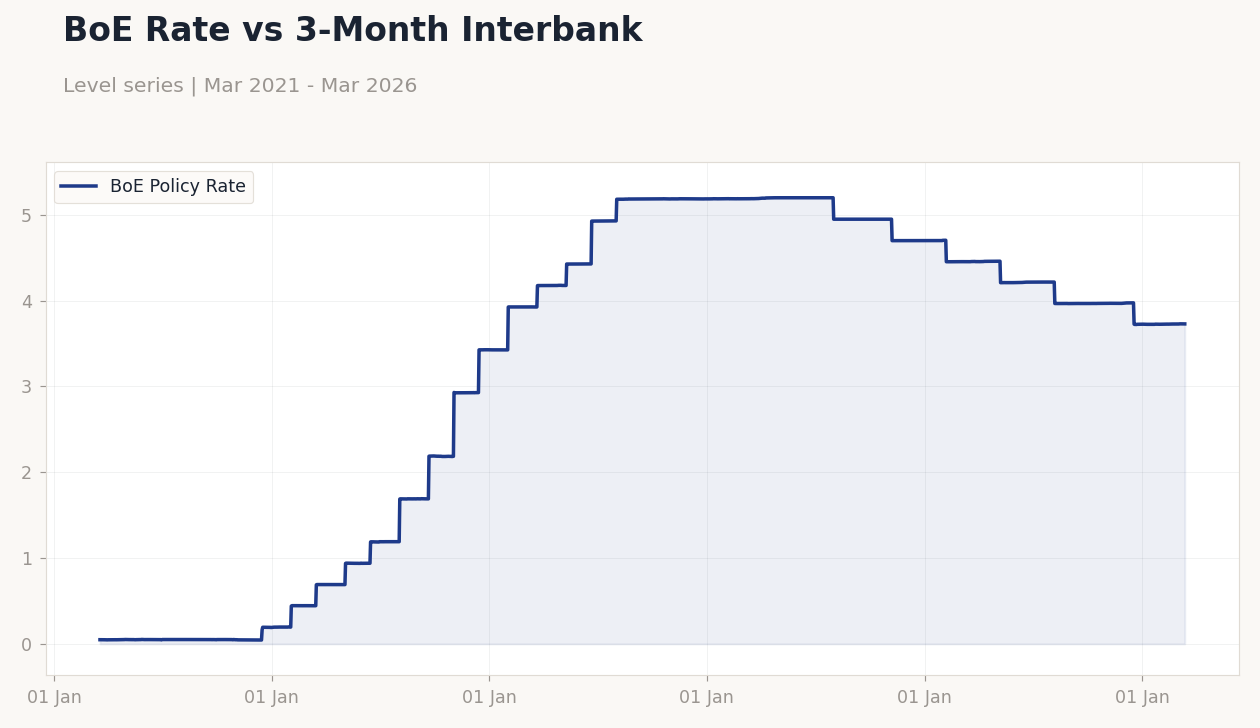

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.729 (2026-03-13) | Range: 0.045–5.2 | Trend(6pt): 0.0485,1.189,5.185,4.7,3.729,3.729

BoE Rate vs 3-Month Interbank | Type: macro_line | BoE Policy Rate: 3.729 (2026-03-13) | Range: 0.045–5.2 | Trend(6pt): 0.0485,1.189,5.185,4.7,3.729,3.729

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-03-19) | |||

| Headline Unemployment Rate | 5.20 | 5.30 | 03:00 |

| Average Earnings incl. Bonus (3Mo/Yr) | 4.20 | 3.90 | 03:00 |

| Employment Change | 52,000 | -4,000 | 03:00 |

| BoE Interest Rate Decision | 3.75 | 3.75 | 08:00 |

| BoE MPC Vote Cut | 4 | - | 08:00 |

| BoE MPC Vote Hike | 0 | - | 08:00 |

| BoE MPC Vote Unchanged | 5 | - | 08:00 |

| MPC Meeting Minutes | - | - | 08:00 |

| Friday (2026-03-20) | |||

- UK equities advanced with FTSE 100 up 0.55% amid positive sentiment, while sterling strengthened against major crosses on yield support.

- Gilt yields dipped slightly, with 10Y at 4.43% down 0.42%, reflecting cautious market positioning ahead of BoE decision.

- No major data releases yesterday, but global energy dynamics pressured Brent and UK Nat Gas lower.

Yesterday's Recap

UK markets posted modest gains on March 17 with no significant data releases, as the FTSE 100 climbed 0.55% to 10,317.69, buoyed by banking and energy sector resilience despite falling oil prices. The FTSE 250 outperformed, rising 0.75% to 22,186.62, driven by mid-cap recovery in consumer-facing stocks amid easing retail concerns. Sterling appreciated across pairs, with GBP/USD up 0.43% to 1.34 and GBP/EUR edging 0.04% higher to 1.16, supported by relative yield attractiveness.

Brent crude fell 2.22% to 101.12, weighed down by supply glut fears, while UK Natural Gas dropped 3.10% to 2.94 on mild weather outlooks. Gold held steady with a marginal 0.02% gain to 5,002.20, acting as a haven amid broader commodity volatility. Bitcoin declined 1.28% to 73,905.14, reflecting crypto market corrections.

Overall, the absence of UK data kept focus on global cues, with Gilt yields softening as 10Y fell 0.42% to 4.43%.

The Day Ahead

Attention turns to March 19 releases, starting with the headline unemployment rate at 03:00 ET, expected at 5.3% versus previous 5.2%, alongside average earnings including bonus at 3.9% (prior 4.2%) and employment change forecasted at -4,000 (prior 52,000). The Bank of England's interest rate decision follows at 08:00 ET, with consensus for no change from 3.75%, accompanied by MPC vote details and meeting minutes that could signal future policy tilts. On March 20, CBI Industrial Trends Orders are due at 07:00 ET, anticipated at -29 versus previous -28, providing insights into manufacturing sentiment.

Looking further, March 24 brings S&P Global Manufacturing PMI Flash and Services PMI Flash at 05:30 ET, with no consensus yet but building on priors of 51.7 and 53.9 respectively, plus CBI Distributive Trades at 07:00 ET following -43. These events could influence sterling and Gilt pricing, especially if labor data surprises amid ongoing inflation pressures. Markets will scrutinize BoE guidance for hints on quantitative tightening amid energy-driven inflation risks.

Other Economic Notes

Persistent inflation remains a core theme, with UK CPI YoY at 3.40% underscoring services and wage pressures that challenge the BoE's 2% target. Unemployment at 5.20% highlights a resilient labor market, potentially fueling further wage growth and delaying rate cuts. (cont...)