UK Macro Daily(Beta Mode)

UK Housing Data Beats Expectations

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,176.50 | +0.48% |

| FTSE 250 | 21,642.30 | -0.21% |

| GBP/USD | 1.32 | -0.52% |

| GBP/EUR | 1.15 | -0.07% |

| GBP/JPY | 211.24 | +0.10% |

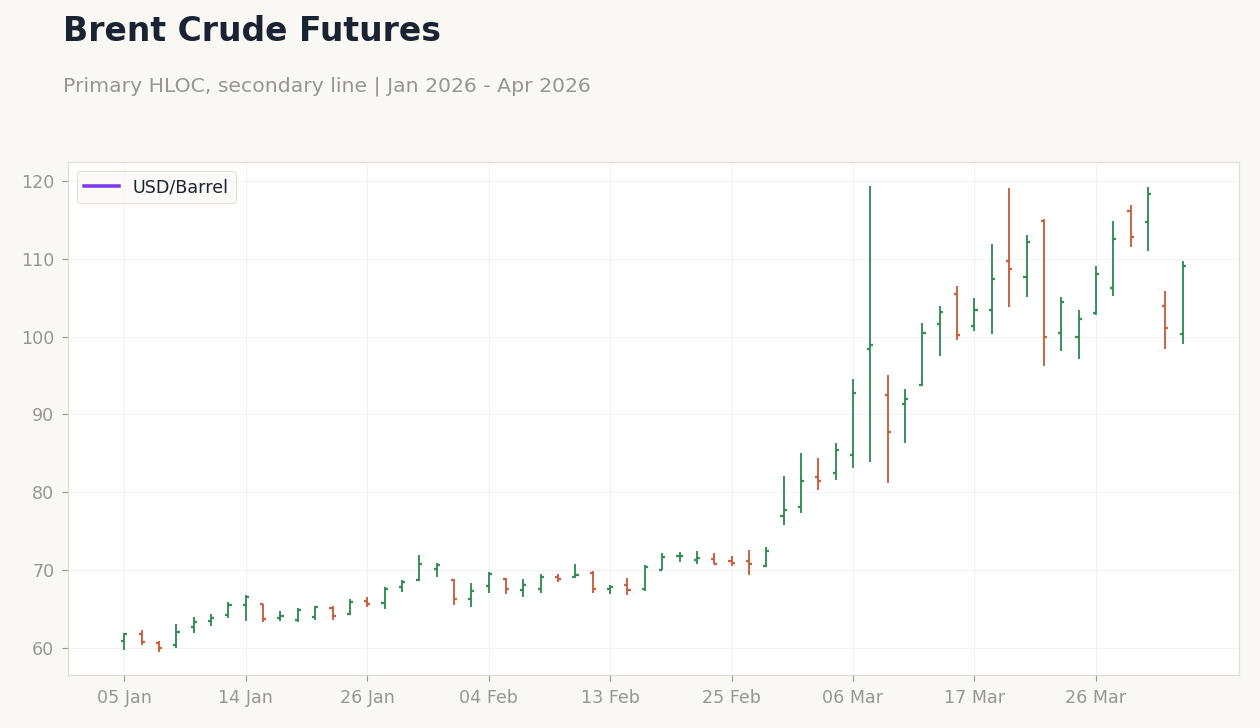

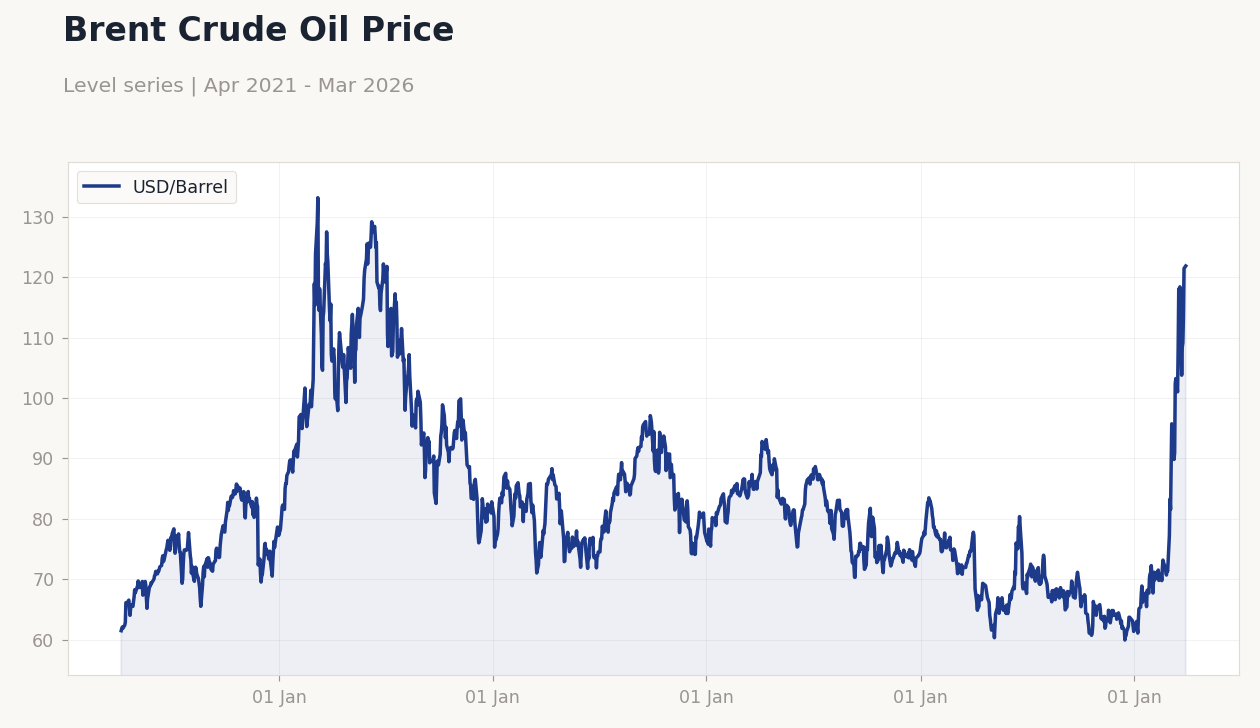

| Brent Crude | 109.03 | +7.78% |

| Gold | 4,651.50 | -2.75% |

| UK Nat Gas | 2.80 | -0.67% |

| Bitcoin | 66,580.33 | -2.20% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoE Consumer Credit | 1,828m | 1,600m | 1,935m |

| Mortgage Approvals | 60,250 | 61,300 | 62,580 |

| Mortgage Lending Level | 4,210m | 4,100m | 4,840m |

| Current Account Balance | -10,700m | -23,400m | -18,400m |

| Nationwide Housing Prices Month-over-Month | 0.30 | 0.60 | 0.90 |

| Nationwide Housing Prices Year-over-Year | 1 | - | 2.20 |

| BoE FPC Meeting Minutes | - | - | - |

Brent Crude Oil Price | Type: macro_line | USD/Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Brent Crude Oil Price | Type: macro_line | USD/Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Housing indicators outperformed forecasts, with mortgage approvals, lending, and prices showing resilience.

- Current account deficit narrowed significantly, bolstering sterling amid global risks.

- BoE FPC minutes stressed vigilance on geopolitical and financial stability threats.

Yesterday's Recap

UK economic data released yesterday highlighted housing sector strength, with BoE Consumer Credit at £1.935 billion, exceeding consensus of £1.6 billion and prior £1.828 billion. Mortgage Approvals reached 62,580, above the 61,300 expected and previous 60,250, while Mortgage Lending hit £4.84 billion, surpassing the £4.1 billion forecast. Nationwide Housing Prices climbed 0.9% month-over-month, better than the 0.6% consensus, and 2.2% year-over-year versus prior 1%.

