UK Macro Daily(Beta Mode)

BoE Holds Amid Energy Shock

Market Snapshot

| Asset | Level | Change |

|---|---|---|

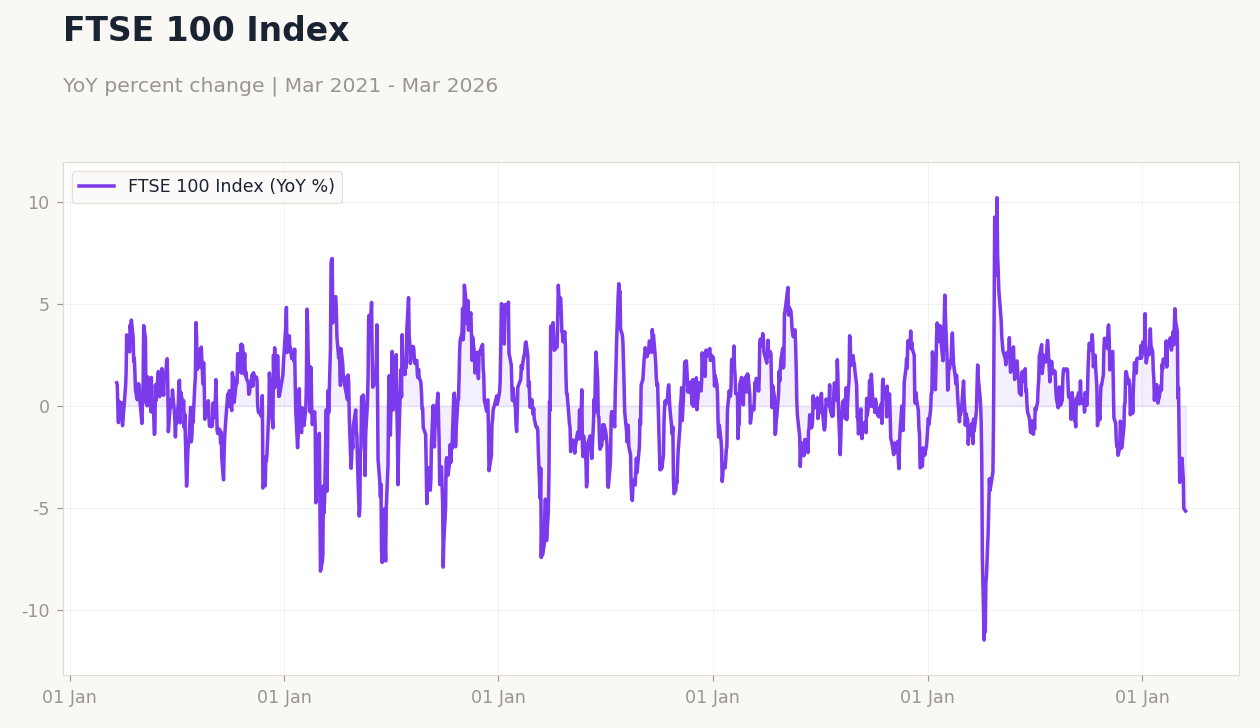

| FTSE 100 | 9,918.33 | -1.44% |

| FTSE 250 | 21,341.97 | -1.01% |

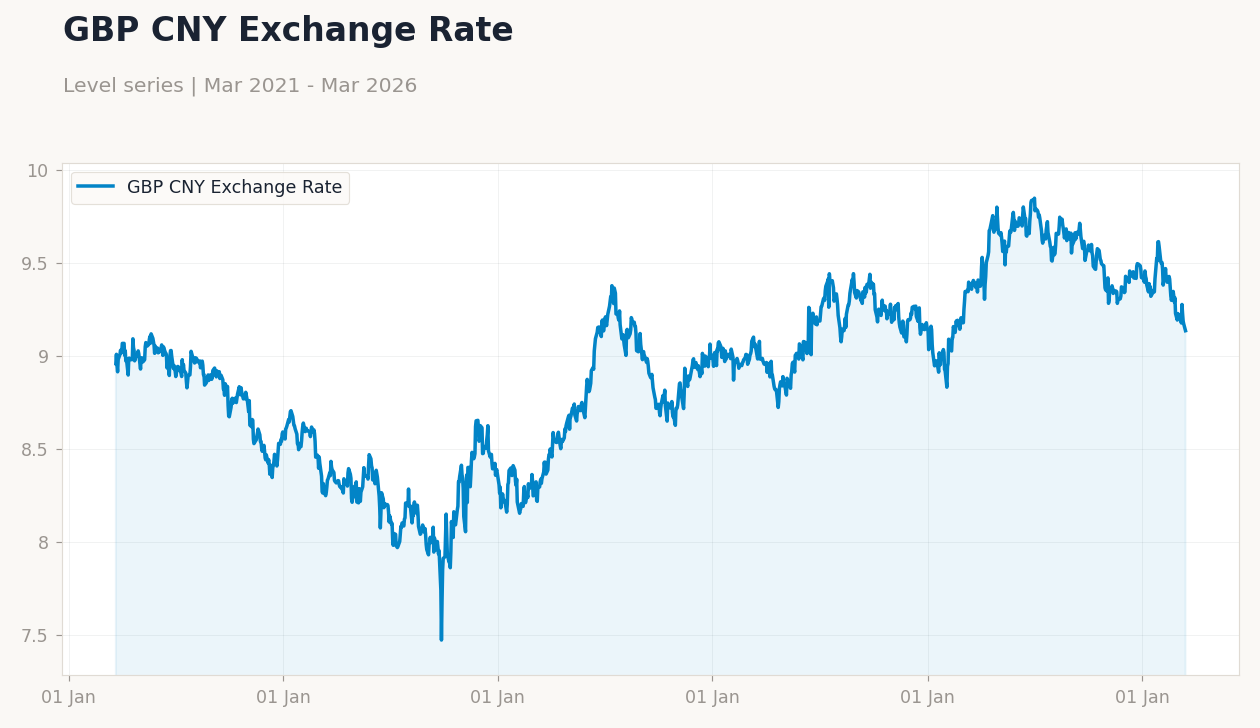

| GBP/USD | 1.33 | -0.63% |

