UK Macro Daily(Beta Mode)

BoE Split on Energy Inflation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| FTSE 100 | 10,176.50 | +0.48% |

| FTSE 250 | 21,642.30 | -0.21% |

| GBP/USD | 1.32 | +0.33% |

| GBP/EUR | 1.15 | +0.12% |

| GBP/JPY | 211.37 | +0.33% |

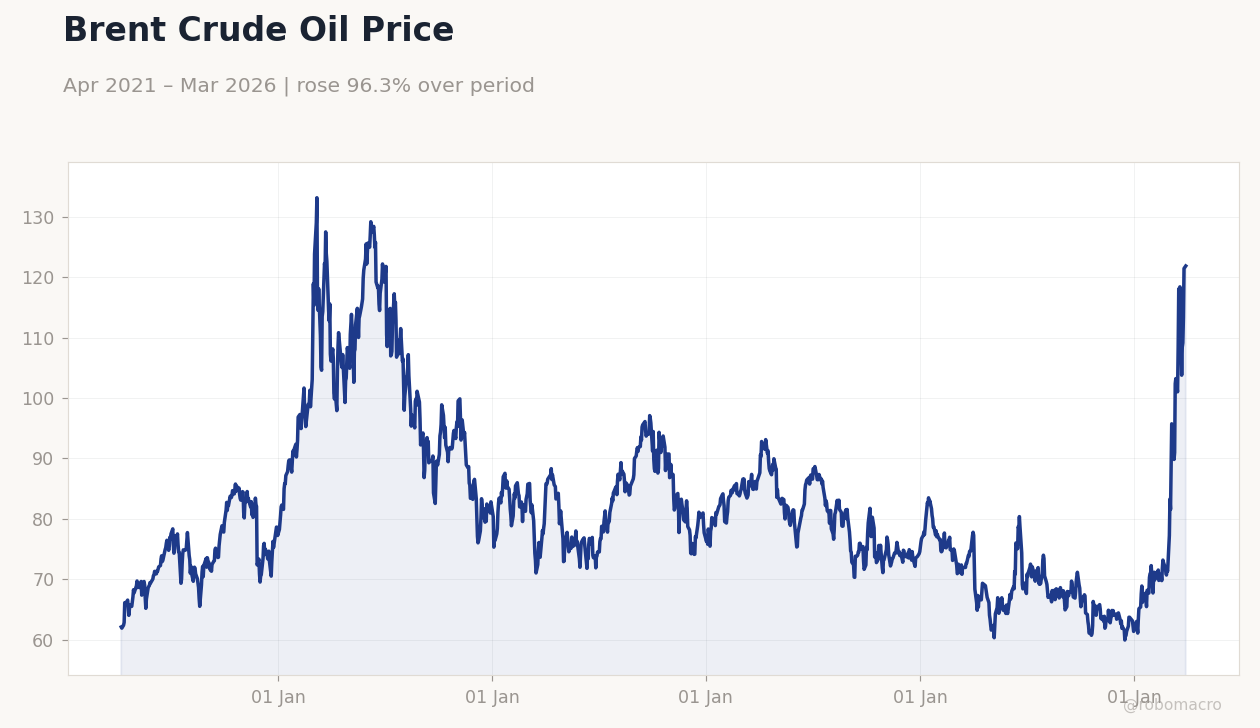

| Brent Crude | 111.35 | +1.44% |

| Gold | 4,661.30 | +0.10% |

| UK Nat Gas | 2.81 | -0.14% |

| Bitcoin | 68,631.14 | -0.51% |

| UK 2Y Gilt | - | - |

| UK 10Y Gilt | 4.43% | -0.42% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(6pt): 62.09,110.5,94.46,74.24,113.4,121.9

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(6pt): 62.09,110.5,94.46,74.24,113.4,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-08) | |||

| Halifax House Price Index Month-over-Month | 0.30 | 0.10 | 22:00 |

| Halifax House Price Index Year-over-Year | 1.30 | 1.50 | 22:00 |

| S&P Global Construction PMI | 44.50 | 43.90 | 00:30 |

| RICS House Price Balance | -12 | -18 | 15:01 |

- Bank of England shows internal divisions on tackling energy-driven inflation amid Iran conflict, holding rates at 3.73%.

- FTSE 100 gains 0.48% on energy sector strength, while gilt yields dip slightly amid volatility warnings.

- Upcoming housing data eyed as sterling firms modestly against major crosses.

Yesterday's Recap

With no major UK data releases on April 6, markets focused on global tensions, driving Brent crude up 1.44% to $111.35 amid Iran conflict fears, boosting energy stocks. The FTSE 100 advanced 0.48% to 10,176.50, supported by oil majors, while the FTSE 250 edged down 0.21% to 21,642.30 on broader caution. Sterling strengthened modestly, with GBP/USD up 0.33% to 1.32 and GBP/EUR rising 0.12% to 1.15, reflecting safe-haven flows.

UK 10-year gilt yields fell 0.42% to 4.43%, signaling bets on steady BoE policy despite inflation pressures. Gold ticked up 0.10% to 4,661.30, underscoring risk aversion, while UK natural gas dipped 0.14% to 2.81 on supply stability. Bitcoin declined 0.51% to 68,631.14, mirroring global crypto volatility.

Overall, UK assets showed resilience but remained sensitive to Middle East developments.

The Day Ahead

Attention turns to the Halifax House Price Index, with month-over-month consensus at 0.1% (prior 0.3%) and year-over-year at 1.5% (prior 1.3%), potentially signaling cooling in the property market amid high borrowing costs. The S&P Global Construction PMI is forecast at 43.9 (prior 44.5), highlighting ongoing sector contraction if it misses. Later, the RICS House Price Balance is expected at -18% (prior -12%), which could pressure sterling if it confirms weakening sentiment.

These medium-impact releases arrive against a backdrop of stable BoE rates at 3.73%, with markets watching for implications on consumer spending. No major BoE speeches are scheduled, leaving data to drive gilt and currency moves. Broader focus includes any updates on energy prices tied to global conflicts.

Other Economic Notes

UK CPI year-over-year stands at 3.40% as of March 2025, exceeding the BoE's 2% target and fueling debates on policy tightening amid energy shocks. Unemployment at 5.20% through November 2025 underscores labor market strains, potentially limiting wage-driven inflation but supporting calls for rate caution. Broader themes include fiscal hints from the government on infrastructure spending, which could offset slowdown risks in construction and housing sectors.