Current Account Balance deficit was -£18.4 billion, narrower than the -£23.4 billion anticipated and prior -£10.7 billion. BoE FPC Meeting Minutes were released, focusing on systemic risks from geopolitical events. Markets reacted with FTSE 100 at 10,176.50 (+0.48%), supported by the data, while FTSE 250 closed at 21,642.30 (-0.21%).

GBP/USD dipped -0.52% to 1.32 on dollar firmness, GBP/EUR eased -0.07% to 1.15, and GBP/JPY rose +0.10% to 211.24. UK 10Y Gilt yield fell -0.42% to 4.43%.

The Day Ahead

No key UK data or events are scheduled for today, shifting focus to processing yesterday's positive housing figures and monitoring global headlines. The UK-led 35-nation summit on reopening the Strait of Hormuz could influence energy markets and sterling volatility, especially with Brent Crude up +7.78% to 109.03. Watch for impacts from US mortgage rate increases and Fed commentary on broader sentiment.

Gilt and FTSE trading may remain subdued absent escalations, with no BoE speeches planned, potentially allowing risk-off moves if tensions heighten.

Other Economic Notes

UK housing remains robust despite high rates, as recent approvals and price gains indicate sustained demand from wage growth. Inflation persists above target, with UK CPI YoY at 3.40%, complicating BoE easing prospects. Unemployment at 5.20% suggests labor market cooling, which may temper wage inflation but could weaken spending.