| GBP/EUR | 1.15 | -0.56% |

| GBP/JPY | 212.44 | +0.20% |

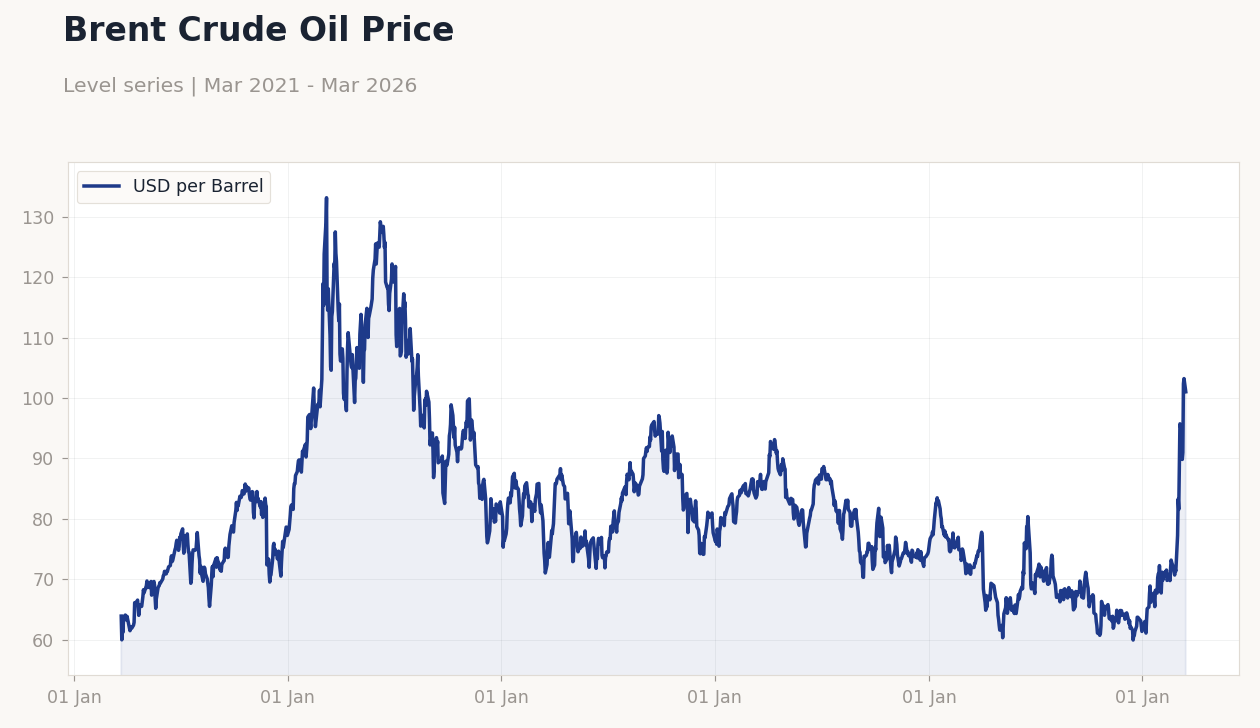

| Brent Crude | 106.41 | -2.06% |

| Gold | 4,574.90 | -0.56% |

| UK Nat Gas | 3.10 | -2.24% |

| Bitcoin | 70,276.18 | -0.35% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

