UK Macro Daily(Beta Mode)

UK PMIs Mixed, Inflation Holds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 9,965.16 | +0.72% |

| FTSE 250 | 21,475.45 | +1.61% |

| GBP/USD | 1.34 | -0.46% |

| GBP/EUR | 1.16 | +0.04% |

| GBP/JPY | 212.98 | +0.02% |

| Brent Crude | 98.96 | -3.19% |

| Gold | 4,470.40 | -1.75% |

| UK Nat Gas | 2.91 | -1.29% |

| Bitcoin | 69,993.00 | -0.74% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 51.70 | 50.10 | 51.40 |

| S&P Global Services PMI Flash | 53.90 | 53 | 51.20 |

| CBI Distributive Trades | -43 | -40 | -52 |

| BoE Pill Speech | - | - | - |

| Inflation Rate Year-over-Year | 3 | 3 | 3 |

| Core Inflation Rate Year-over-Year | 3.10 | 3.10 | 3.20 |

| Inflation Rate Month-over-Month | -0.50 | 0.40 | 0.40 |

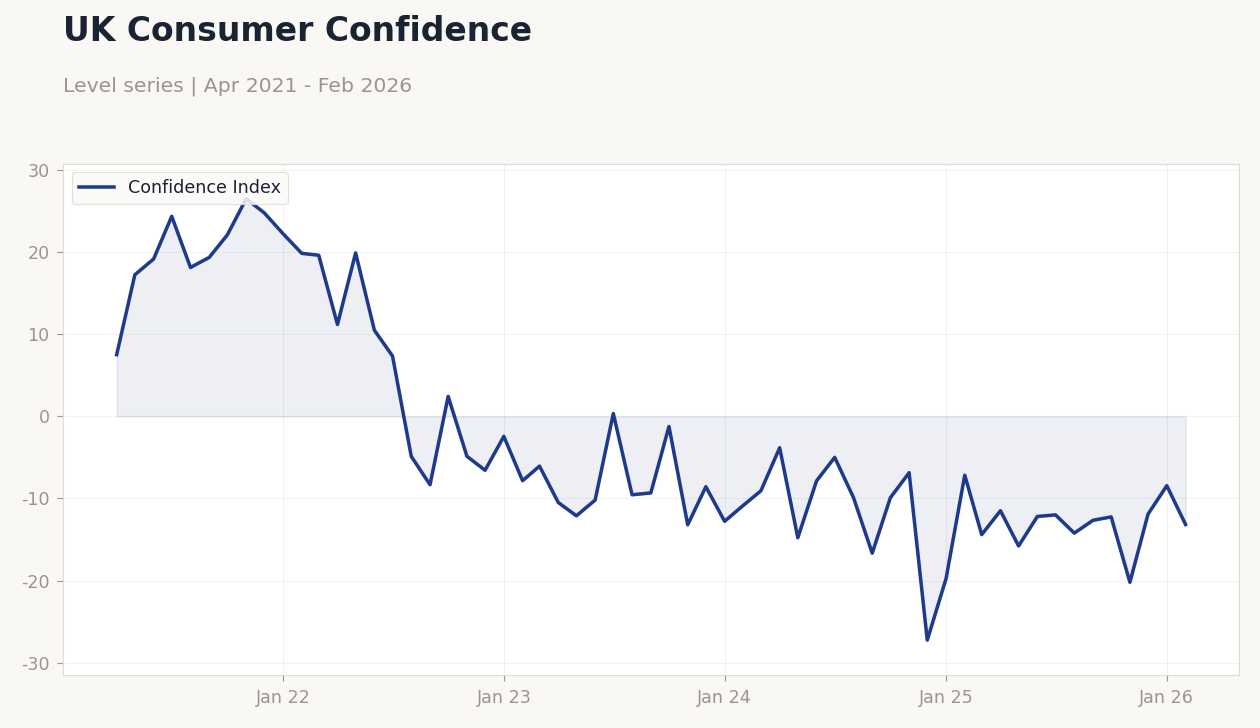

UK Consumer Confidence | Type: macro_line | Confidence Index: -13.16 (2026-02-01) | Range: -27.23–26.47 | Trend(6pt): 7.508,10.48,-9.548,-9.908,-11.9,-13.16

UK Consumer Confidence | Type: macro_line | Confidence Index: -13.16 (2026-02-01) | Range: -27.23–26.47 | Trend(6pt): 7.508,10.48,-9.548,-9.908,-11.9,-13.16

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-03-26) | |||

| BoE Taylor Speech | - | - | 08:00 |

| GFK Consumer Confidence Index | -19 | -24 | 16:01 |

| Friday (2026-03-27) | |||

| Retail Sales Month-over-Month | 1.80 | -0.80 | 23:00 |

| Retail Sales Year-over-Year | 4.50 | 2.10 | 23:00 |

- UK flash PMIs indicated manufacturing at 51.4 beating consensus but services at 51.2 missing expectations, amid steady headline inflation at 3% YoY.

- CBI Distributive Trades fell to -52, signaling retail weakness, while core inflation rose slightly to 3.2% YoY, adding BoE policy pressures.

- FTSE 100 rose 0.72% to 9,965.16 and FTSE 250 gained 1.61% to 21,475.45, but GBP/USD dipped 0.46% to 1.34 on Iran-related risks.

Yesterday's Recap

On March 24, UK flash manufacturing PMI outperformed at 51.4 versus consensus 50.1, showing expansion despite supply issues, while services PMI underperformed at 51.2 against 53 expected, indicating slowdown in the key sector. CBI Distributive Trades index worsened to -52 from -43, reflecting strained consumer spending from energy costs. Inflation figures met forecasts with headline YoY at 3% and MoM at 0.4%, but core YoY increased to 3.2% from 3.1%, raising worries about persistent pressures.

BoE Chief Economist Pill's speech highlighted inflation vigilance amid geopolitical risks, without policy signals. Markets reacted variably: FTSE 100 advanced 0.72% to 9,965.16 on mining and banking strength, FTSE 250 climbed 1.61% to 21,475.45 via cyclicals, yet GBP/USD declined 0.46% to 1.34 due to oil instability from Iran's blockade. Gilt yields fell, with 10Y at 4.43% down 0.42%, as traders eyed sustained BoE caution.

Brent crude decreased 3.19% to 98.96 on supply concerns, affecting UK assets.

The Day Ahead

Focus shifts to BoE's Taylor speech on March 26 at 08:00 ET, offering potential clues on policy amid inflation and global tensions. GFK Consumer Confidence follows at 16:01 ET on March 26, expected at -24 from -19 prior, possibly showing deeper household pessimism from energy prices. Retail sales data arrives March 27 at 23:00 ET, projected to drop MoM to -0.8% from 1.8%, underscoring consumption weakness.

YoY retail sales anticipated at 2.1% from 4.5%, impacting BoE demand views. No key releases today on March 25, with markets tracking global oil movements and US data for GBP implications.

Other Economic Notes

UK faces heightened energy risks from Iran tensions, intensifying living costs and threatening recovery. Inflation persists at 3% YoY, with unemployment at 5.20% as of November 2025, challenging wage and spending dynamics. Mortgage rates are climbing on BoE hawkishness, potentially curbing housing activity and broader growth.