UK Macro Daily(Beta Mode)

Gilts Dip on War Volatility

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,176.50 | +0.48% |

| FTSE 250 | 21,642.30 | -0.21% |

| GBP/USD | 1.32 | -0.11% |

| GBP/EUR | 1.15 | +0.04% |

| GBP/JPY | 210.85 | -0.05% |

| Brent Crude | 110.15 | +1.03% |

| Gold | 4,685.50 | +0.73% |

| UK Nat Gas | 2.80 | -0.11% |

| Bitcoin | 69,173.52 | +2.80% |

| UK 2Y Gilt | - | - |

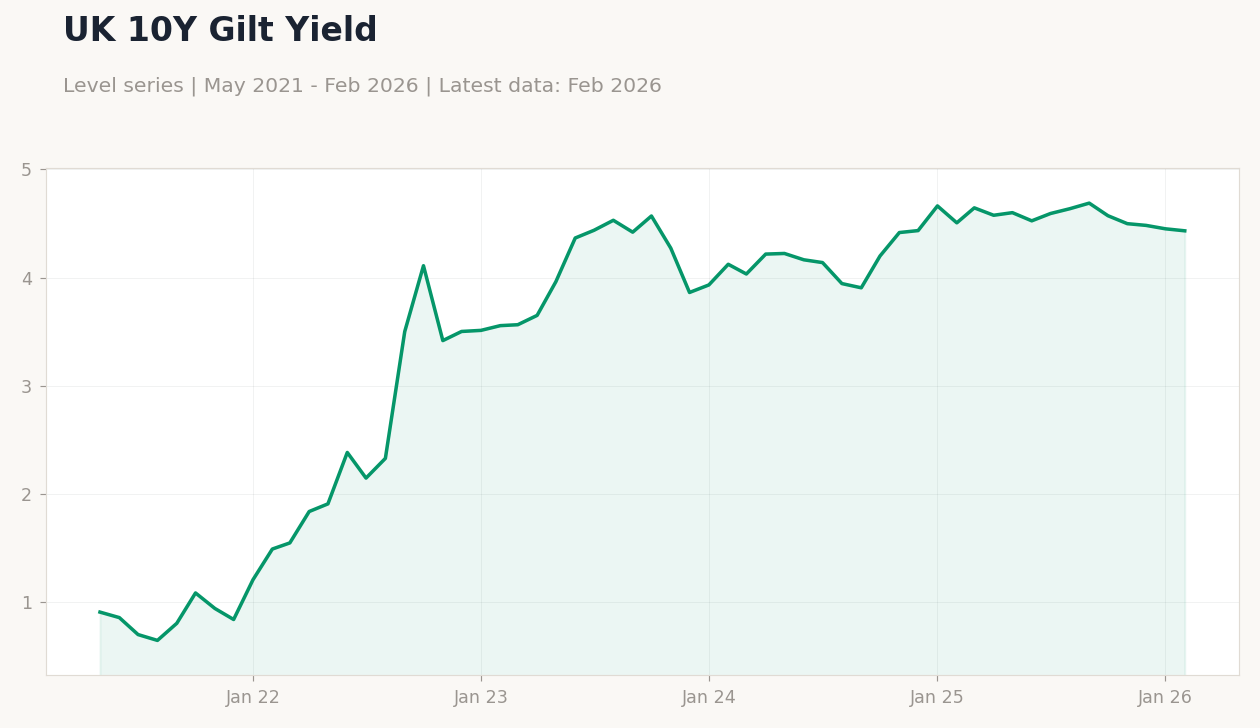

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent USD/bbl: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.86,110.5,89.83,76.14,121.9

Brent Crude Oil Price | Type: macro_line | Brent USD/bbl: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.86,110.5,89.83,76.14,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-08) | |||

| Halifax House Price Index Month-over-Month | 0.30 | - | 22:00 |

| Halifax House Price Index Year-over-Year | 1.30 | - | 22:00 |

| S&P Global Construction PMI | 44.50 | - | 00:30 |

| RICS House Price Balance | -12 | - | 15:01 |

- UK markets mixed: FTSE 100 up 0.48% to 10,176.50 on energy gains, 10Y gilt yield down 0.42% to 4.43% amid risk aversion.

- Sterling softens vs USD to 1.32 (-0.11%), edges up vs EUR to 1.15 (+0.04%).

- Iran conflict raises BoE inflation concerns, potentially delaying rate cuts.

Yesterday's Recap

UK markets displayed resilience yesterday, with the FTSE 100 closing at 10,176.50, up 0.48%, fueled by energy and mining sectors as Brent crude rose to 110.15 (+1.03%). The FTSE 250 slipped to 21,642.30, down 0.21%, under pressure from global uncertainty. Sterling weakened slightly against the dollar to 1.32 (-0.11%) but gained versus the euro to 1.15 (+0.04%), with GBP/JPY dipping to 210.85 (-0.05%).

Gilt yields fell, with the 10-year at 4.43% (-0.42%), driven by safe-haven demand amid Middle East tensions. No major UK data was released, but sentiment reacted to global developments like Iran's resilient oil exports and attacks on UAE facilities. Gold climbed to 4,685.50 (+0.73%), reflecting risk-off flows, while UK natural gas eased to 2.80 (-0.11%) on stable supplies.

Trading volumes stayed moderate, with attention on BoE's potential response to imported inflation.

The Day Ahead

Focus shifts to upcoming UK indicators. The Halifax House Price Index for March releases at 22:00 ET, with prior MoM at 0.3% and YoY at 1.3%, providing housing market insights amid elevated rates. The S&P Global Construction PMI follows at 00:30 ET, previous at 44.5, likely indicating ongoing sector contraction if below 50.

The RICS House Price Balance arrives at 15:01 ET, prior at -12, assessing residential sentiment. These could sway gilt yields and sterling if signaling demand weakness. No BoE speeches planned, but markets eye any comments on global risks.

US data spillovers may influence, though UK metrics drive near-term views.

Other Economic Notes

Stagnation risks loom for the UK economy, with reports citing high taxes, over-regulation, and risk aversion as growth hurdles. Prolonged high rates threaten renewable investments, leading to calls for BoE measures to aid green shifts. Uncertainty could reduce pound buying interest, adding pressure on sterling pairs.