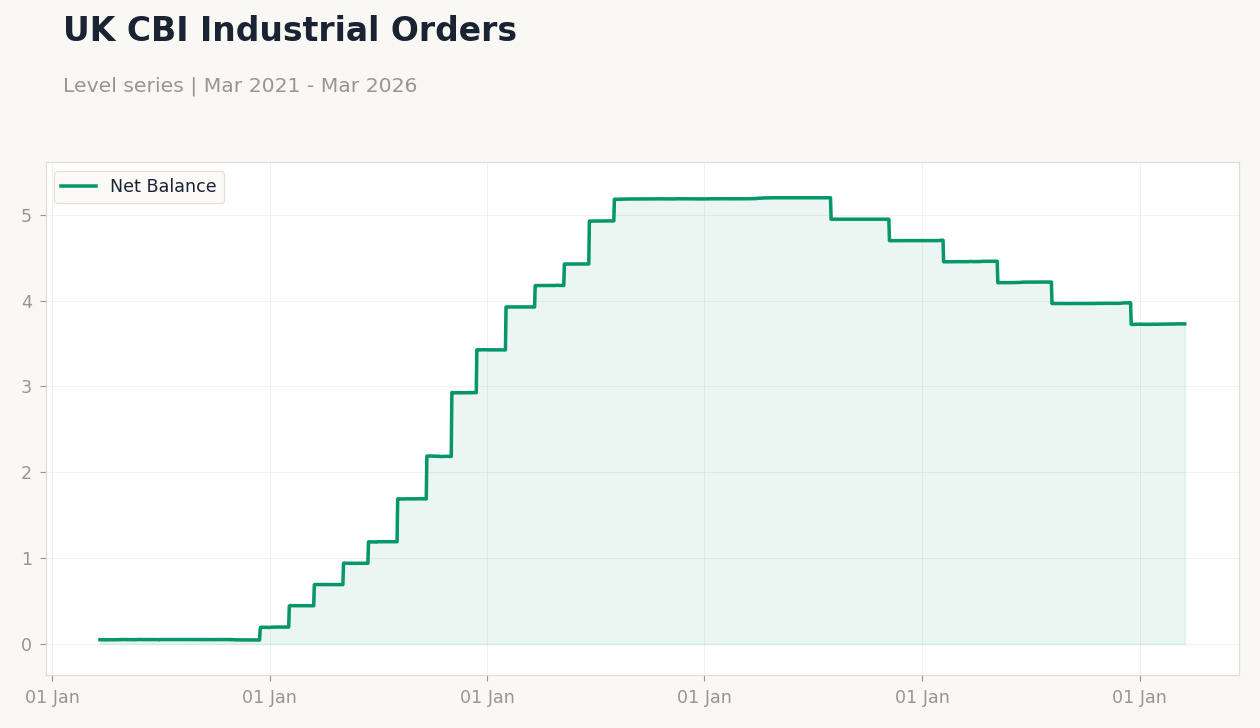

| CBI Industrial Trends Orders | -28 | -29 | -27 |

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 101 (2026-03-16) | Range: 59.93–133.2 | Trend(5pt): 63.89,118.5,94.56,74.3,101

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 101 (2026-03-16) | Range: 59.93–133.2 | Trend(5pt): 63.89,118.5,94.56,74.3,101

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-03-24) | |||

| S&P Global Manufacturing PMI Flash | 51.70 | 51.10 | 05:30 |

| S&P Global Services PMI Flash | 53.90 | 53 | 05:30 |

| CBI Distributive Trades | -43 | -40 | 07:00 |

| Wednesday (2026-03-25) | |||

| Inflation Rate Year-over-Year | 3 | 3 | 03:00 |

| Core Inflation Rate Year-over-Year | 3.10 | 3.10 | 03:00 |

| Inflation Rate Month-over-Month | -0.50 | - | 03:00 |

| Friday (2026-03-27) | |||

| GFK Consumer Confidence Index | -19 | -24 | 20:01 |

- CBI orders beat expectations at -27, signaling modest industrial resilience amid global tensions.

- FTSE indices fell over 1%, GBP weakened vs USD and EUR, as Iran war pressures energy prices.

- BoE maintains hawkish stance on rates, eyeing inflation risks from geopolitical volatility.

Yesterday's Recap

UK markets closed lower on March 20, with the FTSE 100 dropping 1.44% to 9,918.33, driven by declines in energy and mining sectors amid falling Brent crude prices. The FTSE 250 fell 1.01% to 21,341.97, reflecting broader domestic concerns over consumer spending and inflation. Sterling weakened, with GBP/USD down 0.63% to 1.33 and GBP/EUR slipping 0.56% to 1.15, though GBP/JPY rose 0.20% to 212.44 on yield differentials.

Brent crude declined 2.06% to 106.41, pressured by US-Israel efforts to ease Iran war fears, while UK natural gas dropped 2.24% to 3.10. The CBI Industrial Trends Orders for March came in at -27, better than the consensus -29 and previous -28, indicating slight improvement in manufacturing sentiment despite external shocks. UK 10-year Gilt yields fell 0.42% to 4.43%, providing some bond market relief, but gold eased 0.56% to 4,574.90 as safe-haven demand moderated.

Overall, these moves underscored investor caution amid persistent inflation worries and geopolitical risks.

The Day Ahead

No major UK data releases are scheduled for March 21. The upcoming week features key indicators starting March 24 with S&P Global Manufacturing PMI flash expected at 51.1 (previous 51.7) and Services PMI at 53 (previous 53.9), both high-impact gauges of sector health amid energy volatility. CBI Distributive Trades for March follows at 07:00, forecasted at -40 versus previous -43, offering retail sentiment insights.

On March 25, inflation figures include YoY rate at consensus 3% (previous 3%), core YoY at 3.1% (previous 3.1%), and MoM at consensus unchanged (previous -0.5%). March 26 brings GFK Consumer Confidence at consensus -24 (previous -19), highlighting potential household mood shifts. Retail sales on March 27 include MoM at -0.4% (previous 1.8%) and YoY unspecified (previous 4.5%), critical for consumption trends.

These could sway BoE rate expectations if they show ongoing inflationary pressures from global events.

Other Economic Notes

Broader UK themes focus on inflation persistence, with verified CPI YoY at 3.40% as of March 2025, complicating the BoE's easing path. (cont...)